When it comes to building a secure financial future, the humble Fixed Deposit (FD) remains a cornerstone for millions of Indians. Whether you are a retiree looking for a predictable monthly income or a conservative investor who believes in “slow and steady” growth, FDs have long been the go-to safety net.

But here is the million-dollar question: Are you settling for average returns, or are you truly maximizing your hard-earned money?

The banking landscape in India has changed, and interest rates are no longer one-size-fits-all.

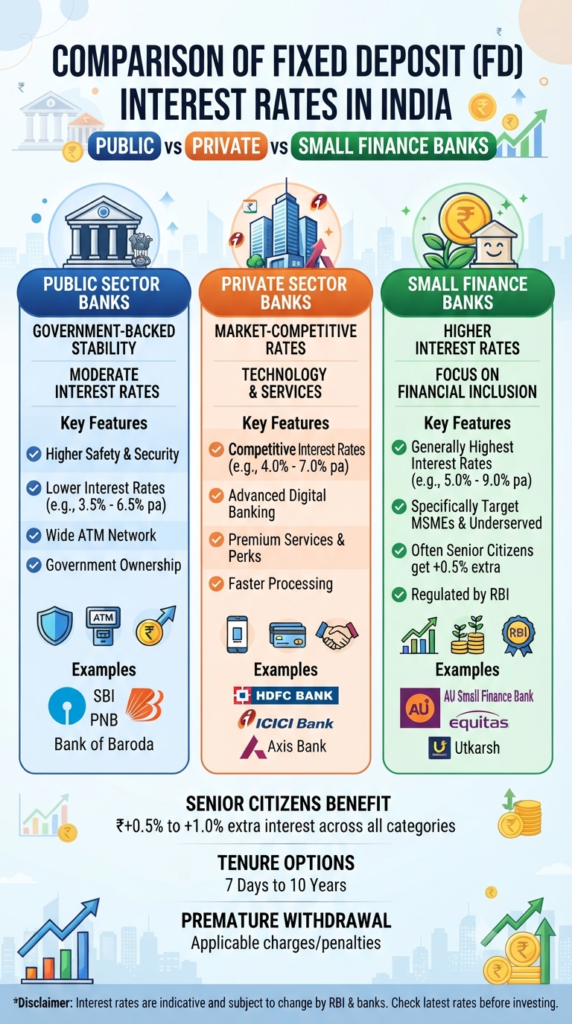

The FD Landscape: A Quick Breakdown

As of July 2026, the spectrum of FD interest rates is wider than many realize. Depending on where you park your funds, you could be looking at a difference of nearly 1.5% to 2% in returns. While that might sound small, over a five or ten-year period, it creates a massive gap in your total maturity amount.

Where Do You Stand?

- Public Sector Banks (PSBs): The classic choice for safety. While you get government backing and unmatched trust, they generally offer lower interest rates (typically ranging between 6.25% and 7.10%).

- Private Sector Banks: These are the “middle ground.” They combine competitive interest rates (6.50% – 7.50%) with modern, user-friendly digital banking.

- Small Finance Banks (SFBs): The “new kids on the block” offering the most aggressive rates. With returns often hitting the 7.00% – 8.50% mark, they are tempting, but they require a bit more homework regarding their financial health and credit ratings.

Why “Highest Rate” Isn’t Always the “Best Choice”

We’ve all seen the flashy advertisements promising the highest interest rates. But before you rush to open an account, take a breath. As investors, we must balance three vital pillars:

- Safety First: Does the bank have a strong history? Check their public disclosures and credit ratings.

- Liquidity: Life is unpredictable. If you need that money tomorrow, what are the penalty charges for premature withdrawal?

- Taxation: Remember, FD interest is fully taxable according to your income tax slab. Are you utilizing Form 15G or 15H if you are eligible?

Pro Tips for Maximizing Your FD Strategy

If you want to move from being an “average” investor to a “smart” one, follow these three rules:

- Look for Special Tenure Schemes: Many banks offer “sweet spot” tenures (like 399, 444, or 888 days) that provide higher interest rates than the standard 1-year or 2-year periods.

- Don’t Ignore Senior Citizen Benefits: If you or a family member are eligible, the extra 0.25% to 0.75% offered by most banks acts as a significant bonus over time.

- Diversify: Don’t put all your eggs in one basket. Split your investment across a couple of stable institutions to balance safety with returns.

The Bottom Line

Fixed Deposits aren’t just a place to keep your money; they are a tool to protect your capital and ensure your peace of mind. By taking a few extra minutes to compare rates and understand the fine print—rather than just picking the bank closest to your house—you can make your money work significantly harder for you.

