If you’ve ever searched for insurance plans designed to secure your child’s future, you’ve almost certainly stumbled upon the term “Kanyadan Policy.” While it sounds like a tailor-made financial blessing, the reality is that it’s actually a marketing label for the LIC Jeevan Lakshya (Plan 733).

But does this popular plan actually live up to the name, or is it just another insurance product with fancy packaging? Let’s break it down in plain English.

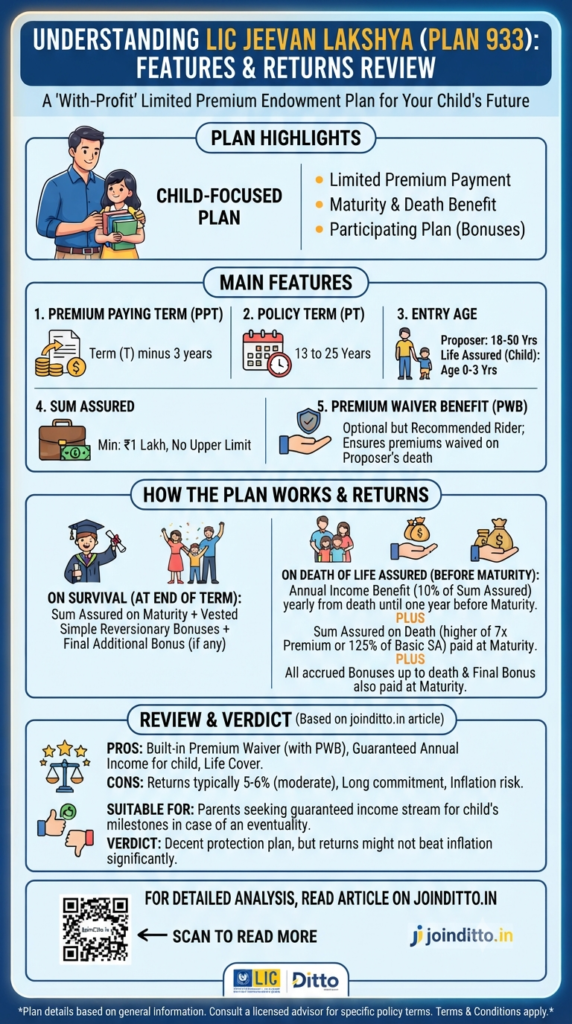

What Exactly Is LIC Jeevan Lakshya?

At its core, Jeevan Lakshya is a participating, non-linked, limited-premium endowment plan. Think of it as a hybrid: it combines life insurance protection with a savings component, specifically designed to help parents stay on track with financial goals—like education or marriage—even if the unexpected happens.

The Standout Feature: If the policyholder (the parent) passes away during the term, the family isn’t left stranded. The plan kicks in an Annual Income Benefit, paying 10% of the Basic Sum Assured every year until one year before maturity. Plus, all future premiums are waived, and the maturity corpus is still paid out at the end.

Is It a Good Investment?

This is where you need to look past the marketing. While the plan offers stability, it’s crucial to understand how it performs as an investment.

- The Returns: Based on the plan’s structure, the internal rate of return (IRR) is generally conservative. Even under optimistic scenarios, the returns typically range between 4% to 6%.

- The Reality Check: When you compare these figures against inflation or alternative long-term savings vehicles like the Public Provident Fund (PPF) or the Sukanya Samriddhi Yojana (SSY), the returns on Jeevan Lakshya often fall short.

The Pros and Cons: A Quick Breakdown

Before you sign on the dotted line, consider these factors:

What Works Well:

- Built-in Safety Net: The waiver of premium and annual income benefit provide genuine peace of mind for families.

- Limited Commitment: You pay premiums for the policy term minus 3 years, which is a nice touch for budget planning.

- LIC’s Stability: For those who prioritize peace of mind and the backing of a massive, state-owned institution over aggressive market returns, it fits the bill.

What to Watch Out For:

- Inflation Risk: Because the returns are modest, they may not grow your corpus fast enough to keep up with the skyrocketing costs of future education or weddings.

- Low Life Cover: The inherent life cover in endowment plans is usually quite small. If you are the primary breadwinner, a dedicated term insurance plan often provides much better protection for your family at a fraction of the cost.

