Entering your retirement years should be about peace of mind, not worrying about where to park your hard-earned savings. If you are a senior citizen in India looking to balance safety with decent returns, you’ve likely found yourself choosing between the Senior Citizen Savings Scheme (SCSS) and a Senior Citizen Fixed Deposit (FD) from banks like ICICI Bank.

But which one actually puts more money in your pocket? Let’s break it down.

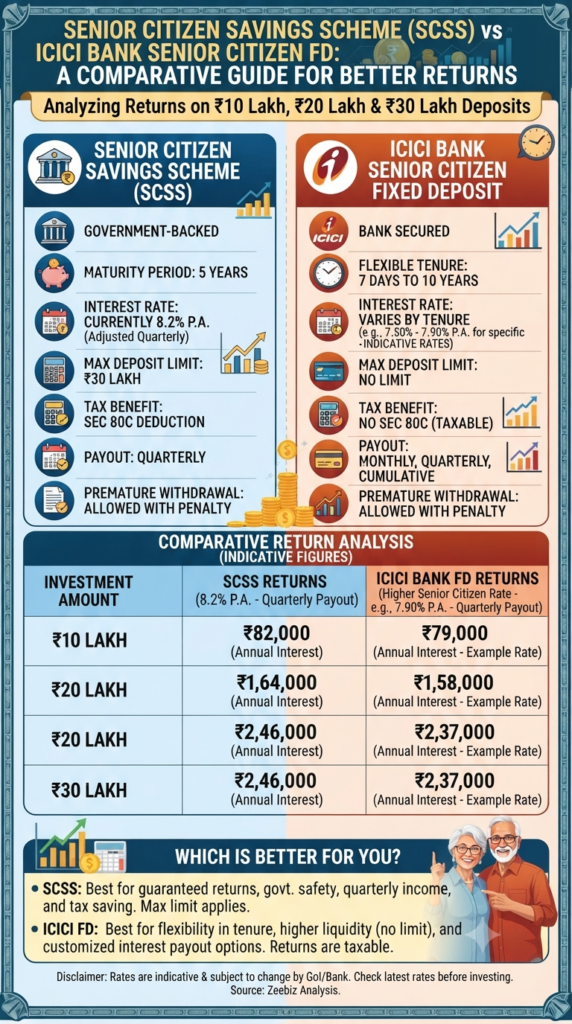

The Contenders: A Quick Overview

1. The Government-Backed Safety Net: SCSS

The Senior Citizen Savings Scheme is a government-backed investment, making it one of the safest options available.

- Tenure: It has a fixed maturity period of 5 years.

- Interest: It currently offers an attractive interest rate of 8.2% per annum, which is adjusted quarterly.

- Limits & Tax: You can invest up to ₹30 lakh, and the icing on the cake is that it qualifies for tax deductions under Section 80C.

- Payout: Interest is paid out on a quarterly basis, providing a steady income stream.

2. The Flexible Alternative: ICICI Bank Senior Citizen FD

If you value flexibility over strict government backing, a bank FD might be your preference.

- Tenure: You get much more freedom here, with tenures ranging from as little as 7 days up to 10 years.

- Interest: Rates vary depending on the tenure you choose (typically ranging between 7.50% and 7.90% for specific tenures).

- Limits & Tax: There is no maximum limit on how much you can deposit, but note that the interest earned is fully taxable (it does not qualify for Section 80C deductions).

- Payout: You can choose between monthly, quarterly, or cumulative payout options, depending on your cash flow needs.

The Numbers Game: How Much Will You Earn?

To see which one performs better, let’s look at how they compare on specific investment amounts, assuming the current illustrative rates (8.2% for SCSS vs. 7.90% for ICICI FD):

| Investment Amount | SCSS Annual Interest (at 8.2%) | ICICI FD Annual Interest (at 7.9%) |

| ₹10 Lakh | ₹82,000 | ₹79,000 |

| ₹20 Lakh | ₹1,64,000 | ₹1,58,000 |

| ₹30 Lakh | ₹2,46,000 | ₹2,37,000 |

Note: Figures are indicative and for comparative purposes based on the provided analysis.

