Buying a home is one of life’s biggest milestones. For most people, it’s not just a house—it’s a long-term investment in their future and a place to build a life. But with such a massive price tag, a fundamental question arises: Should I save up and pay cash, or should I take out a home loan?

The decision can feel overwhelming. On one hand, the idea of being “debt-free” is incredibly powerful. On the other, using a mortgage allows you to secure a property years, or even decades, sooner.

To help you navigate this monumental financial choice, let’s break down the two paths. We’ll explore the pros, cons, and the real-world impact of using your savings versus a mortgage to achieve homeownership.

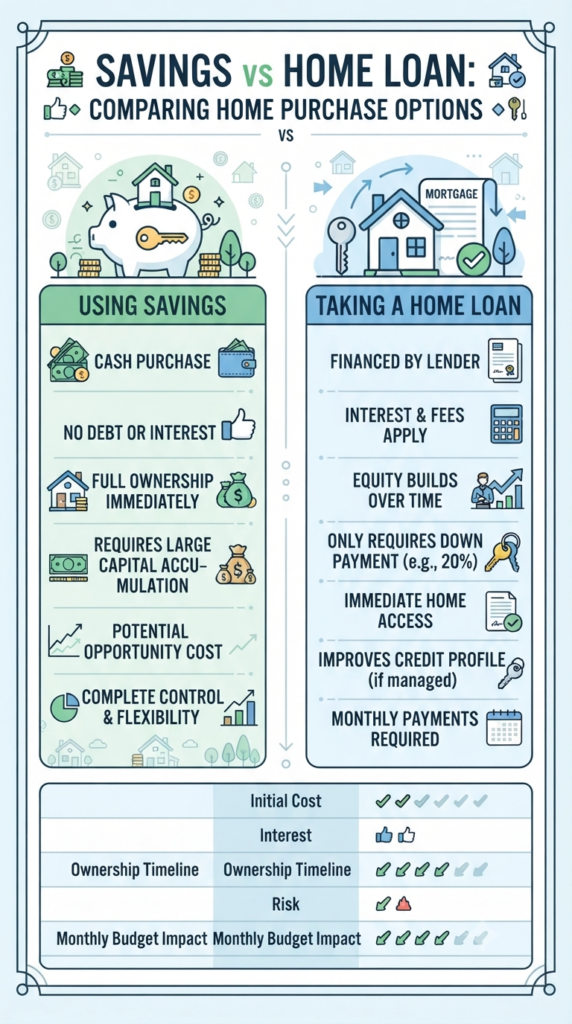

Path 1: The “Pay in Full” Approach (Using Savings)

For disciplined savers, this is the ultimate goal. The allure of handing over cash and immediately owning your home free and clear is undeniable. Let’s look at what this path really involves.

The Good (The Pros)

- Total Financial Freedom: The biggest win is peace of mind. You will never have to worry about foreclosure or a bank repossessing your home because you missed a payment.

- Massive Long-Term Savings: This is the hidden benefit. Because you are not borrowing money, you won’t pay a dime in interest. Over a 30-year term, mortgage interest can easily double the price of your home. By paying cash, you save all of that money.

- Unmatched Flexibility: Without a monthly mortgage payment, your budget is instantly freed up. You can invest more, travel, or save for retirement.

The Bad (The Cons)

- The “Opportunity Cost”: This is the biggest financial sacrifice. The hundreds of thousands of dollars used to buy the house are no longer available to be invested. If that money could have earned a higher return in the stock market, paying cash is actually a “loss” compared to what your money could have done.

- An Astronomical Initial Cost: Unless you live in a very low-cost area, gathering hundreds of thousands of dollars in liquid cash is nearly impossible for most people, especially early in their careers. This path often means renting for decades just to save enough.

Path 2: The Leveraged Approach (Taking a Home Loan/Mortgage)

For the vast majority of buyers, a mortgage isn’t a second choice—it’s the only practical way to become a homeowner. It’s a powerful financial tool that lets you control a valuable asset while paying for it over time.

The Good (The Pros)

- Immediate Home Access: This is the game-changer. Instead of waiting 15–20 years to save enough for a full cash payment, a mortgage lets you get the keys to your home today. You start building equity and living in your dream home now.

- Building Equity Over Time: Your monthly payment isn’t just a fee; it’s a forced savings account. A portion of every payment goes toward the principal balance, slowly building your ownership stake in the property.

