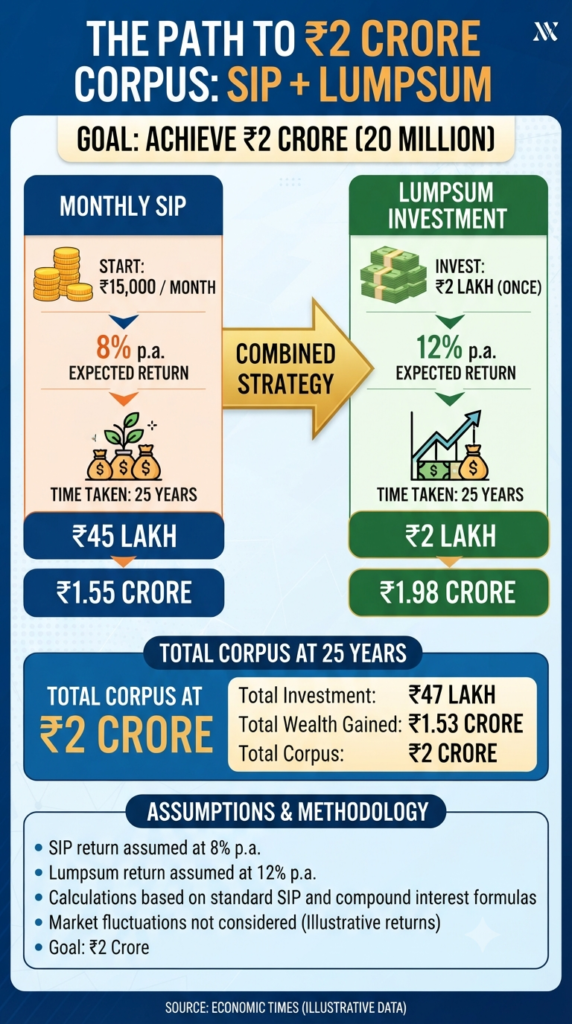

We all have that “magic number” in our heads—the target corpus that represents financial freedom. For many, that number is ₹2 Crore. It sounds like a mountain, doesn’t it? A distant, almost unreachable peak.

But here is the secret that the smartest investors know: Wealth isn’t built in a day; it’s built in decades.

If you have ever wondered exactly what it takes to turn a modest monthly savings plan into a massive financial safety net, we have crunched the numbers for you. The results are not just encouraging; they are a masterclass in the power of compounding.

The Winning Formula

Let’s look at a realistic, actionable strategy that doesn’t require a lottery win. If you start with an initial lumpsum of ₹2 Lakh and commit to a disciplined monthly SIP of ₹15,000, you are already on the path.

Assuming a steady, long-term annual return of 12%, your journey looks like this:

- The Foundation: ₹2 Lakh (Initial Lumpsum)

- The Engine: ₹15,000 (Monthly SIP)

- The Horizon: 22 Years

- The Destination: ~₹2.01 Crore! 🚀

Why 22 Years?

You might look at the “22-year” mark and think, “That’s a long time!” And you’re right—it is. But that is exactly why it works.

Financial independence isn’t about finding the “get-rich-quick” scheme; it’s about letting time do the heavy lifting for you. In the first few years, your money grows slowly. You might not see much of a difference. But as the years turn into a decade, and that decade approaches two, the magic of compounding kicks in. Your interest starts earning interest, and your money begins to grow exponentially rather than linearly.

Your Action Plan

Building a corpus of ₹2 Crore isn’t just about math; it’s about behavior. Before you start, take these three simple steps:

- Know Your Capacity: Be honest about what you can set aside every month without disrupting your lifestyle. Consistency beats intensity every single time.

- Use Your Lumpsum: If you have a bonus, an inheritance, or some idle savings lying around, putting it to work immediately (as a lumpsum) gives your SIP a massive head start.

- Stay the Course: The market will have its ups and downs. The investors who reach the finish line are the ones who don’t stop when the market dips or get over-excited when it surges. Keep your eyes on the 22-year prize.