- Bonus Uncertainty: The “profit-sharing” aspect (bonuses) is not guaranteed; it depends entirely on LIC’s performance.

The Final Verdict

LIC Jeevan Lakshya is a decent protection-oriented plan, particularly if you are a conservative investor who wants to ensure specific financial milestones are met regardless of what happens to you.

However, if your primary goal is maximizing wealth to beat inflation or obtaining high-value life cover to protect your family from debt, you might be better off separating your insurance and investment needs. A combination of a pure term insurance policy (for high, affordable protection) and market-linked instruments (for potentially higher returns) often serves families better in the long run.

Not sure which path is right for you? It’s always worth chatting with an expert to see how your specific financial goals align with these products before committing to a 20-year plan!

Disclaimer: This analysis is based on information from Ditto Insurance and is intended for informational purposes only. Insurance decisions should be made in consultation with a licensed advisor.

Finding Opportunity: A Deep Dive into Top Value-Oriented Mutual Funds

The narrative of Indian finance is changing. For generations, the Indian investor’s journey began and ended with safe, traditional avenues like fixed deposits and gold. While secure, these options often struggled to beat inflation, limiting true wealth creation. Today, that script is being rewritten. We are witnessing an unprecedented “financial awakening,” where millions of Indians…

Have you ever wondered what banks and mutual fund houses really think about your accounts? We often view our savings account as the foundation of our financial life—a place to park our salary, pay our bills, and keep our “emergency” cash. But there is a growing realization in the financial world that the traditional savings…

Continue Reading Why Your SIP is More Than Just an Investment—It’s Your New Financial “Superpower”

