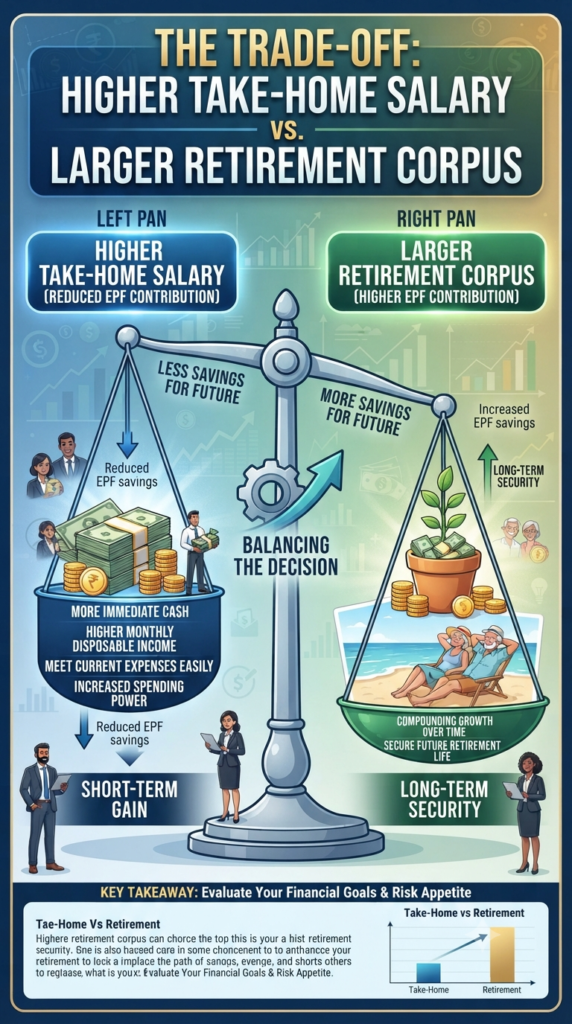

For any salaried professional, that email from HR announcing a salary hike—or better yet, a change that boosts your monthly take-home pay—is usually a cause for celebration. We all love a little extra breathing room in our monthly budget to cover rising costs, splurge on a vacation, or simply enjoy a higher standard of living right now.

But what if that “raise” came with a hidden price tag—one that might cost you a small fortune in the long run?

A new government proposal regarding the Employees’ Provident Fund (EPF) is making waves, suggesting that contributions above the statutory wage ceiling (₹15,000) could become voluntary. On the surface, it sounds like financial freedom. But as is often the case in personal finance, the devil is in the details.

The Temptation: Immediate Cash Flow

The proposal aims to provide flexibility. If you are currently working for an organization that deducts EPF based on your actual basic salary rather than the government-mandated cap, your monthly PF contribution can be quite hefty.

If this change goes through, you might be given the option to stop those “excess” contributions and keep that money in your pocket instead. For someone earning a higher basic salary, this could translate to a significant bump in take-home pay every single month. It’s tempting, right? Who wouldn’t want an extra ₹5,000 or ₹10,000 in their bank account today?

The Hidden Trap: The Power of Compounding

Before you rush to sign up for a smaller PF deduction, take a moment to look at the other side of the balance scale.

EPF isn’t just a tax-saving tool; it is a long-term wealth engine. When you contribute to your EPF, you are benefiting from the magic of compounding combined with government-backed safety and tax-free interest. By opting for a higher take-home salary, you are essentially “consuming” your future retirement wealth today.

Experts have crunched the numbers: reducing your monthly contribution by even a few thousand rupees can lead to a gap of lakhs, or even crores, by the time you retire. If you are in your 20s or 30s, the “cost” of that extra monthly cash is amplified by decades of lost compounding. That “vacation money” today could have been your “financial independence money” tomorrow.

What About Your Pension?

A common fear is that lower EPF contributions will result in a lower monthly pension (EPS) after retirement. The good news? For most employees, this won’t be the case. Your pensionable salary is already capped at the statutory limit, so your future pension eligibility typically remains intact even if you tweak your voluntary contributions.

The real casualty here isn’t your pension—it’s your wealth corpus.

The Verdict: Look Beyond the Paycheck

Is this proposal a good thing? It depends on your financial discipline.