The Bottom Line

A target of ₹2 Crore is not a dream—it is a destination. With ₹15,000 a month and a bit of patience, you are not just saving money; you are buying your future freedom.

So, are you ready to start your 22-year journey today?

Disclaimer: Investments in mutual funds are subject to market risks. Please read all scheme-related documents carefully. The calculations above are for illustrative purposes based on an assumed 12% annual return and do not guarantee future performance.

Secure Your Daughter’s Dreams: Sukanya Samriddhi Yojana vs. Fixed Deposits

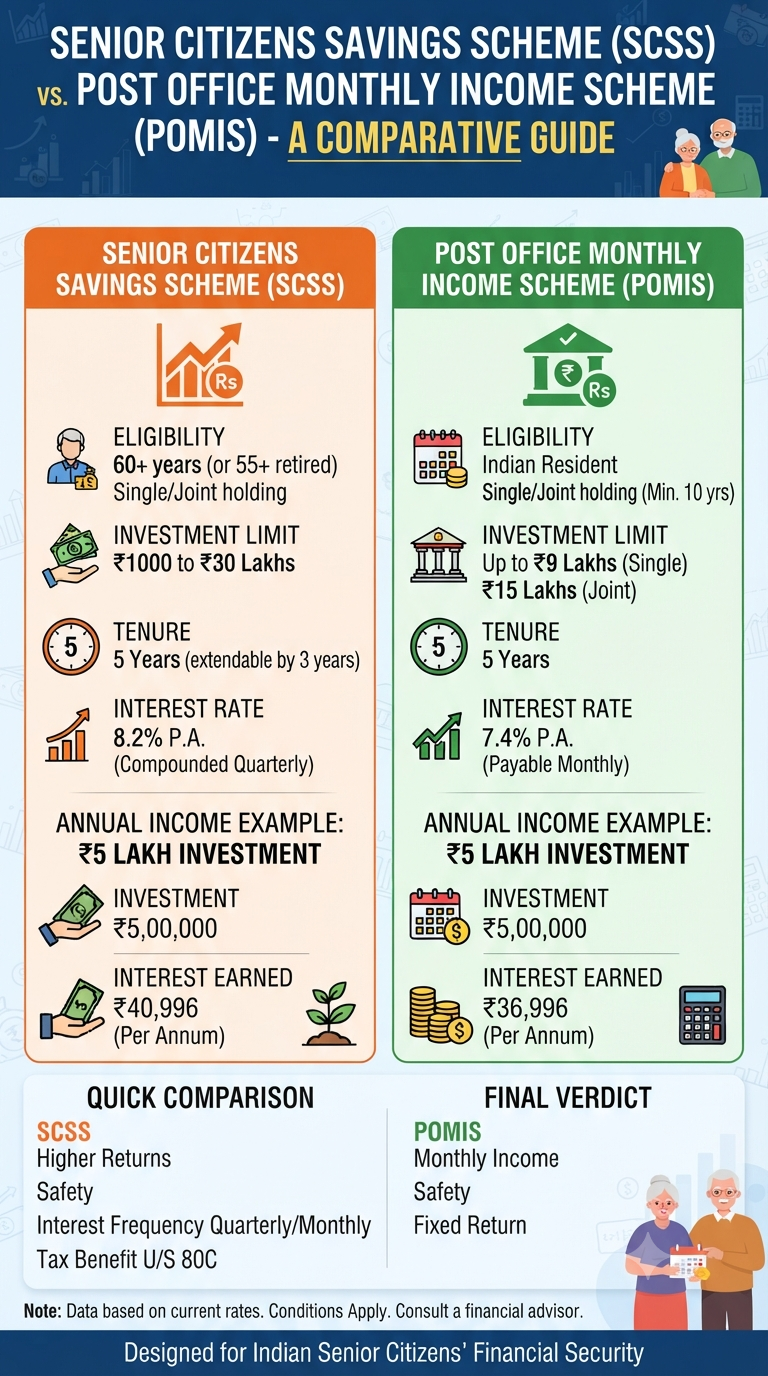

If you are looking for a safe, government-backed harbor for your hard-earned money, the Senior Citizens Savings Scheme (SCSS) and the Post Office Monthly Income Scheme (MIS) are likely at the top of your list. They offer peace of mind, stability, and the reliability of a sovereign guarantee. But when it comes to maximizing your…

