Planning for a child’s future is arguably the most important responsibility any parent takes on. As we watch them grow, the dream of providing them with the best education or a stress-free start to adulthood becomes our North Star. But in the world of financial planning, the question inevitably arises: Where should I put my money?

When it comes to securing your daughter’s financial foundation, two options usually top the list: the Sukanya Samriddhi Yojana (SSY) and the traditional Fixed Deposit (FD). Both are safe, but they serve very different purposes. Let’s break it down to see which one aligns with your family’s journey.

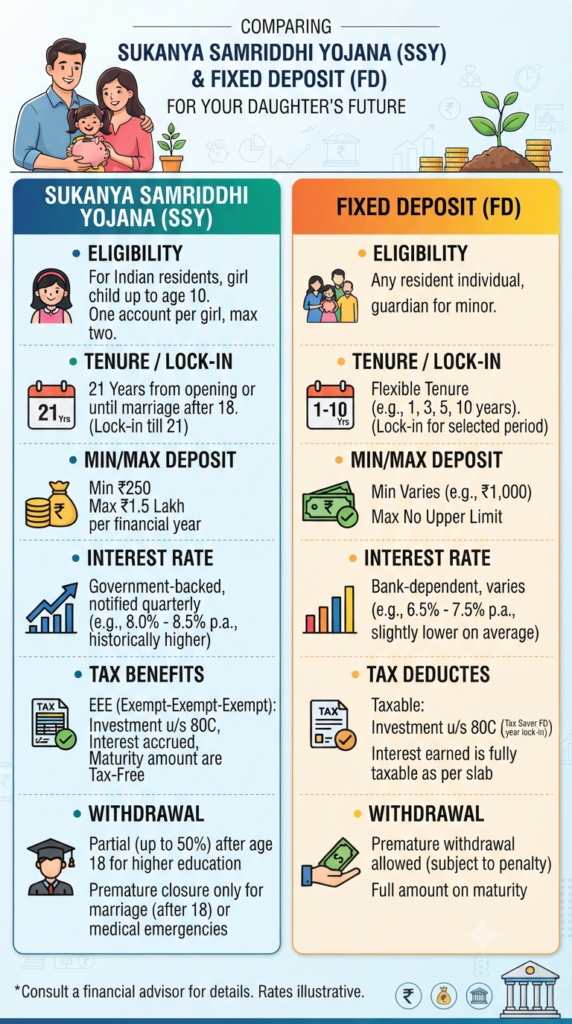

The Power of Government Backing: Sukanya Samriddhi Yojana

If you have a daughter under the age of 10, the SSY is arguably the gold standard for long-term saving. Introduced as part of the “Beti Bachao, Beti Padhao” campaign, it is designed specifically for a girl child’s future.

- The Advantage: It offers higher interest rates compared to most bank instruments, and because it’s government-backed, the risk is virtually non-existent.

- The “Triple Tax” Benefit: This is the real game-changer. You get tax benefits under Section 80C on your investment, the interest earned is tax-free, and the final maturity amount is completely tax-exempt. It’s a rare “Triple-E” (Exempt-Exempt-Exempt) instrument that keeps more money in your pocket.

- The Trade-off: The “lock-in” is real. Your money stays invested until your daughter turns 21 (or reaches her wedding date after 18). It isn’t for quick access; it’s a marathon strategy.

The Reliable Classic: Fixed Deposits (FD)

Fixed Deposits have been the bedrock of Indian savings for generations. They are straightforward, reliable, and incredibly easy to manage.

- The Advantage: Flexibility is the name of the game. If you need money for school fees next year, or perhaps a sudden family expense, an FD allows you to withdraw (often with a small penalty). You choose the tenure that suits you, whether it’s six months or ten years.

- The Reality Check: While FDs are safe, the interest you earn is taxable. Depending on your income tax slab, that annual “growth” might be eaten away by taxes, making the post-tax return look less attractive than the SSY.

Which Path Should You Choose?