So, Which One Should You Choose?

The “better” option really depends on your personal financial goals:

- Choose SCSS if: You prioritize absolute safety, want to maximize tax benefits under Section 80C, and are looking for a reliable, guaranteed quarterly income.

- Choose ICICI FD if: You need flexibility in how long your money is locked away, want the freedom to deposit large sums without a cap, or prefer payout frequencies like monthly interest.

Regardless of which you choose, both are excellent tools for senior citizens to ensure their money works as hard for them as they did for it.

Disclaimer: Interest rates are indicative and subject to change by the Government of India or the bank. Always check the latest applicable rates with your bank or post office before making an investment decision.

Fixed Deposits in India: Are You Really Getting the Best Returns?

You’ve done your homework. You’ve read the financial news, listened to the podcasts, and decided it’s time to secure your financial future. To build a robust, resilient portfolio, you adopt a “more is merrier” strategy, buying into several different mutual funds to ensure you are diversified. But here is a hard truth that many investors…

Continue Reading The Illusion of Choice: Are You Trapped in the Mutual Fund Overlap Web?

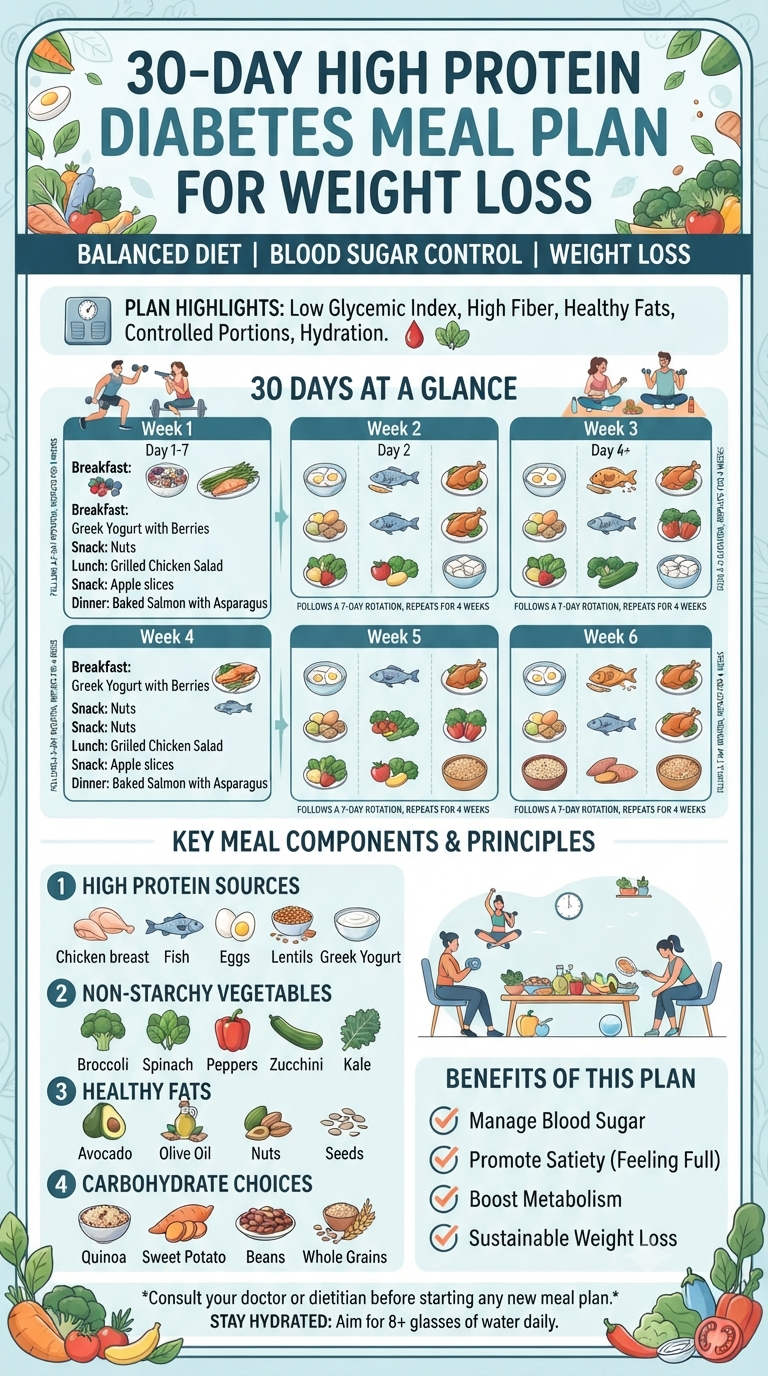

When it comes to health, we’re often bombarded with quick fixes and extreme restrictions. But what if the secret to managing blood sugar and achieving weight loss wasn’t about deprivation, but about intentional, high-protein nourishment? If you’ve been looking for a way to reset your habits without feeling constantly hungry, a high-protein, diabetes-friendly approach might…

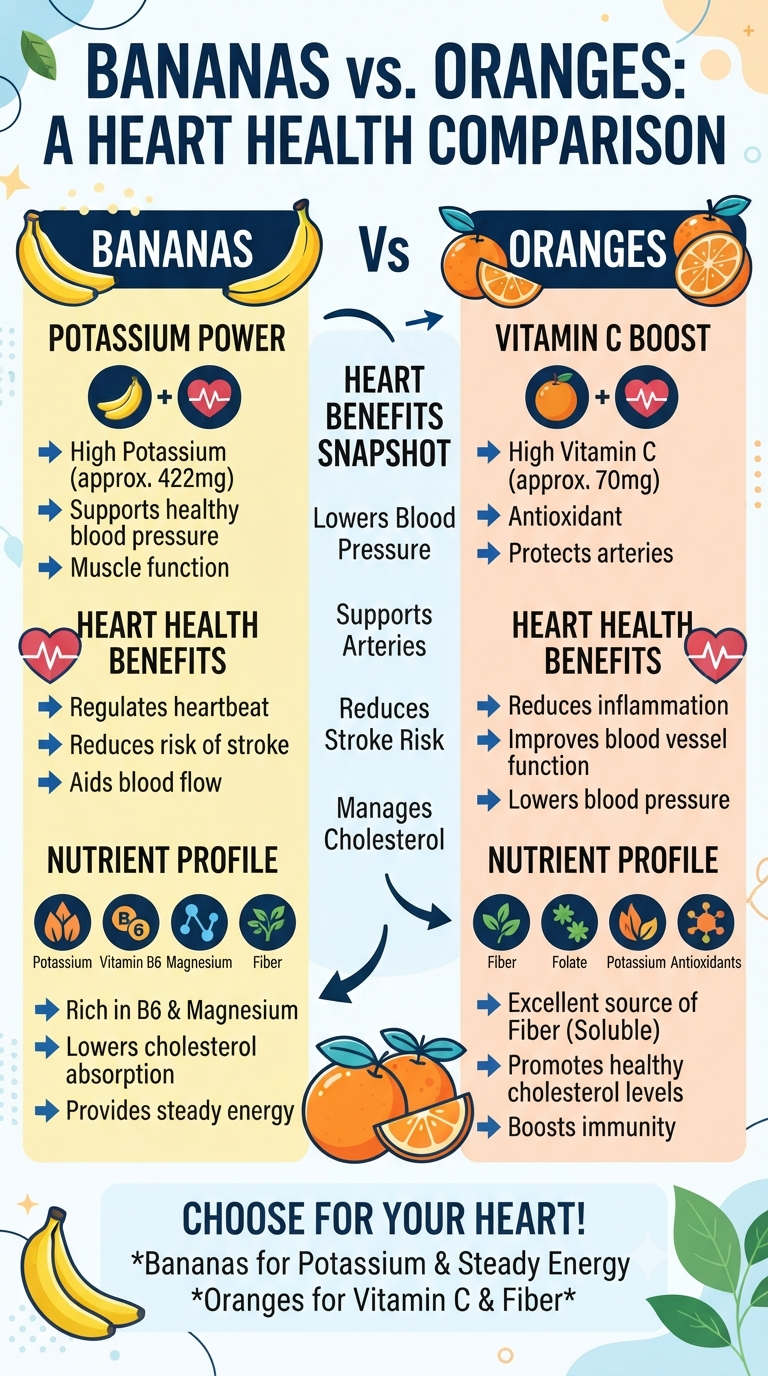

When you’re staring at the fruit bowl wondering which snack will do your heart the most good, it’s easy to feel torn. Do you reach for the convenient banana or the zesty, refreshing orange? Both are nutritional powerhouses, but they bring different strengths to your cardiovascular game. Let’s break down how these two favorites measure…