Let’s be honest. Most of us know EPF stands for Employees’ Provident Fund, and we know a chunk of our salary goes into it every month. But how many of us actually know exactly how much is in that corpus, or—more importantly—if that promised 8.25% interest has hit our account yet? If you’ve been meaning…

Continue Reading Checkmate Your PF Status: 4 Simple Ways to View Your EPF Balance Right Now

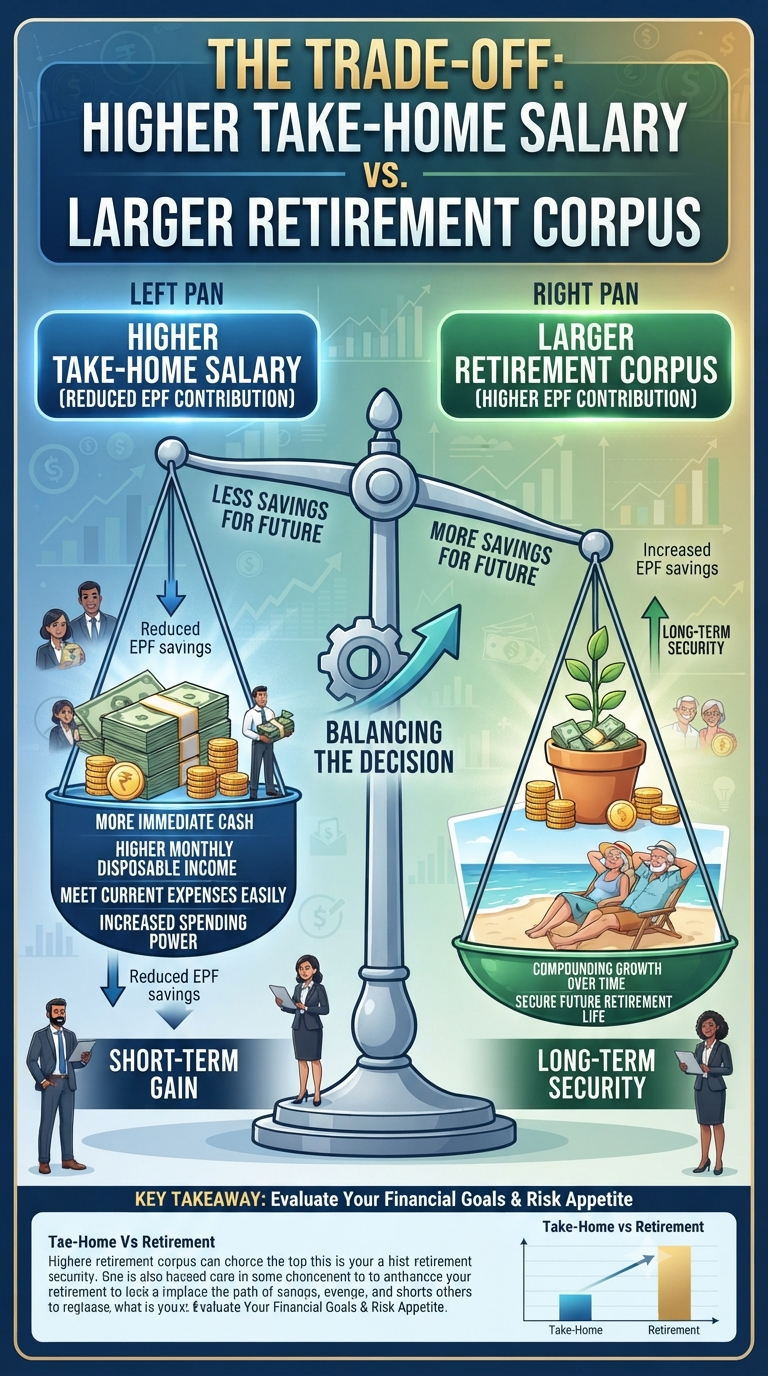

For any salaried professional, that email from HR announcing a salary hike—or better yet, a change that boosts your monthly take-home pay—is usually a cause for celebration. We all love a little extra breathing room in our monthly budget to cover rising costs, splurge on a vacation, or simply enjoy a higher standard of living…