Think of your goals in terms of Time and Need:

- Choose SSY if: You are looking 10–15 years into the future. You want to build a substantial corpus for your daughter’s higher education or wedding, and you want to maximize your returns without worrying about the ups and downs of the market or tax implications.

- Choose FD if: You value liquidity. If you’re saving for intermediate costs—like recurring tuition fees or a specific short-term goal—the FD gives you the peace of mind that your money is accessible when you need it most.

The Bottom Line

There is no “better” option in a vacuum—only the right option for your specific plan. Many parents choose a hybrid approach: they max out the SSY for the long-term, high-interest tax-free growth, and keep a smaller, liquid bucket in FDs for those unpredictable “life happens” moments.

Ultimately, the best investment you can make is the one you start today. Your daughter’s future is waiting—what will your first step be?

Big News for Your Retirement Fund: 8.25% Interest Coming Your Way!

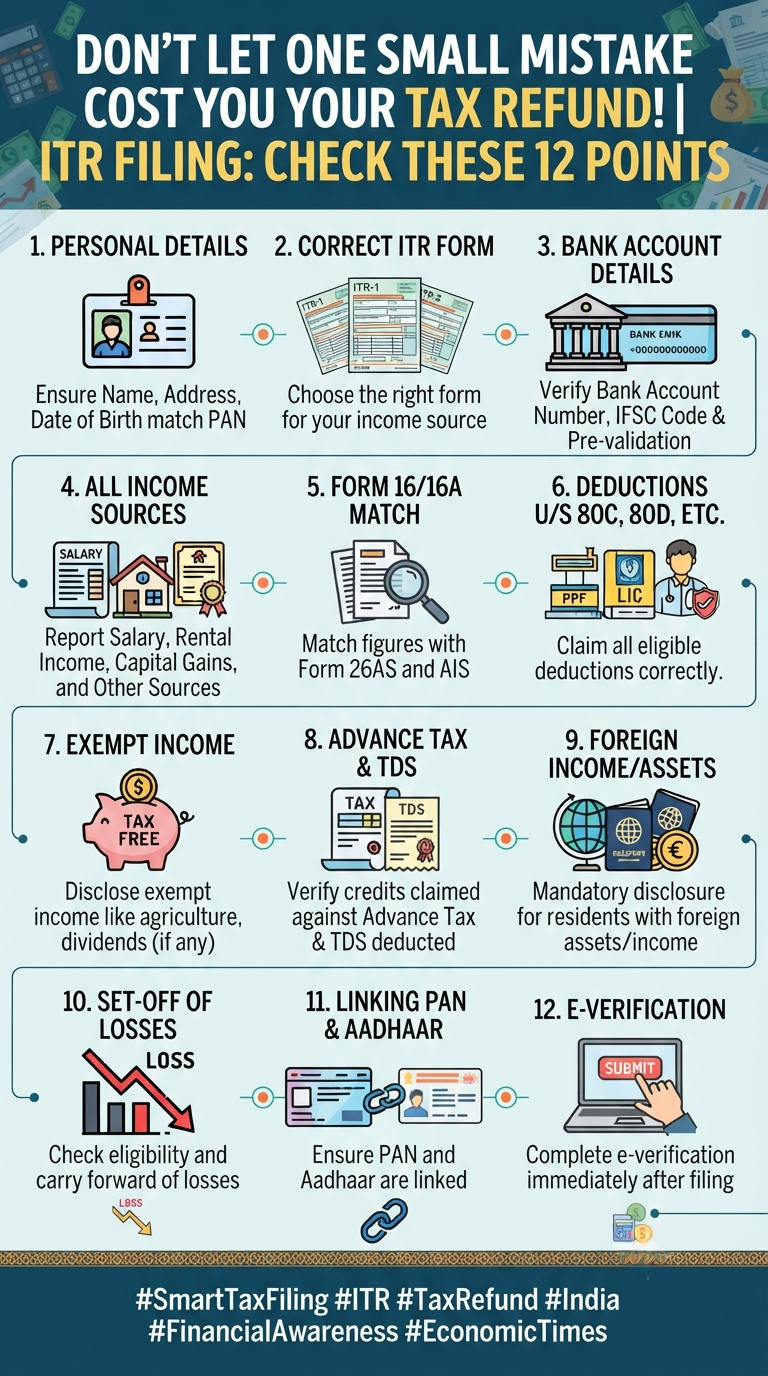

Filing your Income Tax Return (ITR) can often feel like a chore—a necessary evil that we rush through just to get it off our to-do list. But here is the reality: a single typo or a missed detail can be the difference between getting a swift tax refund and getting stuck in a bureaucratic nightmare.…

