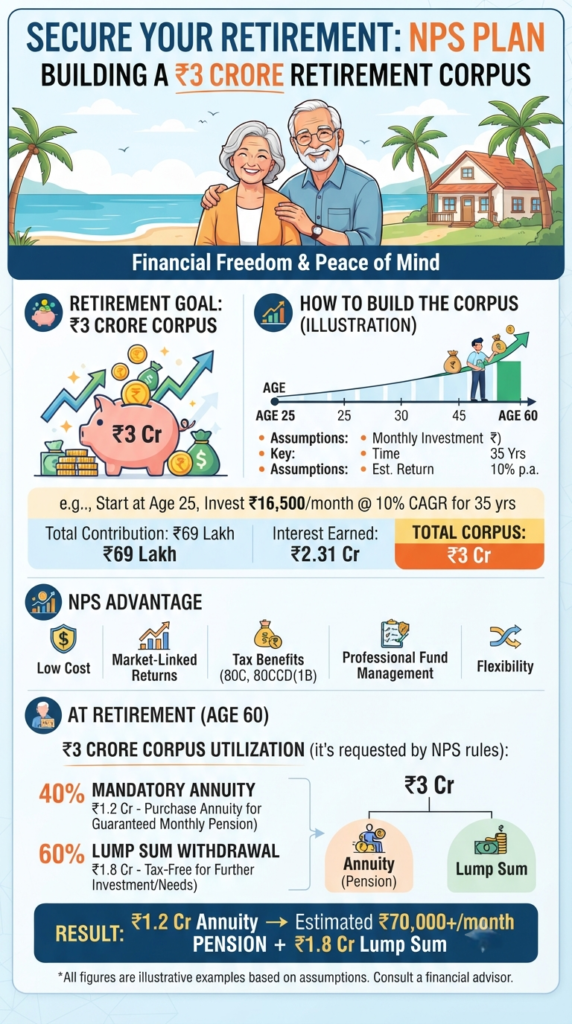

Retirement often feels like a distant milestone—something to worry about “later.” But what if you could visualize that “later” right now? Imagine hitting age 60 with a solid ₹3 crore corpus. It’s not just a number on a screen; it’s the key to your financial independence, the bridge to your passions, and the ultimate safety net.

If you’ve been wondering how to make that vision a reality using the National Pension System (NPS), let’s break it down into something actionable, human, and—dare we say—exciting.

The Power of Starting Early

Building a ₹3 crore corpus doesn’t require winning the lottery. It requires the quiet, unstoppable power of compounding. Think of it as planting a tree; the best time was years ago, but the second-best time is today.

If you start your journey at age 25, consistently investing ₹16,500 every month for 35 years at an estimated 10% annual return, you aren’t just saving money—you’re engineering your future. By age 60, your contributions of ₹69 lakh could blossom into a massive ₹3 crore kitty, thanks to the magic of long-term market growth.

Why NPS is a Smart Move

The NPS isn’t just another investment vehicle; it’s a disciplined financial partner. Here’s why it deserves a spot in your portfolio:

- Cost-Efficiency: It’s one of the most low-cost investment options available in India.

- Professional Expertise: Your money is managed by experienced pension fund managers.

- Tax Efficiency: With benefits under Section 80C and 80CCD(1B), you’re saving on taxes while building your wealth.

- Flexibility: You have the freedom to choose your asset allocation (equity vs. debt) based on your risk appetite.

Life at 60: The “Payday” Phase

So, you’ve reached the big 6-0, and you’re staring at that ₹3 crore corpus. Now what? NPS rules provide a structured way to ensure you never run out of money:

1. The Tax-Free Lump Sum (60%)

You can withdraw ₹1.8 crore immediately. This is your “freedom fund.” Use it to pay off the mortgage, renovate your home, fund a bucket-list trip, or reinvest for your family’s future. The best part? It’s tax-free.

2. The Guaranteed Monthly Pension (40%)

The remaining ₹1.2 crore is parked into an annuity, which acts as your personal “salary” for life. Depending on the annuity rates at the time, this portion can generate a steady, monthly pension of ₹70,000 or more.