- A Potential Credit Boost: If you manage a mortgage responsibly by making all payments on time, it demonstrates excellent financial discipline to lenders. This can improve your credit score, making it easier to borrow for future needs.

The Bad (The Cons)

- Interest and Fees: The convenience of borrowing comes at a high cost. Over the life of the loan, you will pay a significant amount of money in interest to the bank.

- Ongoing Monthly Pressure: A mortgage is a non-negotiable, long-term debt obligation. This can create financial stress and reduce your flexibility if your income changes, you lose your job, or you face an emergency.

- A Large Down Payment is Still Needed: Even with a loan, you aren’t getting the house for free. You typically need to bring a substantial amount of cash (often 10%–20% of the home’s value) to the closing table, plus closing costs.

The Final Verdict: Which Path is Right for You?

Ultimately, there is no single “right” answer. The best choice depends entirely on your unique financial situation, your personality, and your goals.

Here are a few key questions to ask yourself:

- How’s your financial health? Do you have a large emergency fund in addition to your house fund? If paying cash would leave you with zero savings, it’s too risky.

- What’s your investing savvy? If you are a confident investor who can consistently generate high returns, a mortgage may be the smarter move so you can keep your cash working for you.

- What is your tolerance for risk and debt? If the idea of owing a bank hundreds of thousands of dollars keeps you up at night, the peace of mind from a cash purchase is invaluable, even if it costs you financially in the long run.

A Balanced Strategy: The Best of Both Worlds

You don’t have to choose an extreme. Many savvy buyers opt for a middle ground: They secure a mortgage but make extra principal payments whenever possible. This approach gives them the immediate homeownership of a loan while significantly reducing the total interest paid over time.

To summarize the comparison:

| Factor | Using Savings | Taking a Home Loan |

|---|---|---|

| Initial Cost | Very High | Moderate (Down Payment) |

| Interest Costs | None | Significant |

| Risk | Low | Moderate (You owe a debt) |

| Ownership | Immediate | Builds over time |

| Budget Impact | High at start, then ₹0/mo | Steady, long-term payments |

No matter which path you choose, the most important first step is to get your financial house in order. Consult with a financial advisor and a mortgage lender to see what is realistically affordable for you. Good luck with your home buying journey!