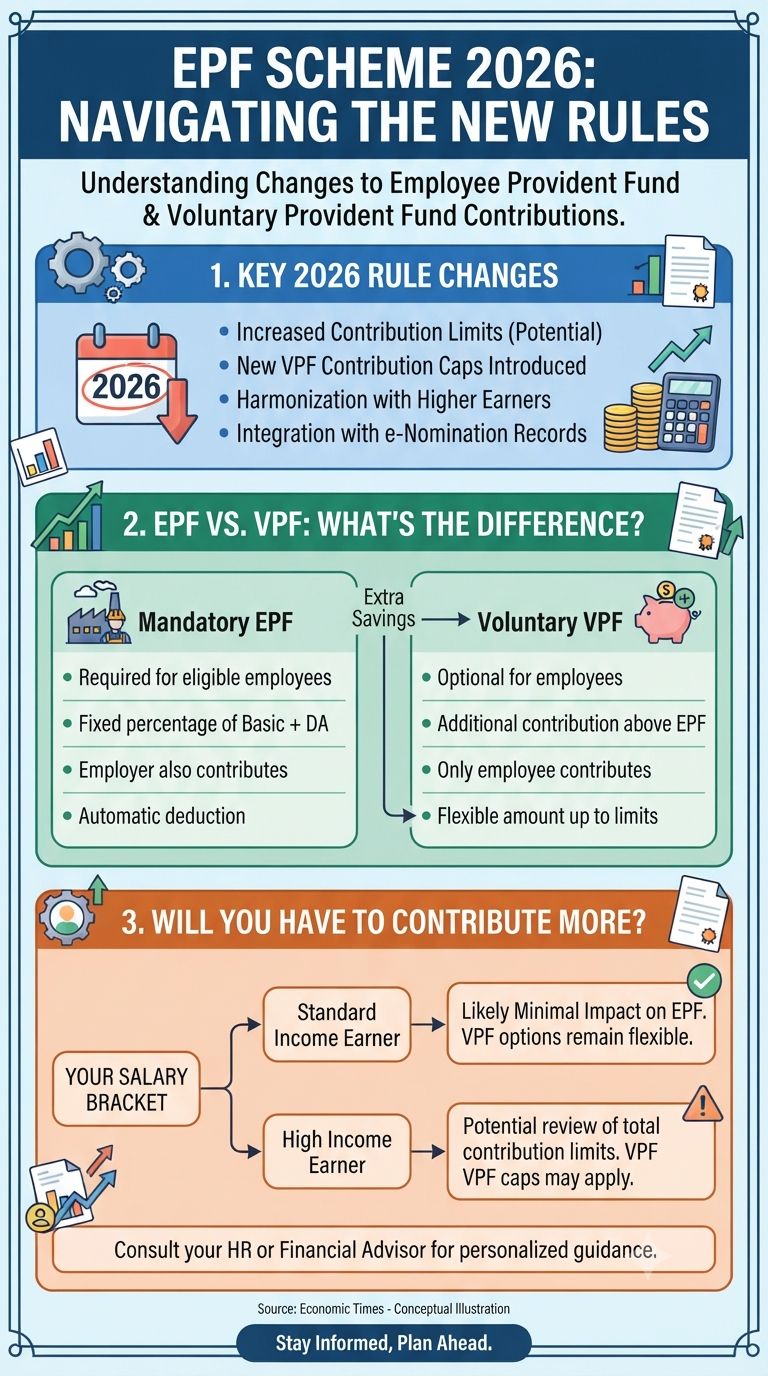

If you’ve been scrolling through financial news lately, you’ve probably noticed the buzz around the “EPF Scheme 2026” updates. It’s the kind of topic that sounds dry until you realize it directly affects how much of your hard-earned money stays in your pocket today versus how much gets tucked away for your future. With the…