Continue Reading Heart-Healthy Snacking: The Battle of the Fruits

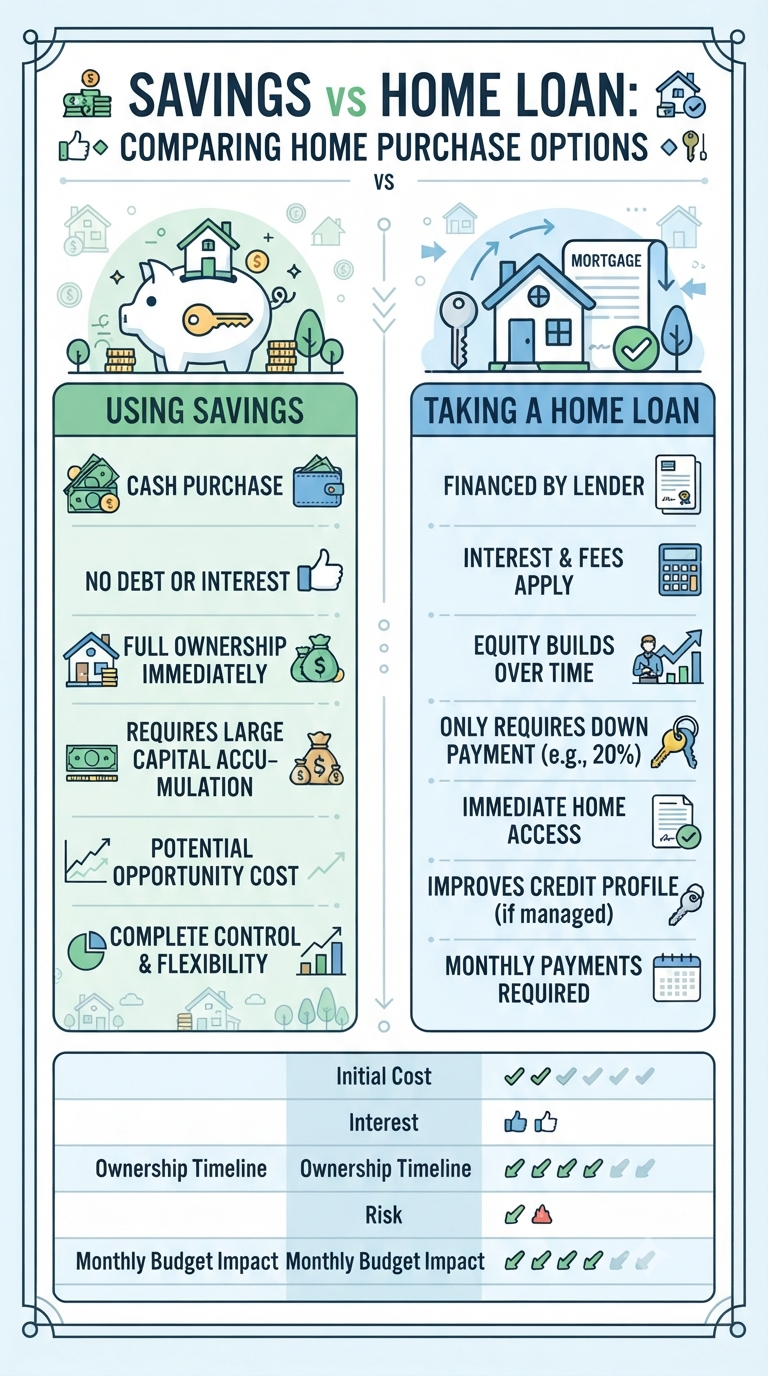

Buying a home is one of life’s biggest milestones. For most people, it’s not just a house—it’s a long-term investment in their future and a place to build a life. But with such a massive price tag, a fundamental question arises: Should I save up and pay cash, or should I take out a home…

Continue Reading The Ultimate Showdown: Is it Better to Buy Your Dream Home with Cash or a Mortgage?