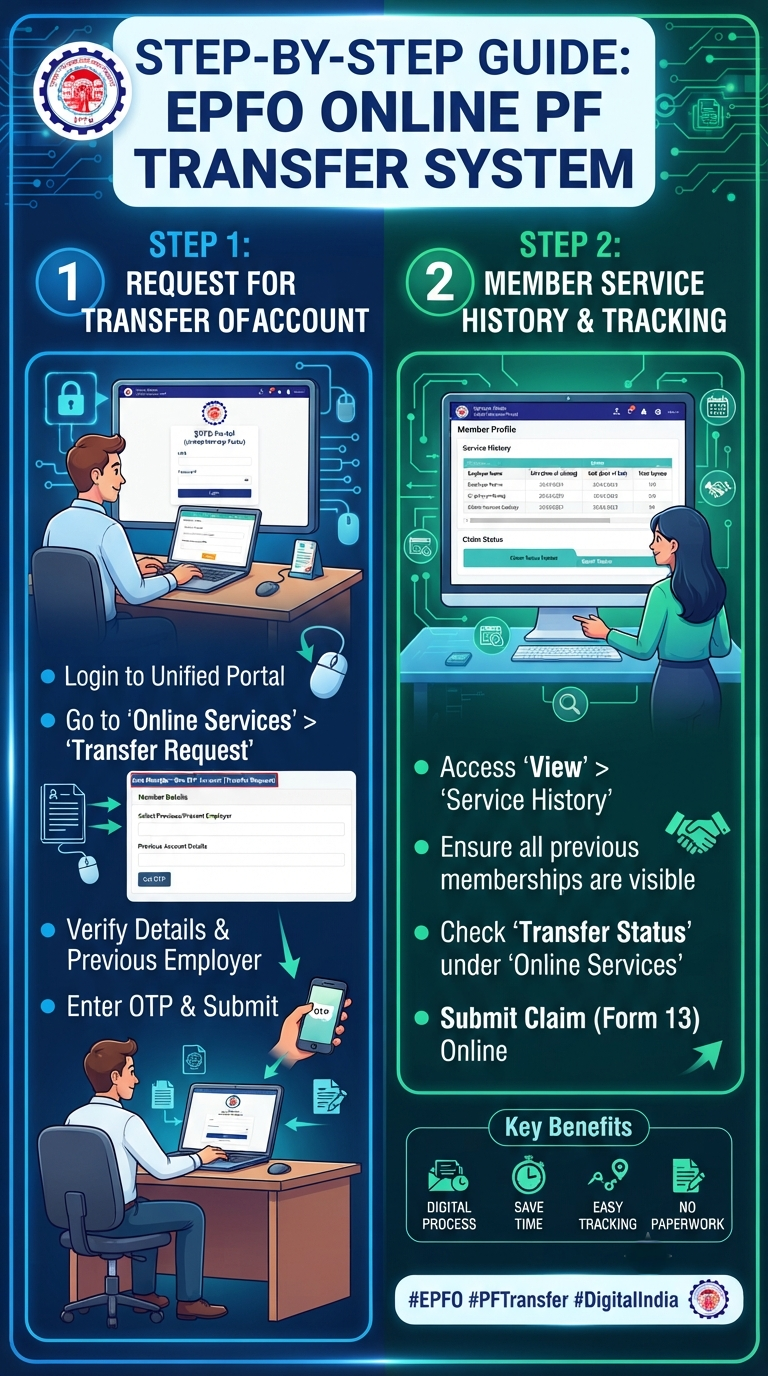

Say Goodbye to Paperwork: How to Consolidate Your EPF Accounts Online

When you’re staring at the fruit bowl wondering which snack will do your heart the most good, it’s easy to feel torn. Do you reach for the convenient banana or the zesty, refreshing orange? Both are nutritional powerhouses, but they bring different strengths to your cardiovascular game. Let’s break down how these two favorites measure…

Continue Reading Heart-Healthy Snacking: The Battle of the Fruits

Let’s be honest: tracking down old Provident Fund (PF) accounts from past jobs feels like a chore no one wants to tackle. Between the mountain of forms, the fear of losing service history, and the sheer time it takes, many of us just leave our old accounts sitting idle. But what if you could clean…

Continue Reading Say Goodbye to Paperwork: How to Consolidate Your EPF Accounts Online