Continue Reading EPF Scheme 2026: What the New Rules Actually Mean for Your Paycheck

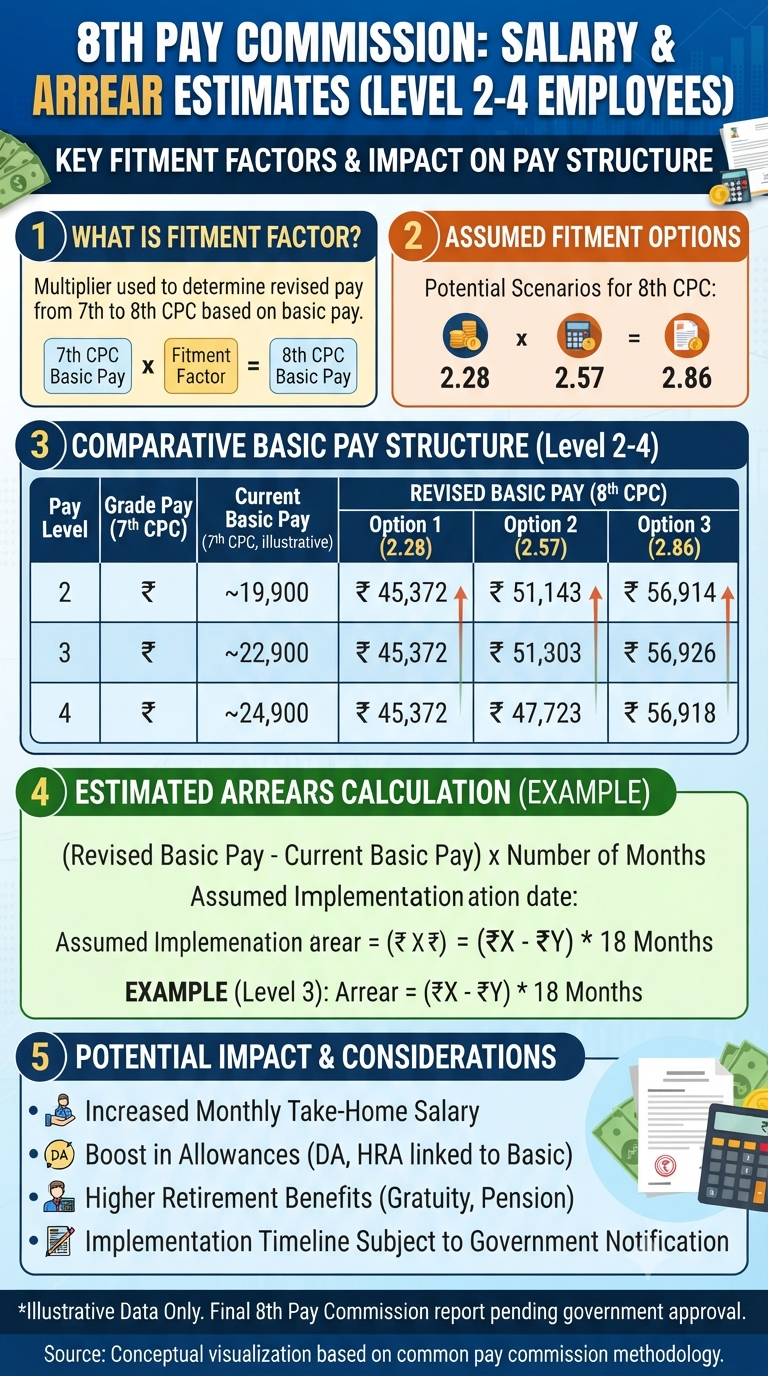

As the conversation around the 8th Pay Commission gains momentum, central government employees—particularly those in Pay Levels 2 through 4—are understandably eager to know what the future holds for their salary structures. While the official report is still in the works, the speculation surrounding the “fitment factor” has become the talk of the town. Understanding…

Continue Reading The 8th Pay Commission Buzz: What Could It Mean for Your Paycheck?