Continue Reading More Cash Today or Millions Tomorrow? Decoding the Proposed EPF Change

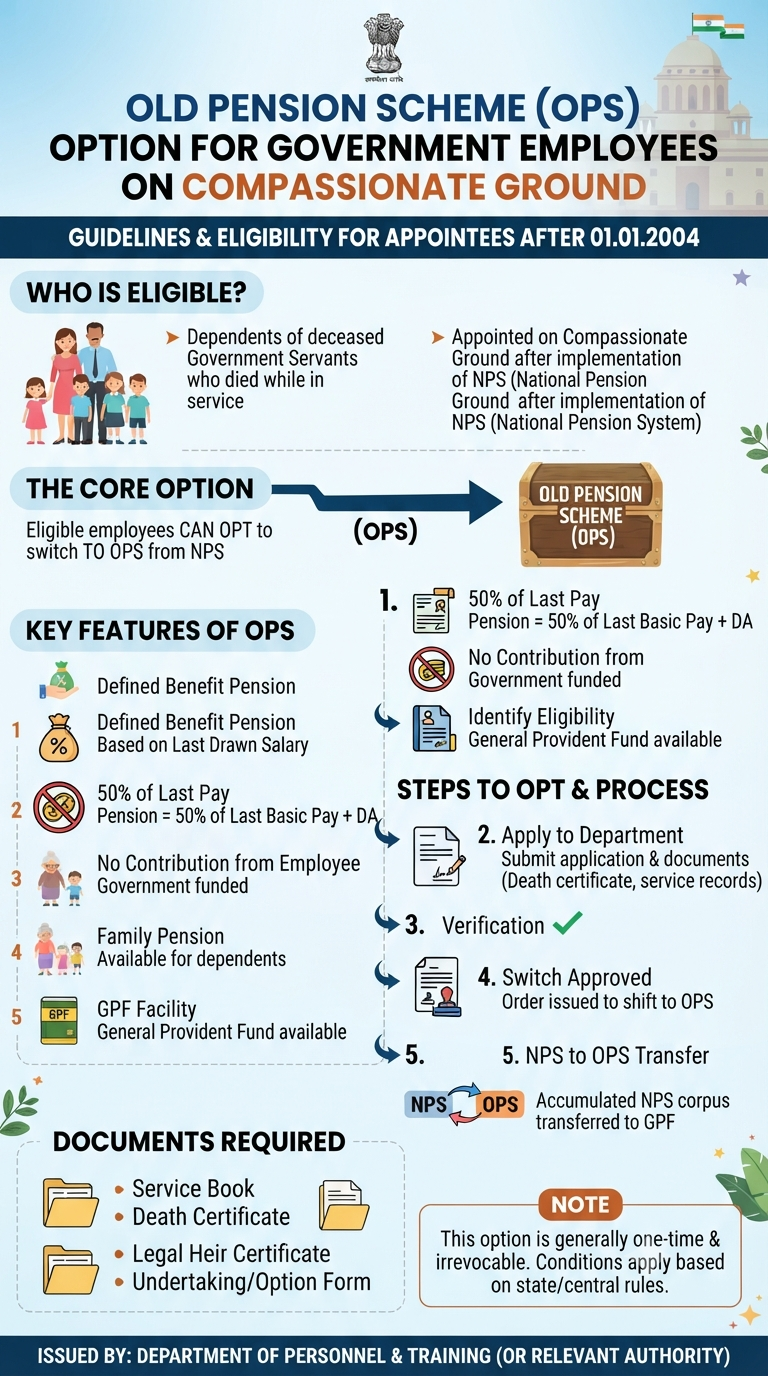

For thousands of government employees who entered service through the compassion of a family-related appointment, the transition into their careers was often marked by a bureaucratic “what-if.” Many had applied for their positions before the cutoff of December 2003, only to join service after the National Pension System (NPS) had already taken hold in January…