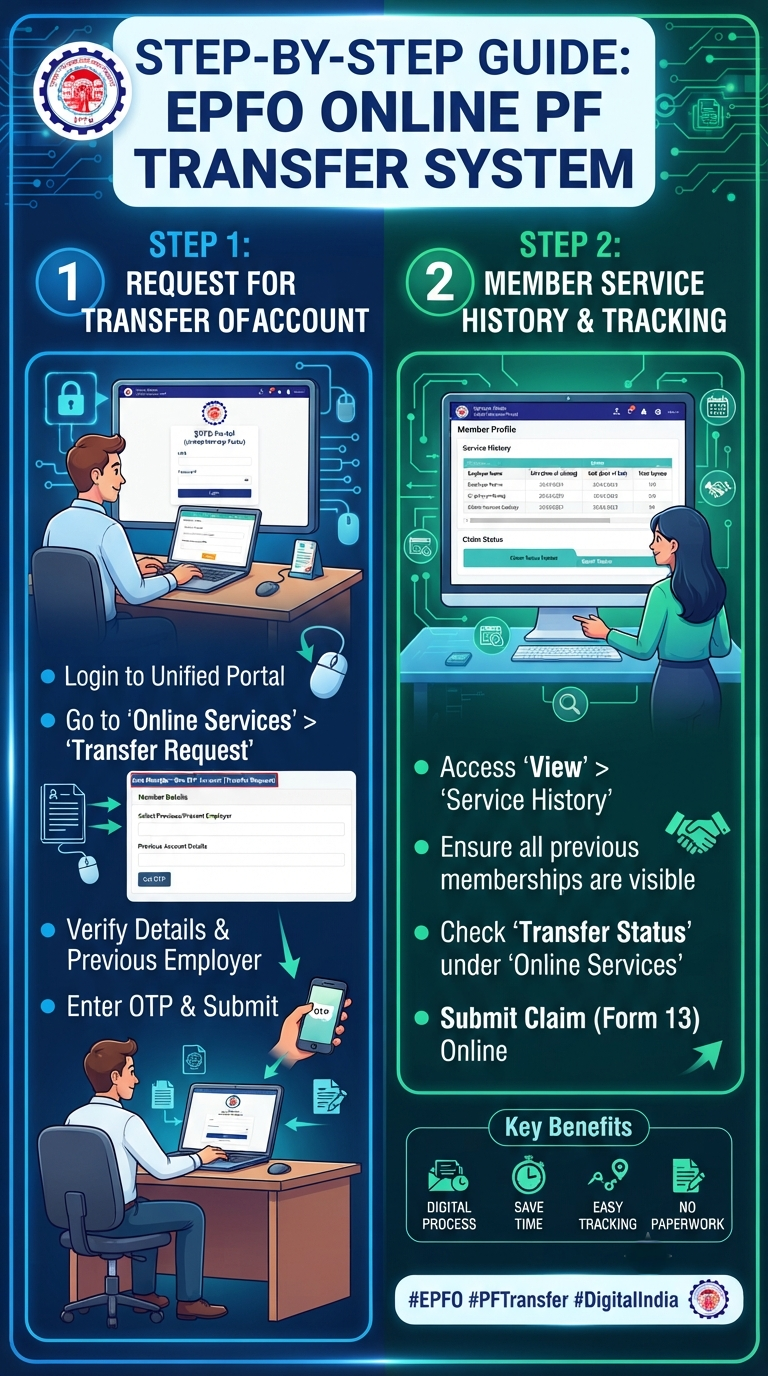

Let’s be honest: tracking down old Provident Fund (PF) accounts from past jobs feels like a chore no one wants to tackle. Between the mountain of forms, the fear of losing service history, and the sheer time it takes, many of us just leave our old accounts sitting idle. But what if you could clean…