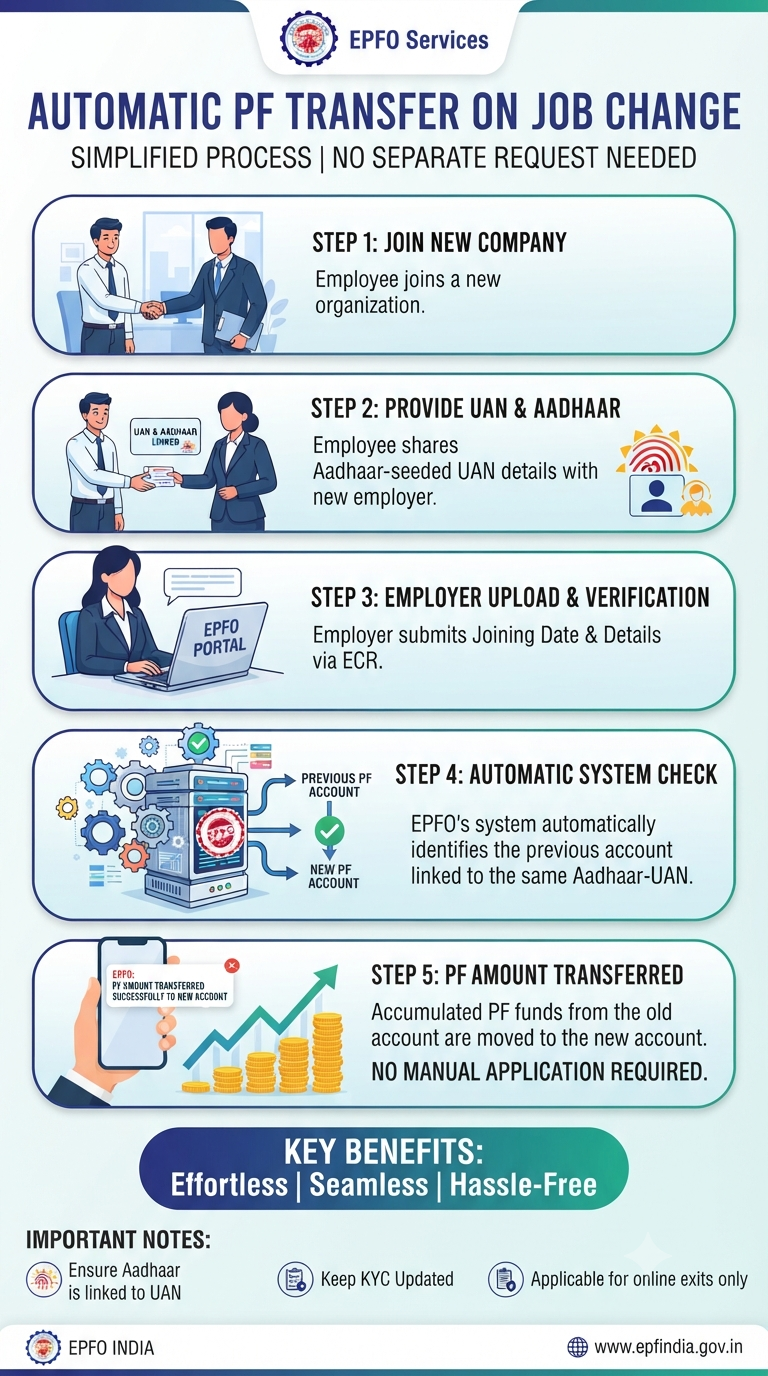

Are you one of those people who cringes at the thought of switching jobs simply because of the paperwork nightmare that follows? We’ve all been there—the endless forms, the back-and-forth between the old HR and the new, and the agonizing wait for your hard-earned PF (Provident Fund) balance to migrate to your current account. Well,…

Continue Reading Say Goodbye to the Hassle: EPFO Automates PF Transfers for Aadhaar-Linked Accounts!