Imagine the peace of mind knowing that every single month, a consistent amount hits your bank account—no matter what the market is doing. That is the definition of true retirement security.

The Bottom Line

Retirement planning isn’t about sacrificing today for tomorrow; it’s about ensuring that your “tomorrow” is just as vibrant and comfortable as your “today.” A ₹3 crore goal is ambitious, but entirely achievable with consistency and the right strategy.

Whether you’re starting with your first paycheck or accelerating your investments in your 40s, the path is clear. Why wait for retirement to start living? Start building your legacy today.

Disclaimer: All figures mentioned are illustrative examples based on specific assumptions. Market investments are subject to risk. Please consult with a qualified financial advisor before making any major investment decisions.

The Illusion of Choice: Are You Trapped in the Mutual Fund Overlap Web?

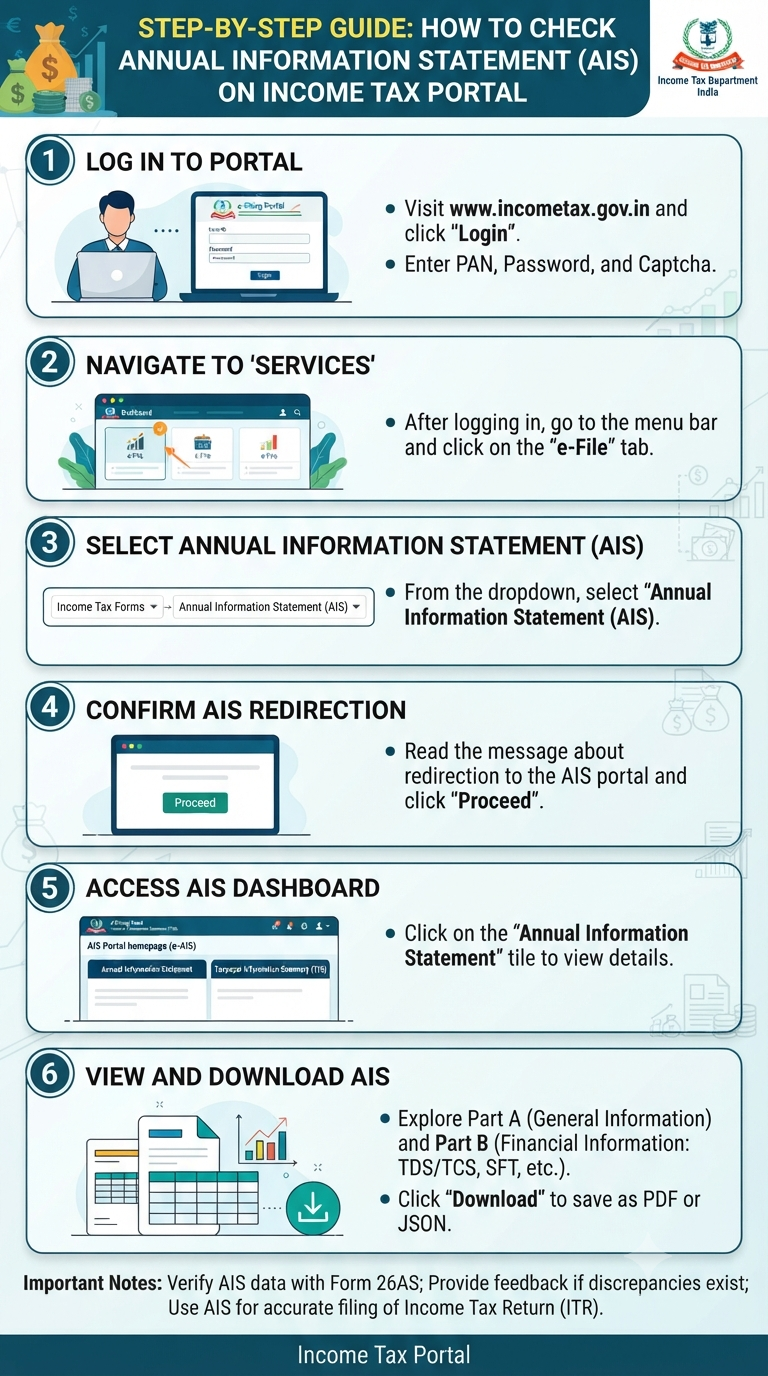

Filing your Income Tax Return (ITR) is one of those annual financial chores that often feels daunting. We scramble for Form 16s, look for investment proofs, and hope we haven’t missed anything. But what if there was a “cheat sheet” that held nearly all the information the Income Tax Department already has about your financial…