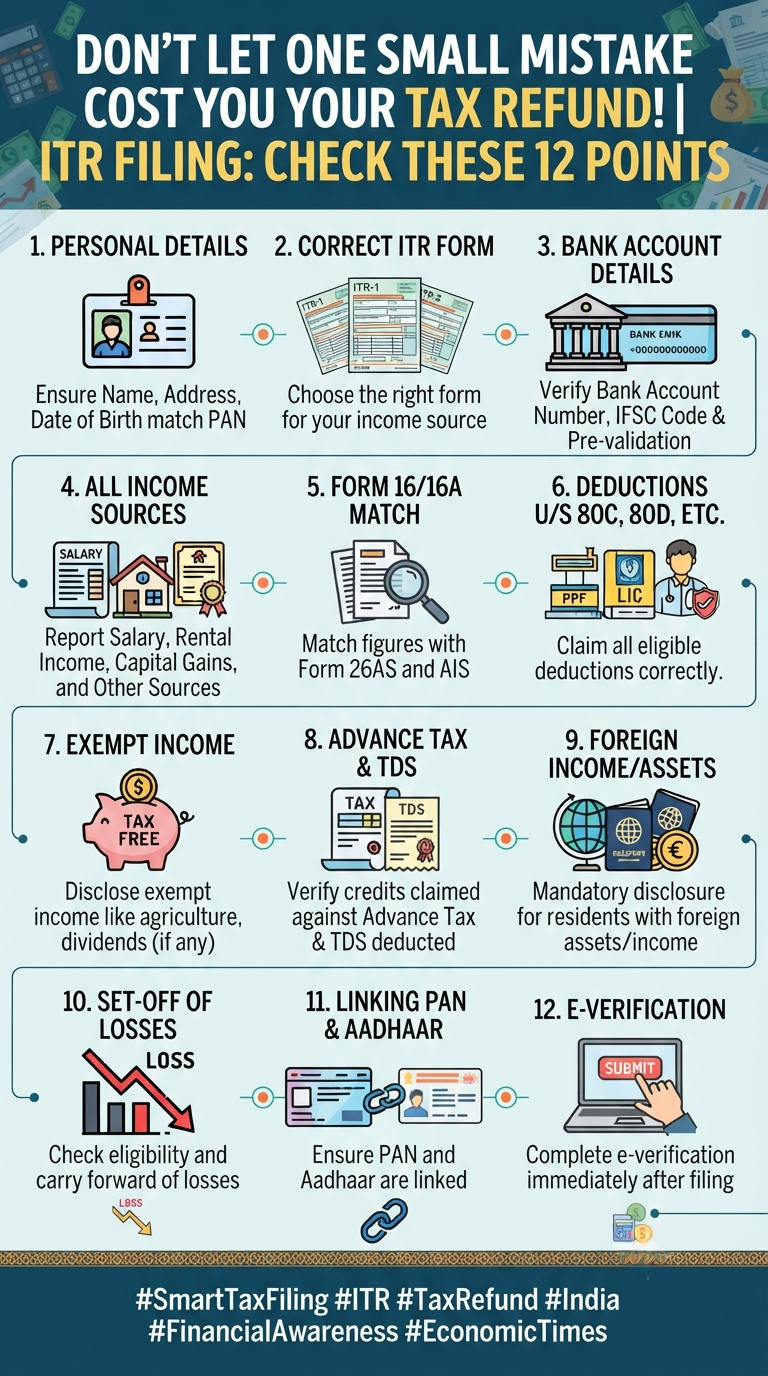

Filing your Income Tax Return (ITR) can often feel like a chore—a necessary evil that we rush through just to get it off our to-do list. But here is the reality: a single typo or a missed detail can be the difference between getting a swift tax refund and getting stuck in a bureaucratic nightmare.…