If you are the type of person who will take that extra monthly cash and invest it in high-performing assets (like mutual funds or stocks) that offer better long-term returns than the EPF, this new flexibility might actually be an opportunity to grow your wealth faster.

However, if that extra cash is simply going to vanish into daily expenses or lifestyle inflation, you are effectively choosing a slightly more comfortable “now” at the expense of a significantly more fragile “later.”

Our advice: Before you change your contribution settings, pull out a calculator. Ask yourself: Am I trading a few thousand rupees today for a massive hole in my retirement savings tomorrow? Sometimes, the smartest financial move is the one that keeps you from touching your own future.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always consult with a financial advisor before making significant changes to your retirement planning.

Planning for your child’s future is perhaps the most important financial responsibility a parent carries. Whether it is dreaming about her higher education in a top-tier university or ensuring her wedding is everything she wished for, the math can sometimes feel overwhelming. But what if there was a government-backed “secret weapon” designed specifically to help…

Continue Reading The Secret to Building a Rs 50 Lakh Corpus for Your Daughter’s Future

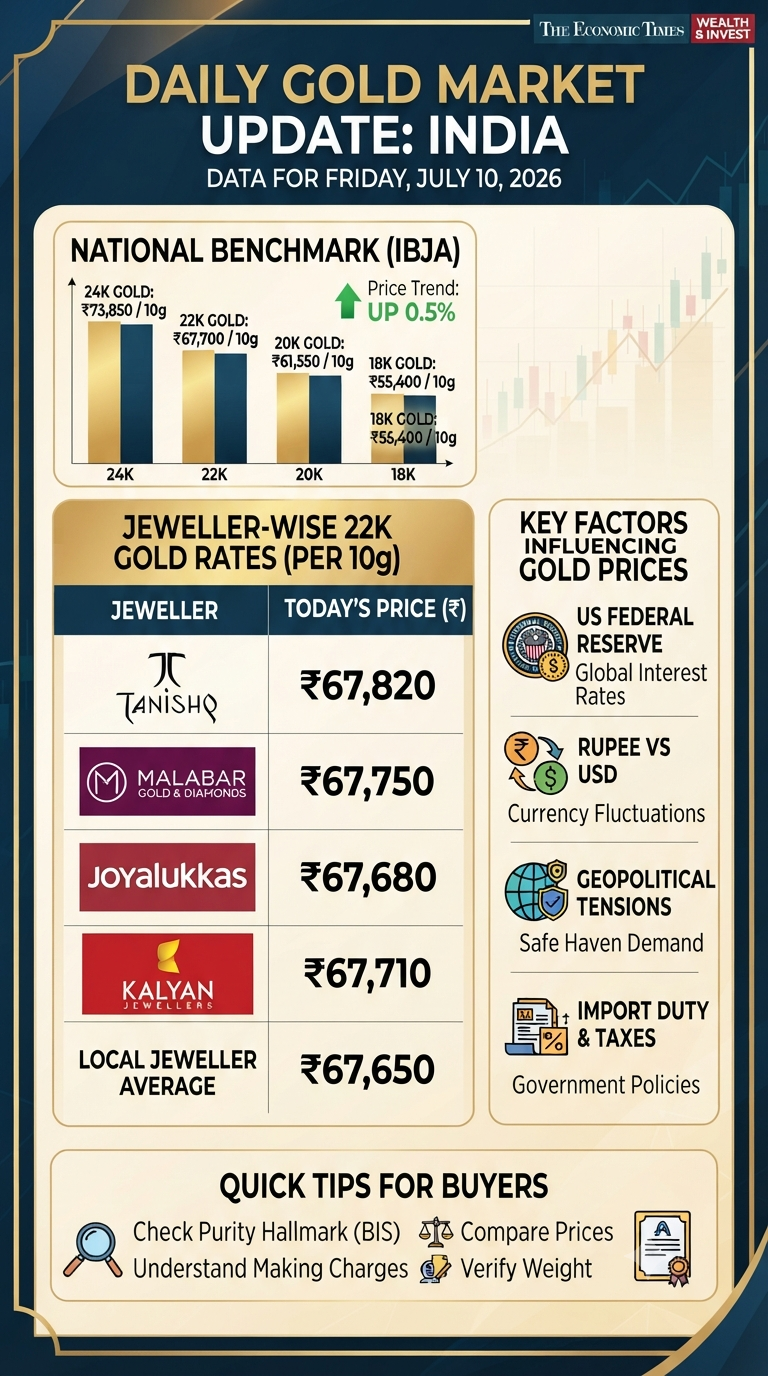

If you’ve been keeping an eye on the markets lately, you know that gold isn’t just a shiny accessory—it’s the heartbeat of Indian investment. Whether you are planning for a wedding, looking for a festive gift, or simply bolstering your portfolio, staying updated on daily price shifts is essential. As of today, Friday, July 10,…

Continue Reading Decoding Today’s Gold Rush: A Buyer’s Guide to Navigating the Market

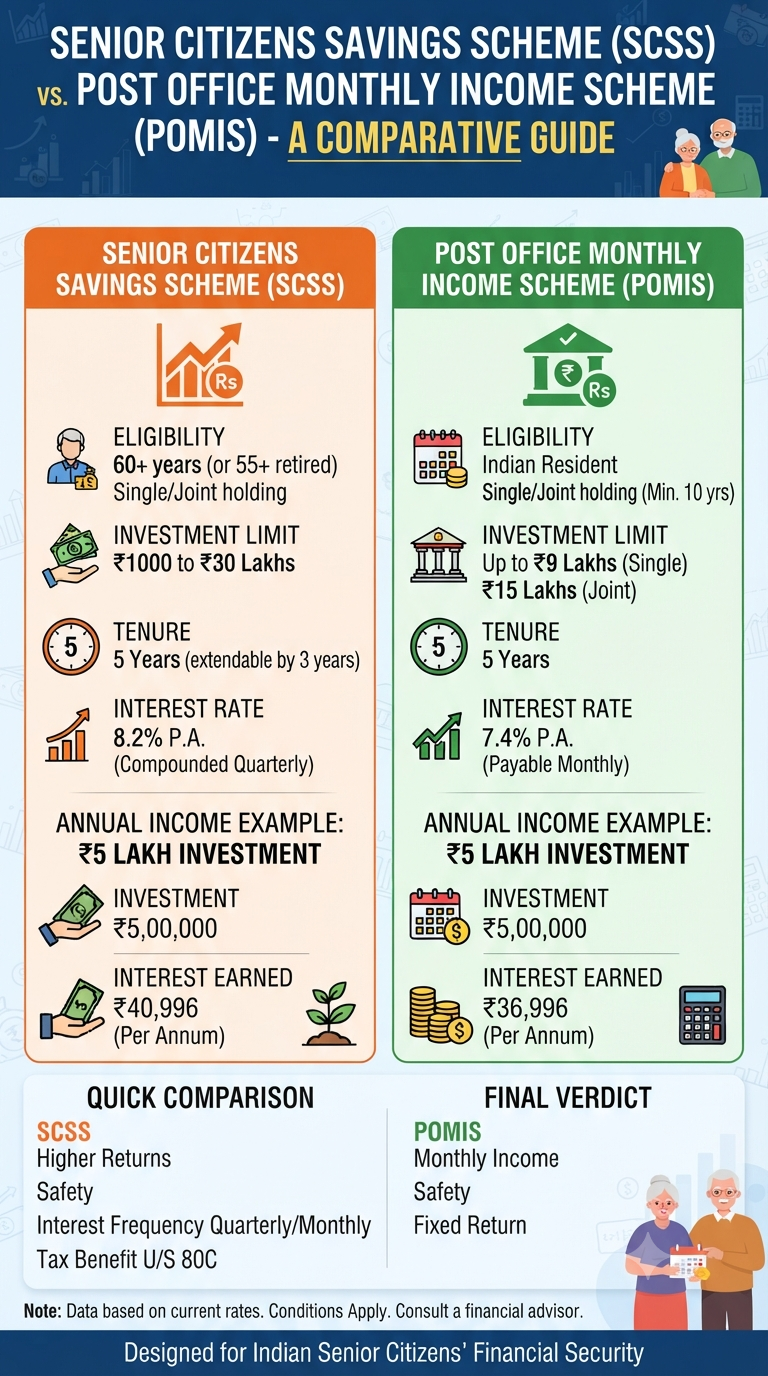

If you are looking for a safe, government-backed harbor for your hard-earned money, the Senior Citizens Savings Scheme (SCSS) and the Post Office Monthly Income Scheme (MIS) are likely at the top of your list. They offer peace of mind, stability, and the reliability of a sovereign guarantee. But when it comes to maximizing your…