Continue Reading Why Your Annual Information Statement (AIS) is Your Best Friend Before Filing ITR

You’ve done your homework. You’ve read the financial news, listened to the podcasts, and decided it’s time to secure your financial future. To build a robust, resilient portfolio, you adopt a “more is merrier” strategy, buying into several different mutual funds to ensure you are diversified. But here is a hard truth that many investors…

Continue Reading The Illusion of Choice: Are You Trapped in the Mutual Fund Overlap Web?

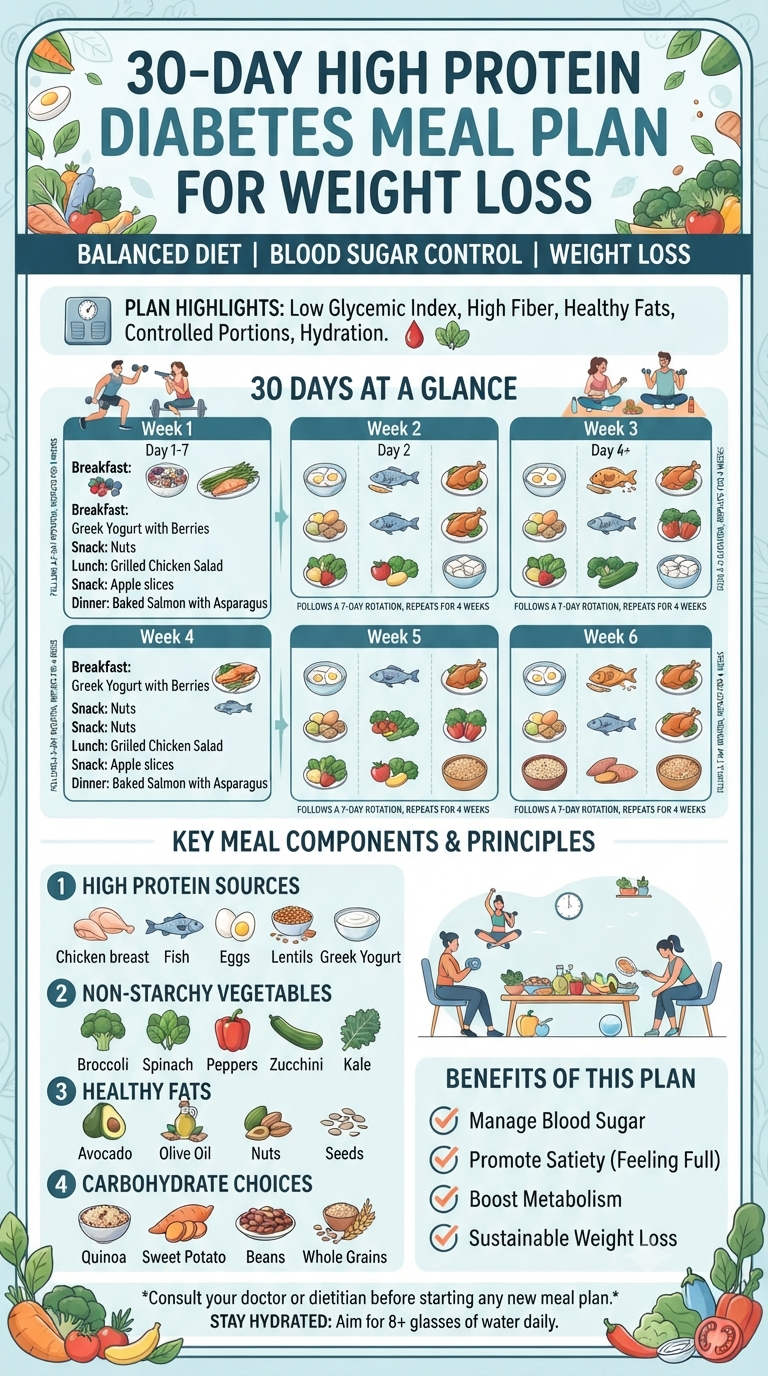