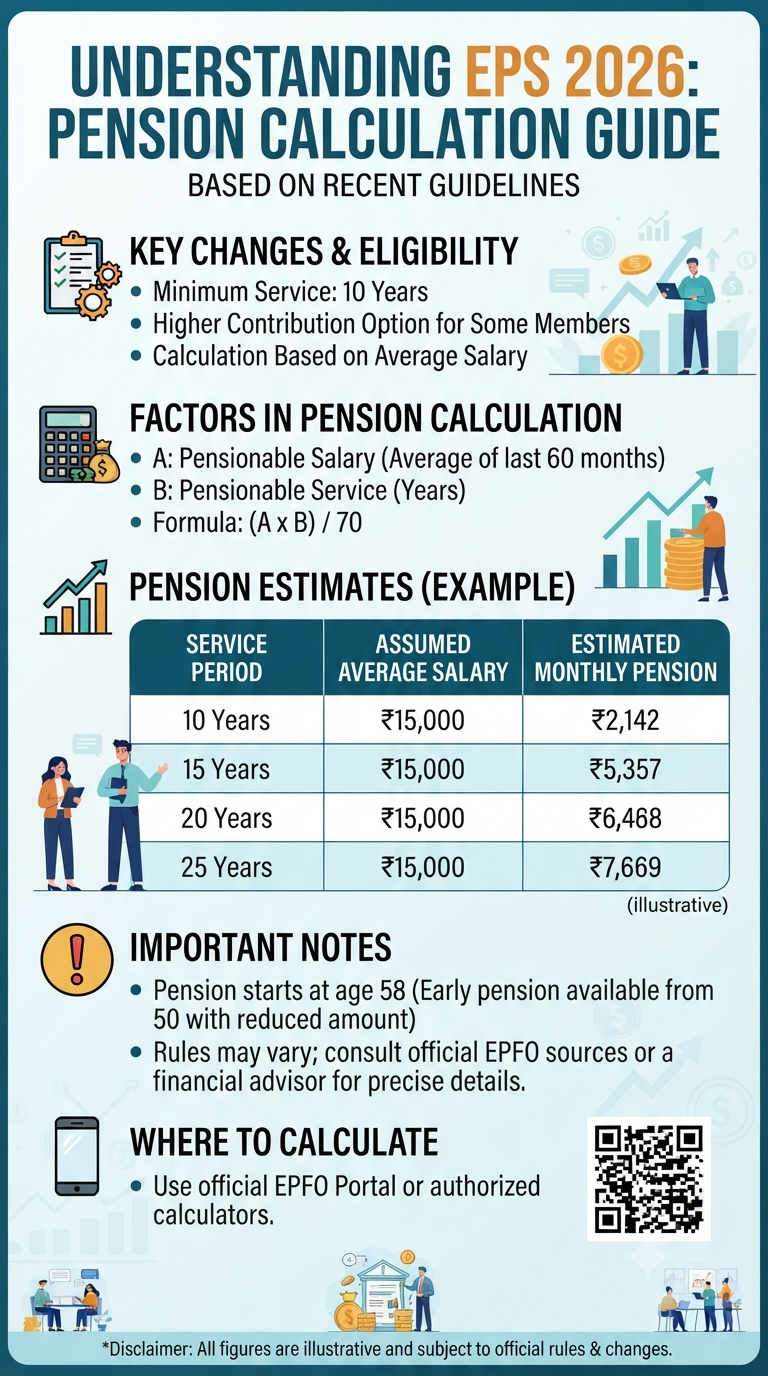

If you have been keeping up with financial news, you might have heard about the transition to the Employees’ Pension Scheme (EPS) 2026 under the Code on Social Security, 2020. With any big regulatory shift, it is natural to wonder: Has everything changed? The good news is that when it comes to your monthly pension,…