Let’s be honest. Most of us know EPF stands for Employees’ Provident Fund, and we know a chunk of our salary goes into it every month. But how many of us actually know exactly how much is in that corpus, or—more importantly—if that promised 8.25% interest has hit our account yet? If you’ve been meaning…

Continue Reading Checkmate Your PF Status: 4 Simple Ways to View Your EPF Balance Right Now

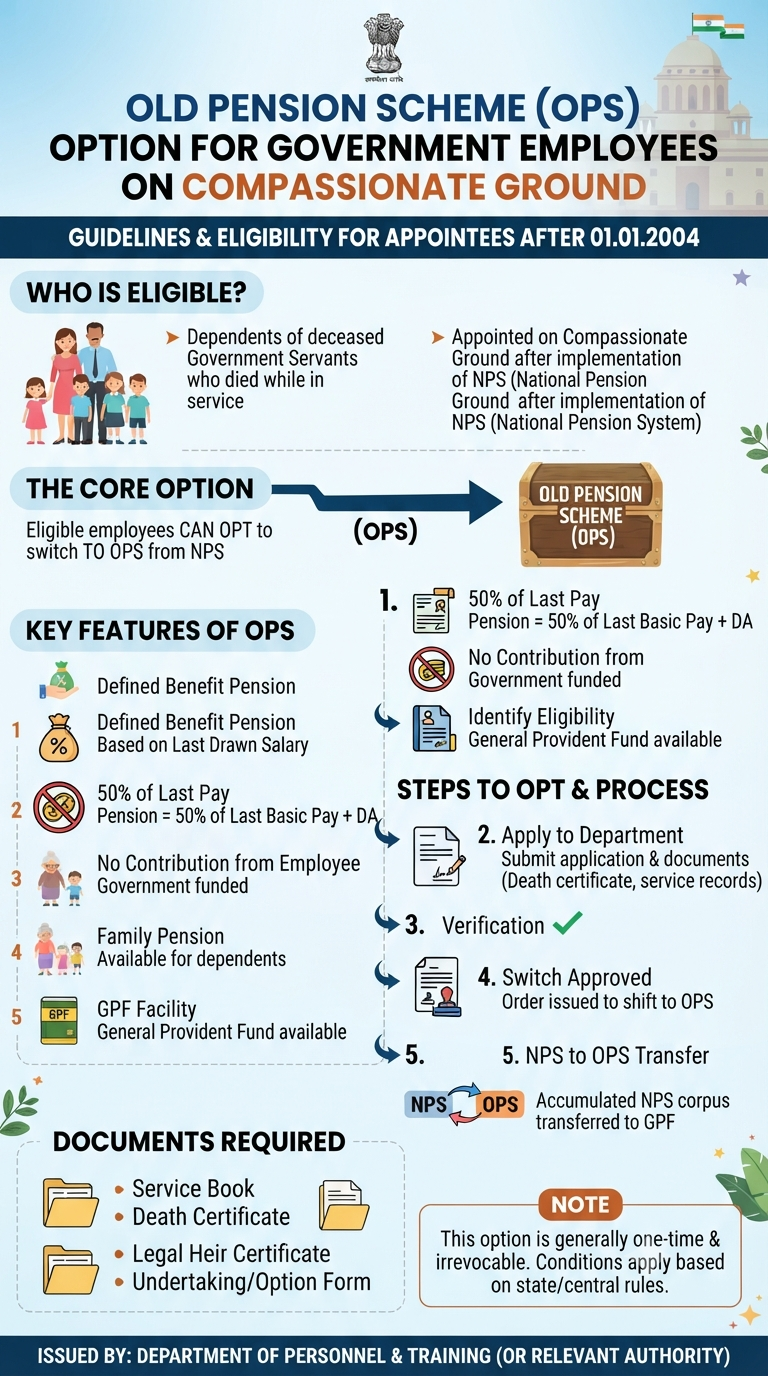

For thousands of government employees who entered service through the compassion of a family-related appointment, the transition into their careers was often marked by a bureaucratic “what-if.” Many had applied for their positions before the cutoff of December 2003, only to join service after the National Pension System (NPS) had already taken hold in January…