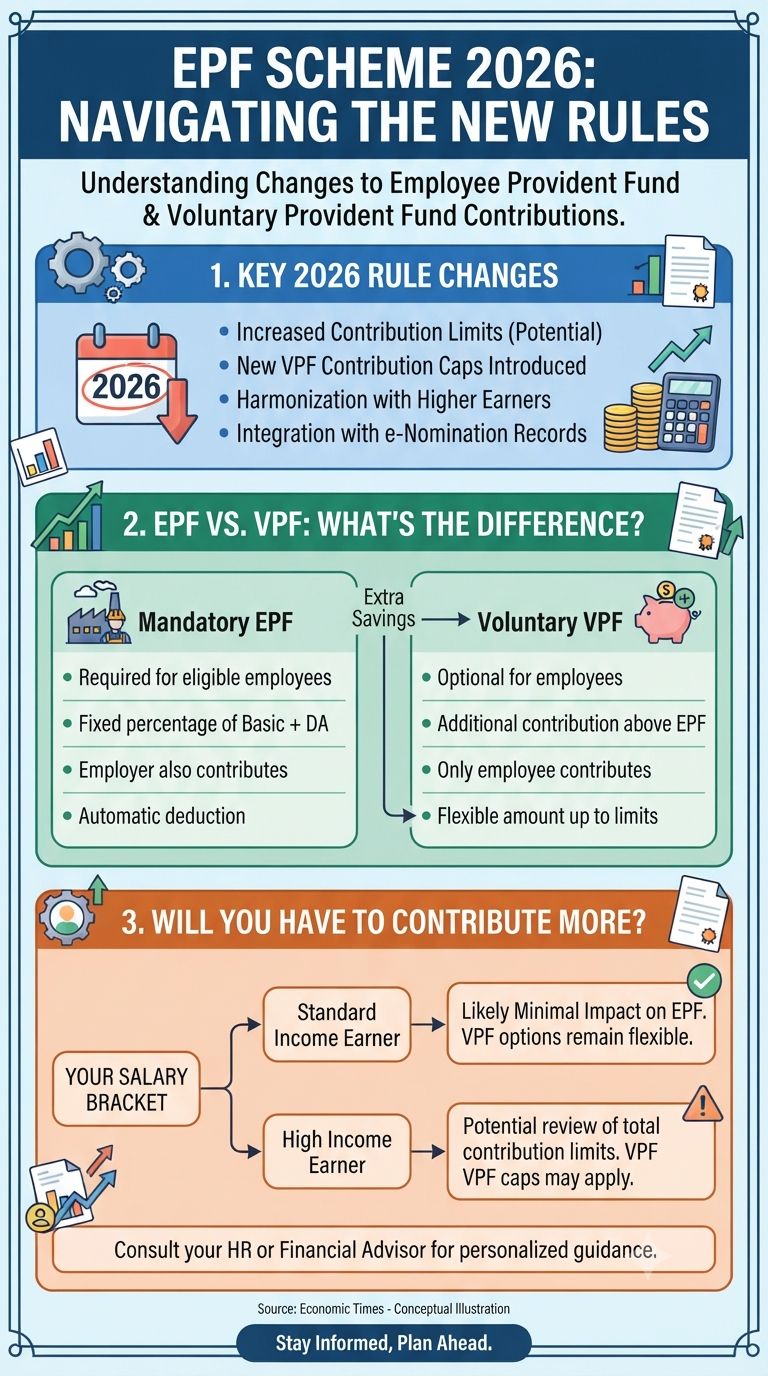

If you’ve been scrolling through financial news lately, you’ve probably noticed the buzz around the “EPF Scheme 2026” updates. It’s the kind of topic that sounds dry until you realize it directly affects how much of your hard-earned money stays in your pocket today versus how much gets tucked away for your future. With the…

Continue Reading EPF Scheme 2026: What the New Rules Actually Mean for Your Paycheck

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.