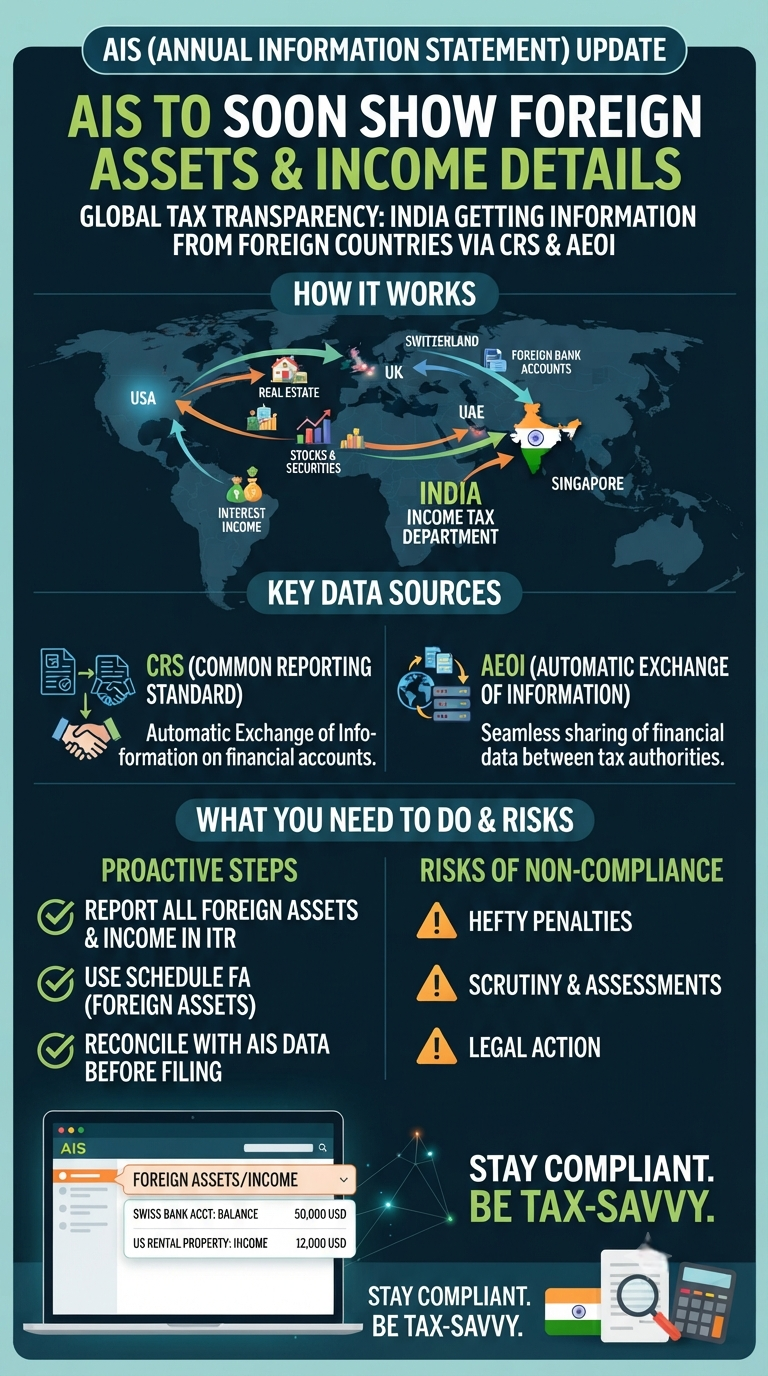

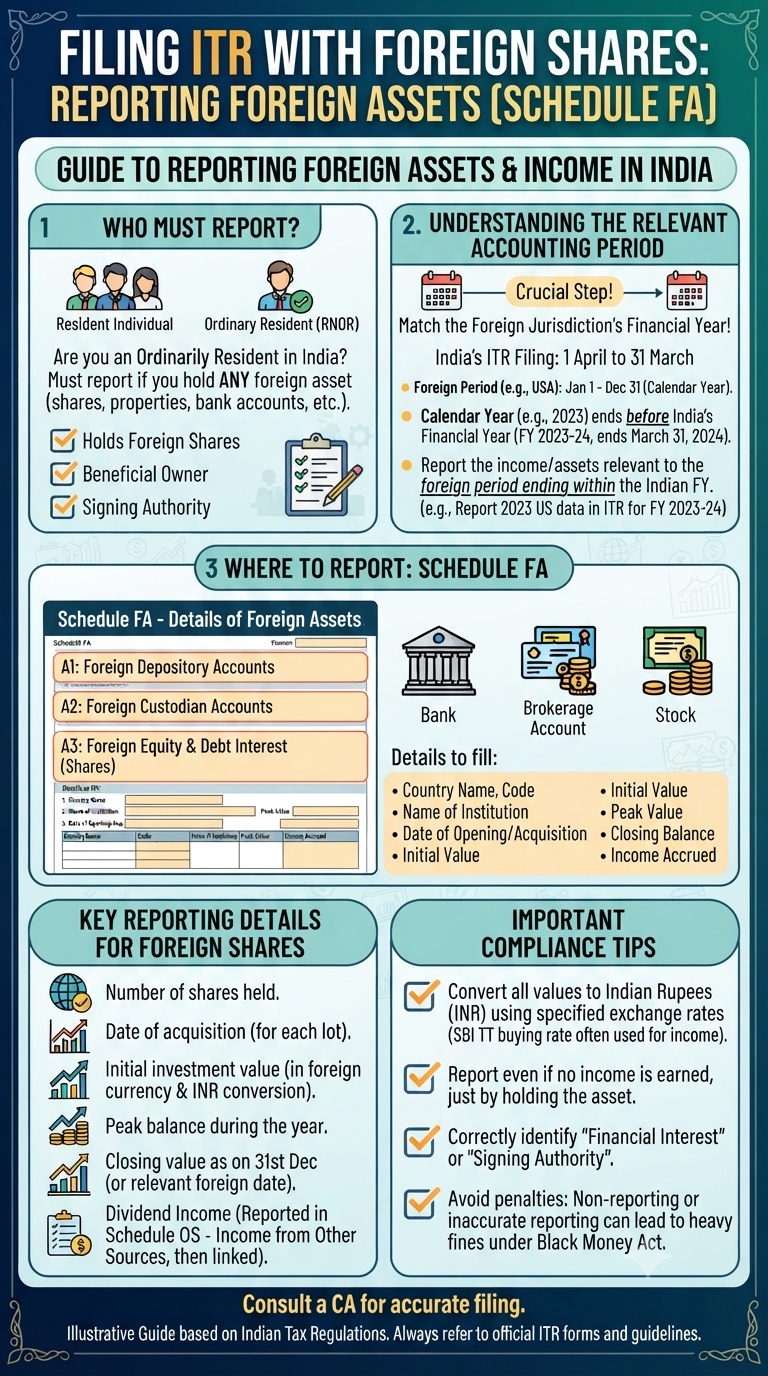

If you have ever held a bank account, real estate, or stocks in another country, you know the anxiety that can come with filing your Income Tax Return (ITR). There has always been a subtle question in the back of many taxpayers’ minds: “Does the tax department already know about this?” As of July 8,…