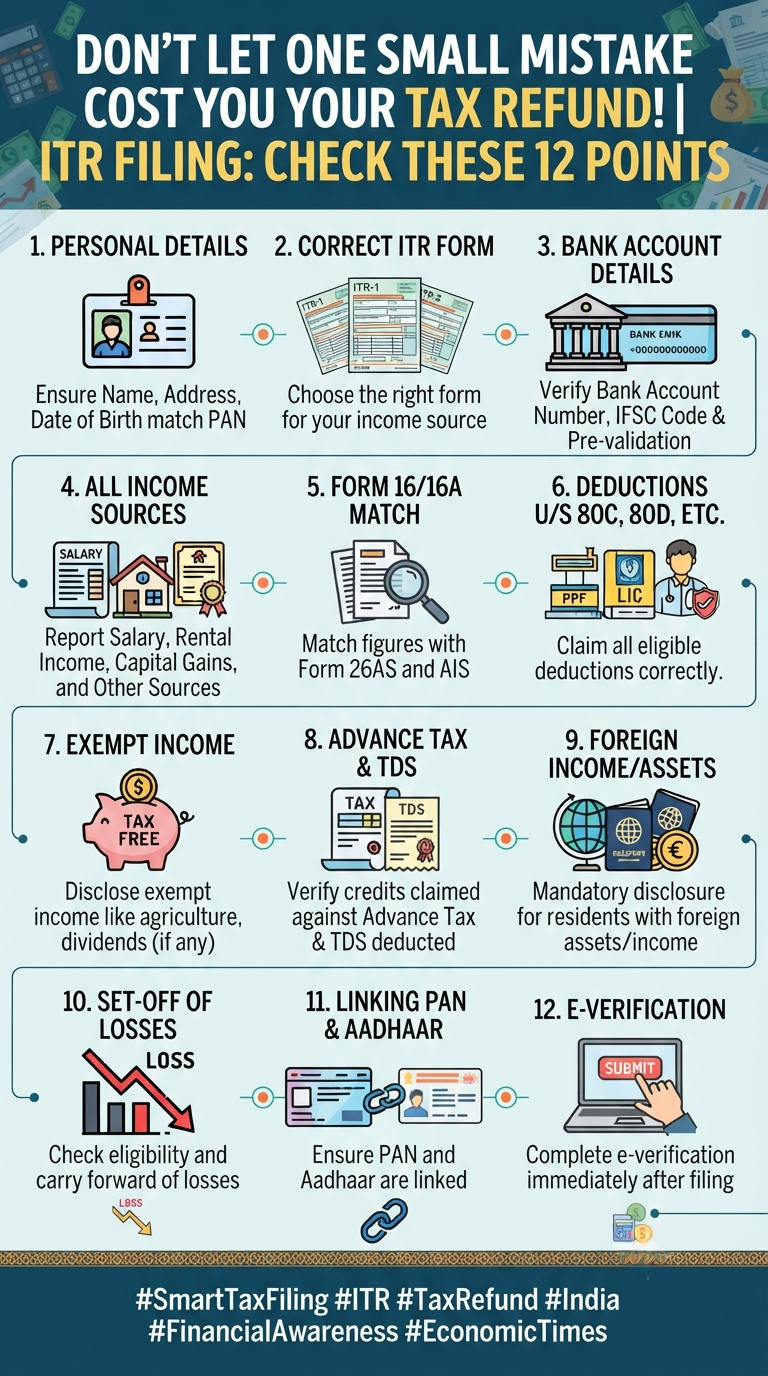

Filing your Income Tax Return (ITR) can often feel like a chore—a necessary evil that we rush through just to get it off our to-do list. But here is the reality: a single typo or a missed detail can be the difference between getting a swift tax refund and getting stuck in a bureaucratic nightmare.…

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.