Continue Reading Demystifying EPS 2026: What You Need to Know About Your Pension

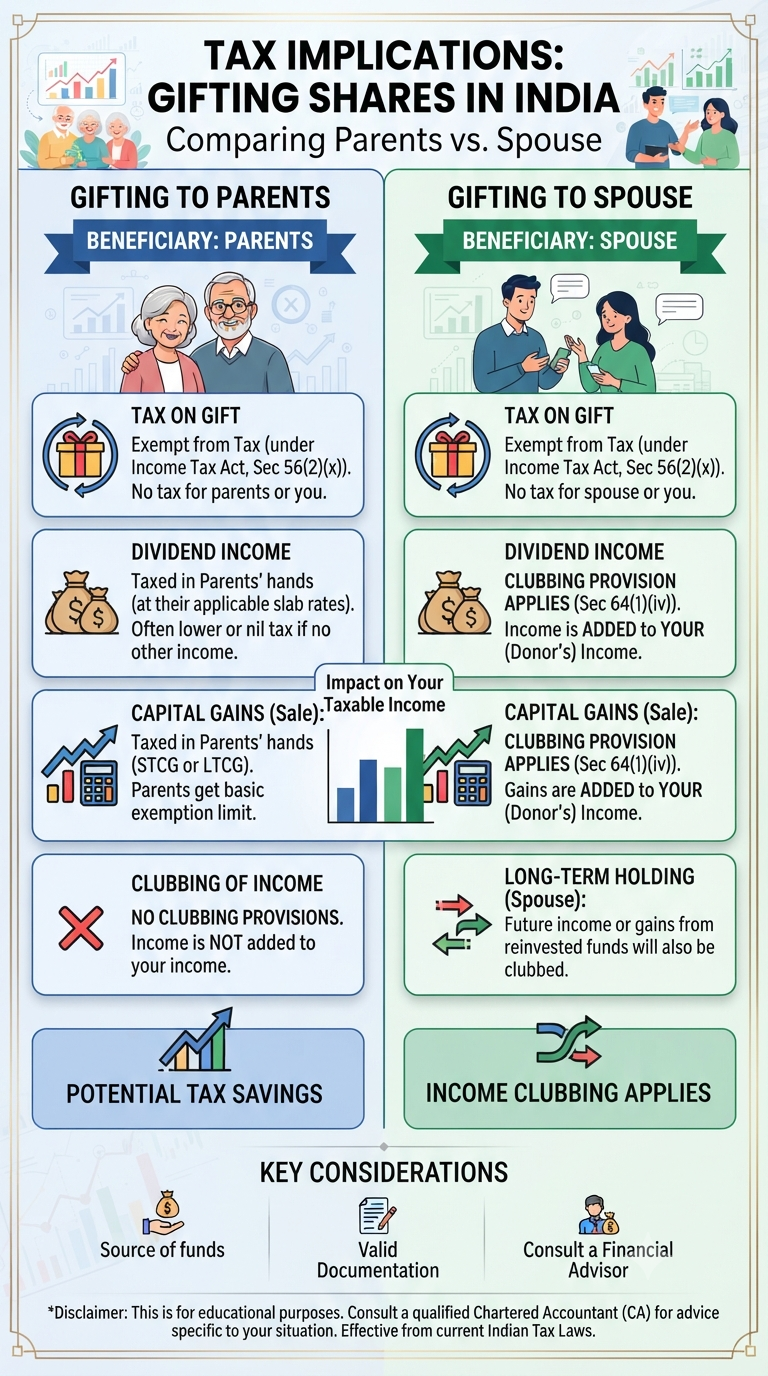

We all love to give back to our families. Whether it’s a surprise gift for a birthday or a gesture of appreciation, the intent is usually rooted in love. But what if that gift could also be a strategic move that saves your family thousands in taxes? When it comes to gifting shares, it turns…

Continue Reading The Art of Gifting Shares: Why Your Parents Are Your Best Tax-Planning Partners

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.