Continue Reading Say Goodbye to Paperwork: How to Consolidate Your EPF Accounts Online

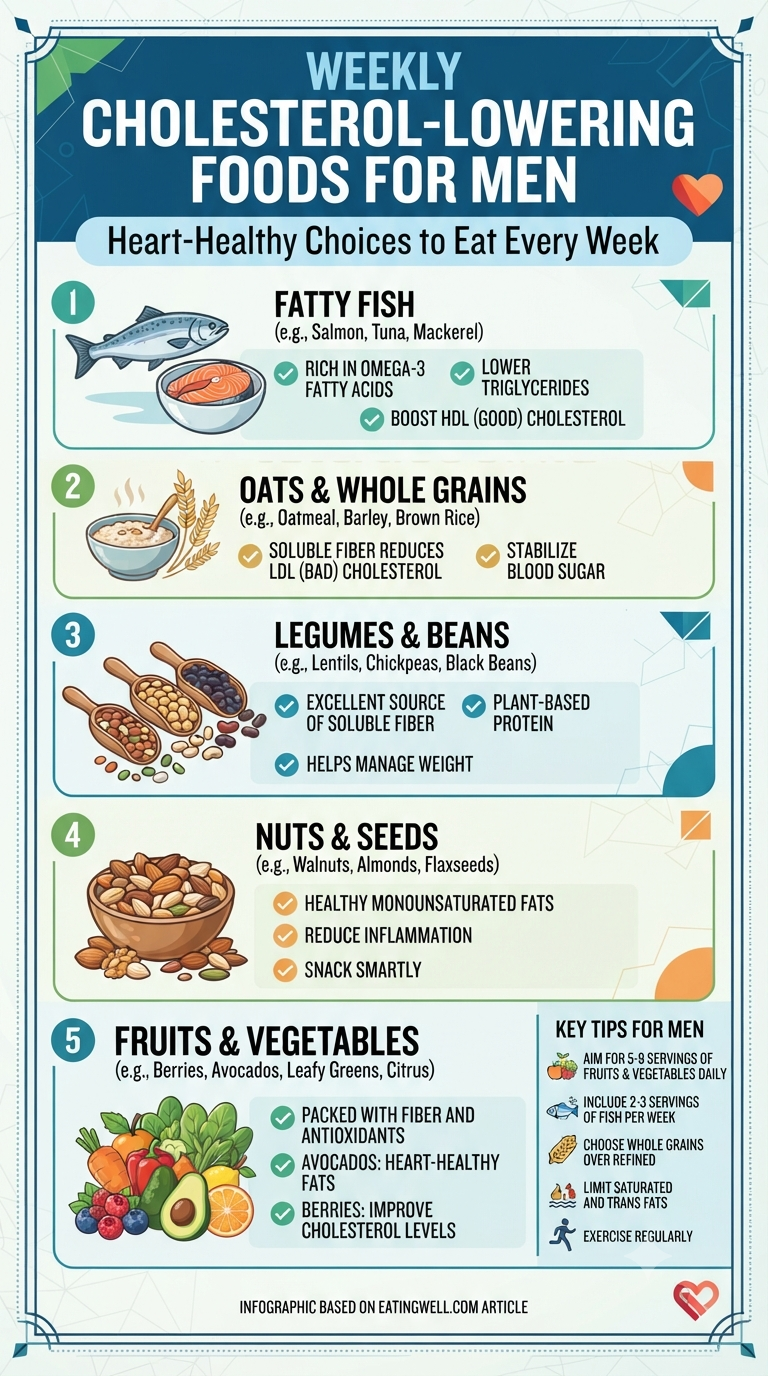

When it comes to longevity, men often focus on building muscle or increasing stamina, but there is a silent powerhouse that deserves just as much attention: your cholesterol levels. Managing cholesterol isn’t just about what you don’t eat—it’s about what you do add to your plate. If you’re looking for a simple, actionable way to…

Continue Reading Take Control of Your Heart Health: 5 Simple Foods to Add to Your Weekly Routine

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.