Continue Reading Hidden No More: What the New AIS Update Means for Your Foreign Assets

So, you’ve dipped your toes into the global market. Whether it’s those Google shares you picked up, a mutual fund in a different country, or simply maintaining an account abroad, investing internationally can be an exciting journey. But as the tax season rolls around, a common question often pops up: “Do I really need to…

Continue Reading Beyond Borders: A Simple Guide to Reporting Your Foreign Assets in Your ITR

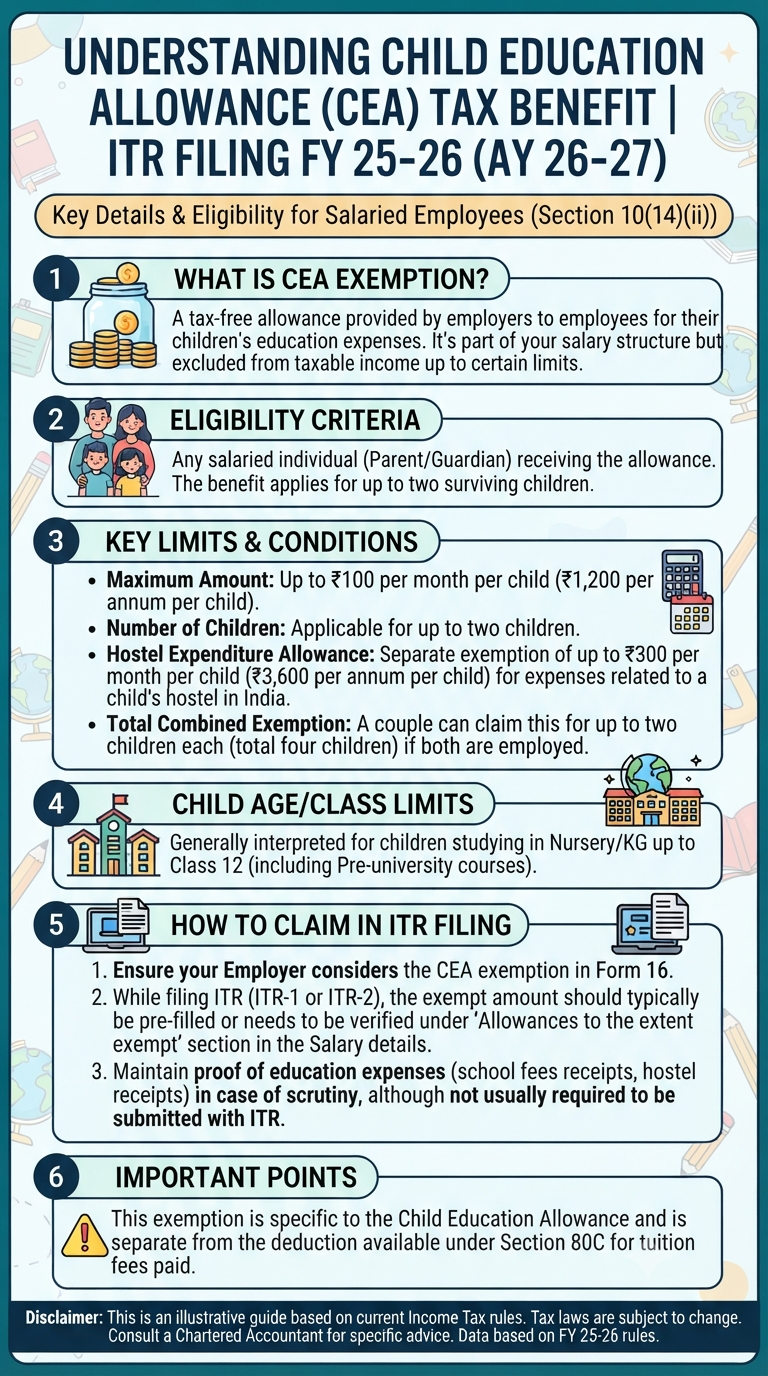

If you’re a salaried parent, you know that the costs of schooling—from uniforms to those ever-increasing activity fees—can add up fast. While we all want the best for our kids, wouldn’t it be nice if the taxman gave us a little breather? Enter the Child Education Allowance (CEA). It’s one of those “hidden” perks in…