When it comes to health, we’re often bombarded with quick fixes and extreme restrictions. But what if the secret to managing blood sugar and achieving weight loss wasn’t about deprivation, but about intentional, high-protein nourishment? If you’ve been looking for a way to reset your habits without feeling constantly hungry, a high-protein, diabetes-friendly approach might…

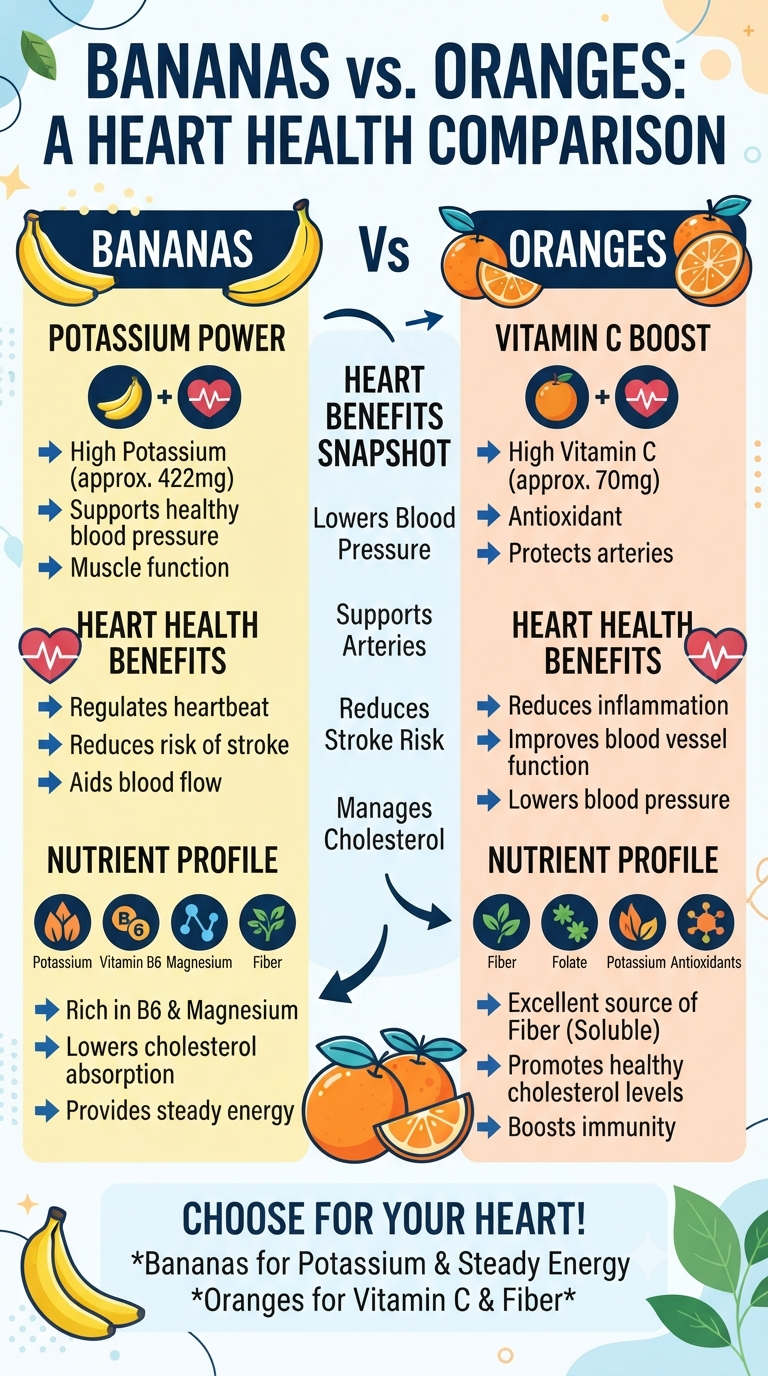

When you’re staring at the fruit bowl wondering which snack will do your heart the most good, it’s easy to feel torn. Do you reach for the convenient banana or the zesty, refreshing orange? Both are nutritional powerhouses, but they bring different strengths to your cardiovascular game. Let’s break down how these two favorites measure…