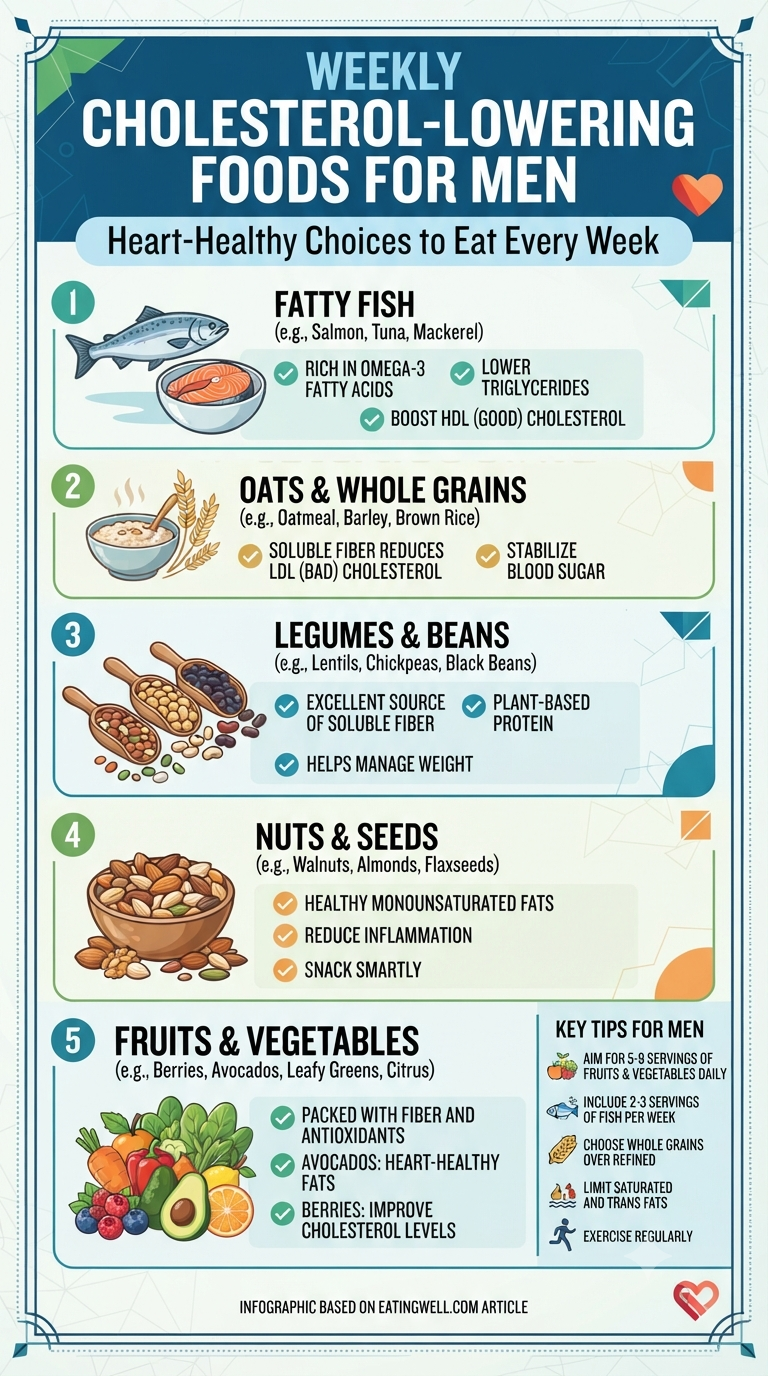

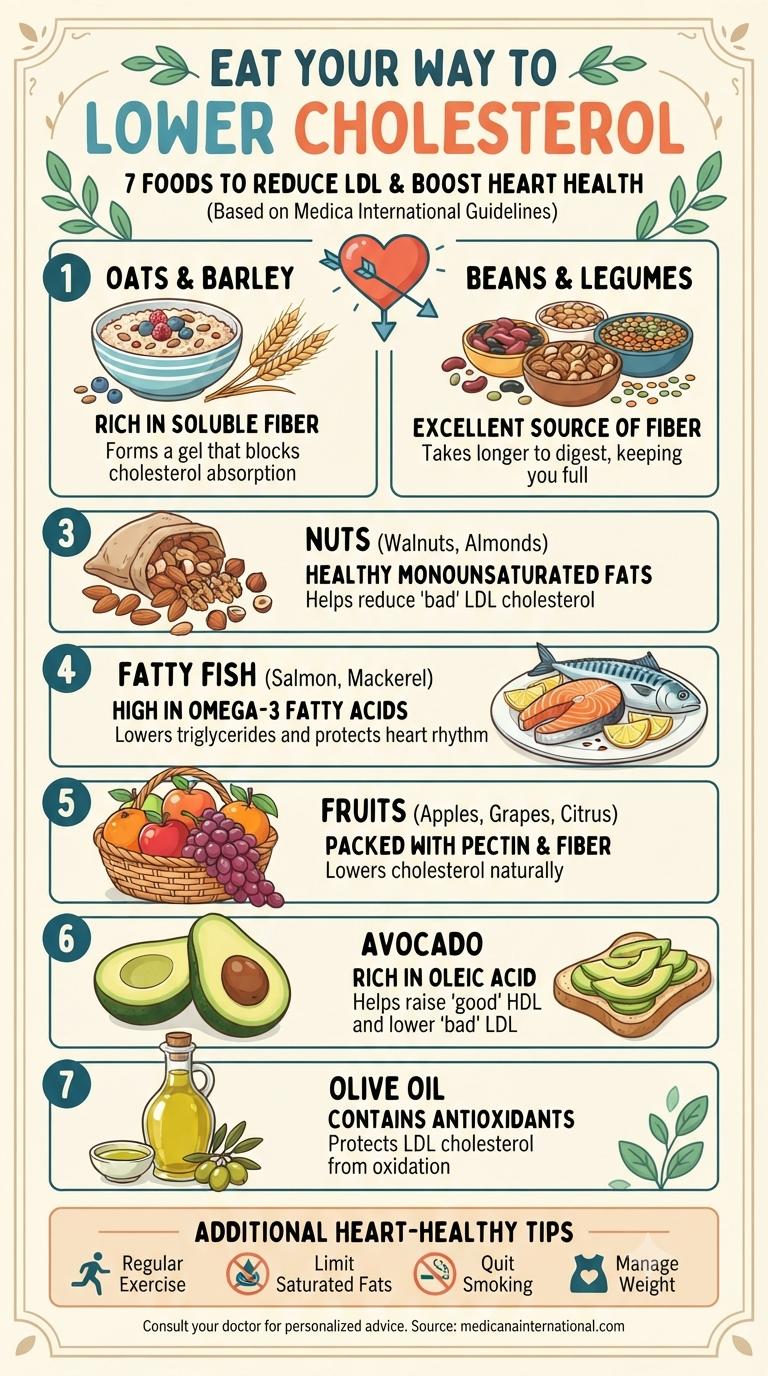

When it comes to longevity, men often focus on building muscle or increasing stamina, but there is a silent powerhouse that deserves just as much attention: your cholesterol levels. Managing cholesterol isn’t just about what you don’t eat—it’s about what you do add to your plate. If you’re looking for a simple, actionable way to…