Continue Reading Decoding Your Paycheck: A Simple Guide to the Child Education Allowance (CEA)

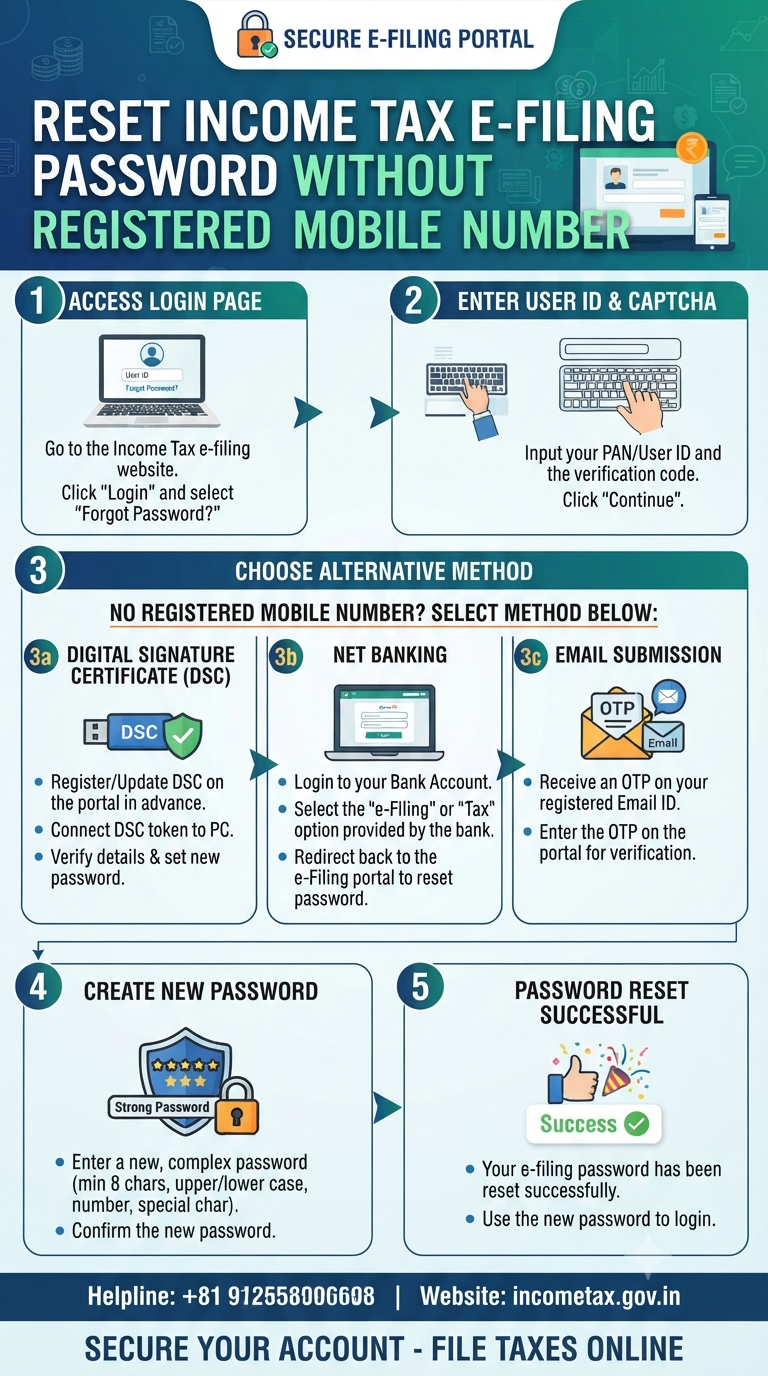

Locked Out of Your Income Tax Account? How to Reset Your Password Without a Registered Mobile Number

We’ve all been there—it’s time to file your ITR, you sit down with your documents, head to the Income Tax e-filing portal, and then… total blank. You’ve forgotten your password. Usually, this is a minor annoyance solved by a quick OTP sent to your registered mobile number. But what if you’ve changed your number, lost…

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.