Continue Reading Heart-Healthy Snacking: The Battle of the Fruits

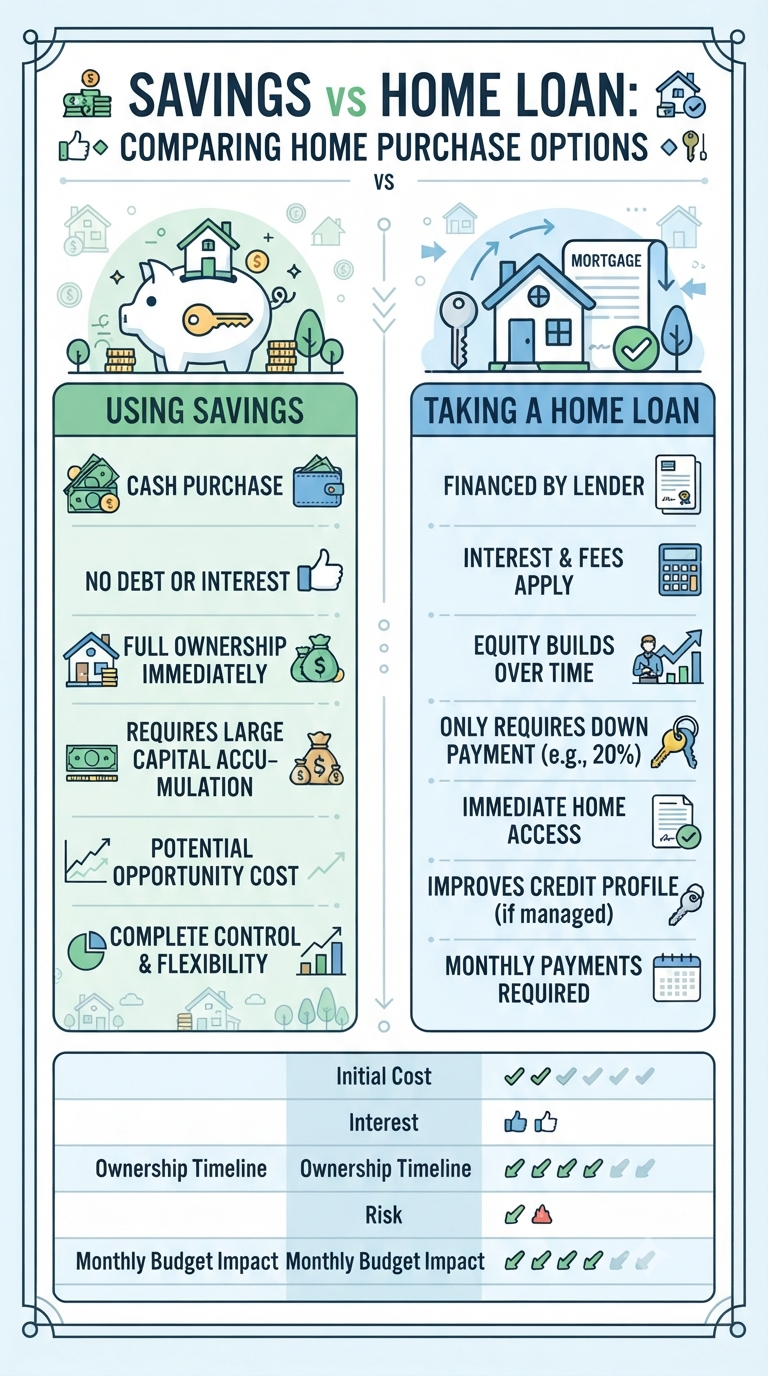

Buying a home is one of life’s biggest milestones. For most people, it’s not just a house—it’s a long-term investment in their future and a place to build a life. But with such a massive price tag, a fundamental question arises: Should I save up and pay cash, or should I take out a home…

Continue Reading The Ultimate Showdown: Is it Better to Buy Your Dream Home with Cash or a Mortgage?