Continue Reading Take Control of Your Heart Health: 5 Simple Foods to Add to Your Weekly Routine

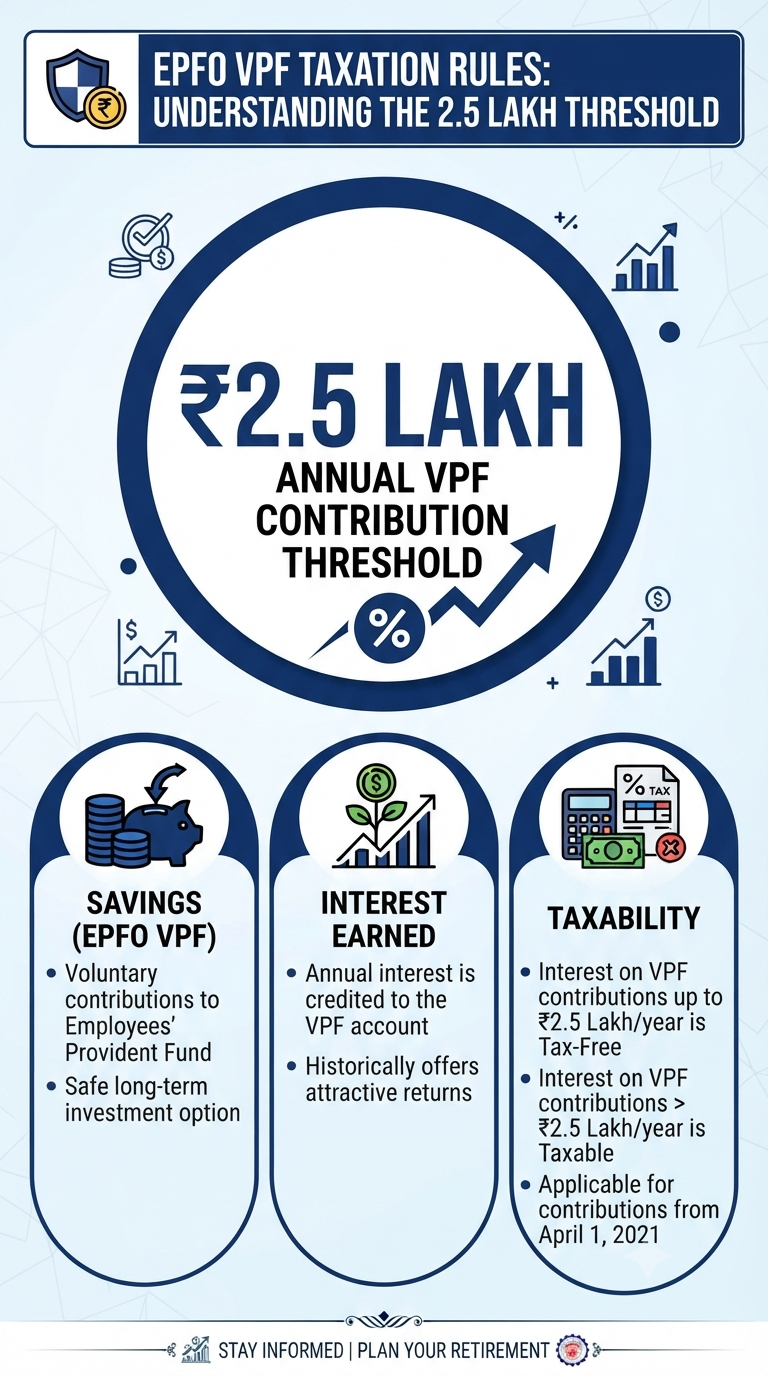

If you’ve been meticulously planning your retirement and using the Voluntary Provident Fund (VPF) as your go-to “set it and forget it” investment vehicle, you’re not alone. It’s a favorite for conservative investors who love the safety, the government backing, and those consistent returns that often outshine standard savings instruments. But, if you’ve been pumping…

Continue Reading Beyond the Threshold: Making Sense of the EPFO VPF Taxation Rule

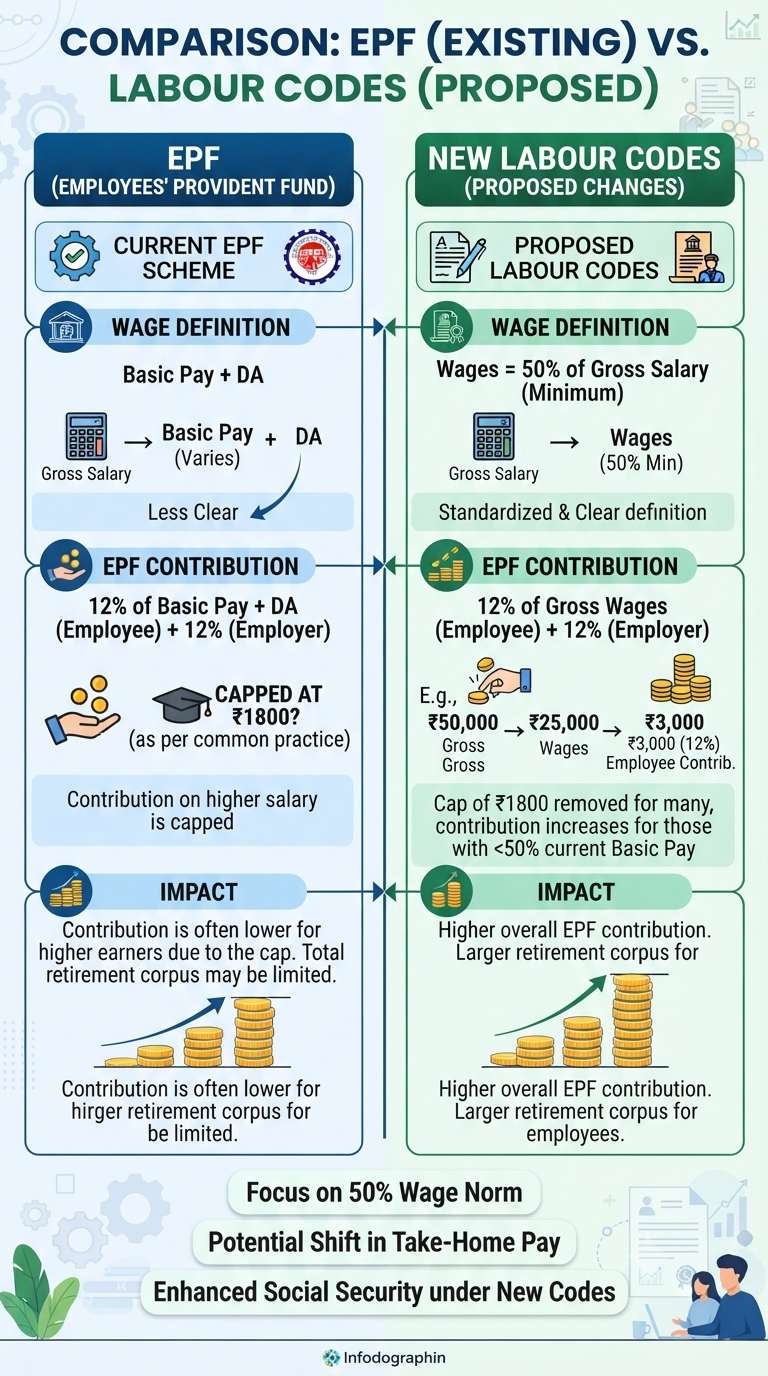

If you’ve recently opened your payslip with a sense of bewilderment, you aren’t alone. Between the buzz surrounding India’s new Labour Codes and the persistent questions about that mysterious ₹1,800 Provident Fund (PF) cap, the world of personal finance can feel like a labyrinth. But what exactly is changing, and more importantly, what does it…

Continue Reading The Great Salary Shift: Decoding the Labour Codes and the EPF Cap Myth

We often hear that “you are what you eat,” and when it comes to heart health, this couldn’t be more true. Cholesterol is a vital substance our bodies use to build cells and produce hormones. However, when levels of low-density lipoprotein (LDL)—often called the “bad” cholesterol—climb too high, it can increase our risk for cardiovascular…

Continue Reading Eat Your Way to a Healthier Heart: A Simple Guide to Lowering Cholesterol

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.