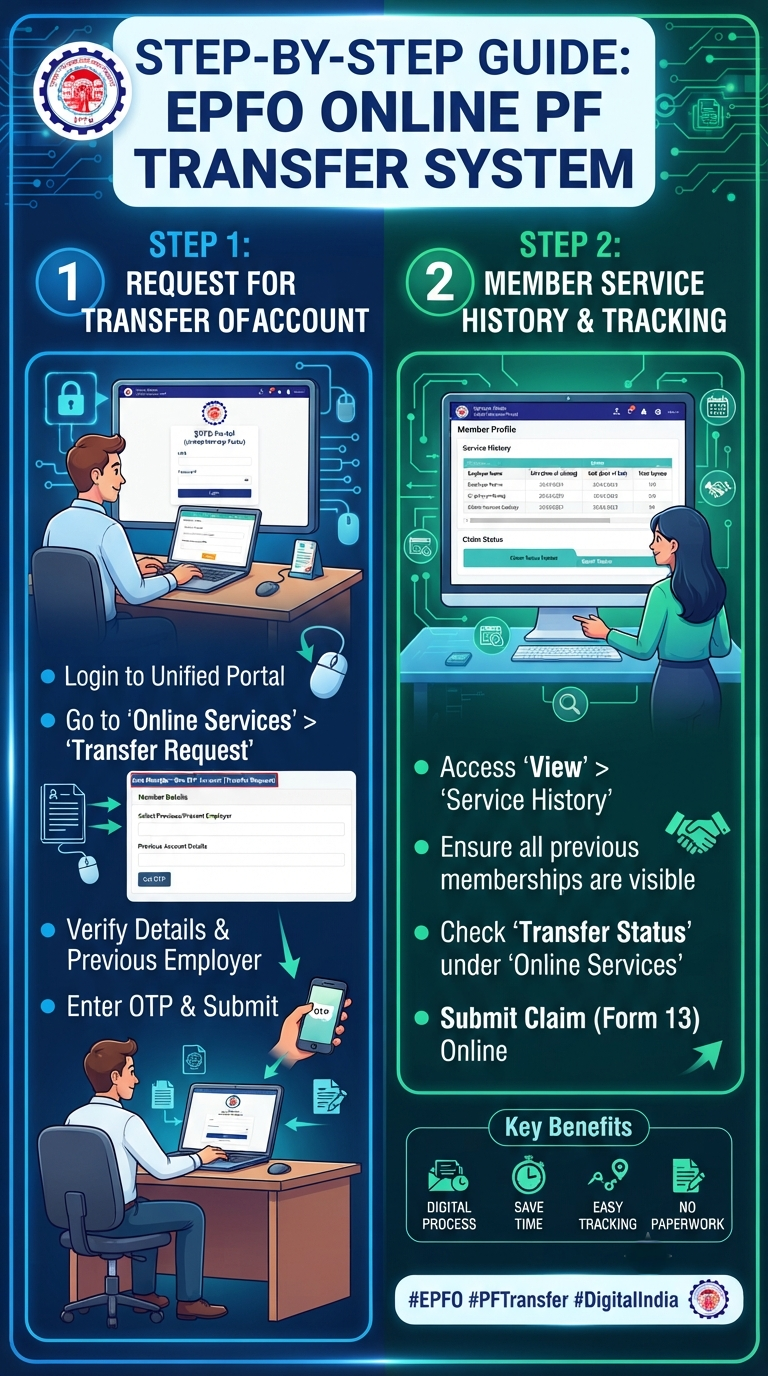

Let’s be honest: tracking down old Provident Fund (PF) accounts from past jobs feels like a chore no one wants to tackle. Between the mountain of forms, the fear of losing service history, and the sheer time it takes, many of us just leave our old accounts sitting idle. But what if you could clean…

Continue Reading Say Goodbye to Paperwork: How to Consolidate Your EPF Accounts Online

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.