Final Thought: The best investment is an informed one. Happy investing!

Disclaimer: This article is for educational purposes only. Always evaluate the financial health of an institution before investing. Interest rates are subject to change, so check with your specific bank before making any final decisions.

Secure Your Future: A Simple Guide to Post Office Savings Schemes (July – September 2026)

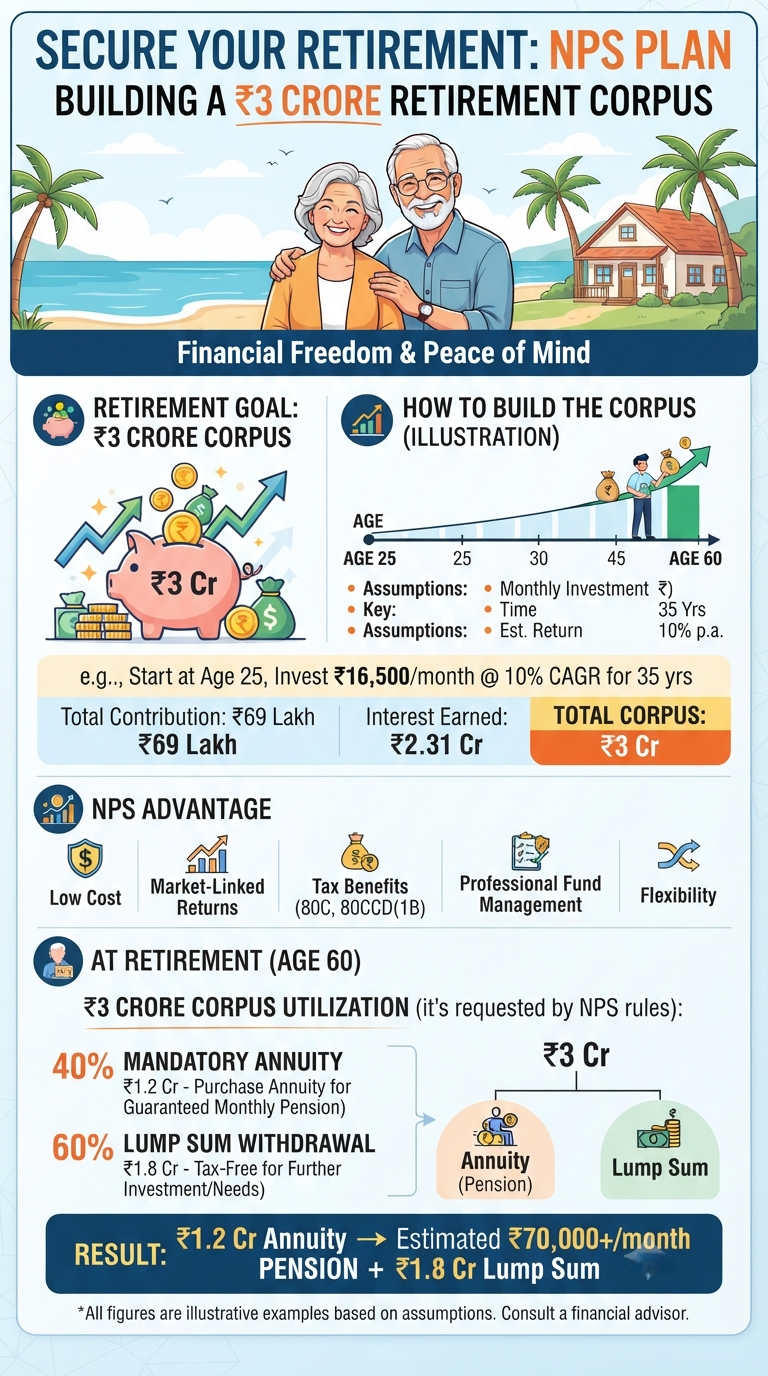

Retirement often feels like a distant milestone—something to worry about “later.” But what if you could visualize that “later” right now? Imagine hitting age 60 with a solid ₹3 crore corpus. It’s not just a number on a screen; it’s the key to your financial independence, the bridge to your passions, and the ultimate safety…

Continue Reading Retire Rich: How a ₹3 Crore Corpus Can Power Your Dream Life

You’ve done your homework. You’ve read the financial news, listened to the podcasts, and decided it’s time to secure your financial future. To build a robust, resilient portfolio, you adopt a “more is merrier” strategy, buying into several different mutual funds to ensure you are diversified. But here is a hard truth that many investors…

Continue Reading The Illusion of Choice: Are You Trapped in the Mutual Fund Overlap Web?

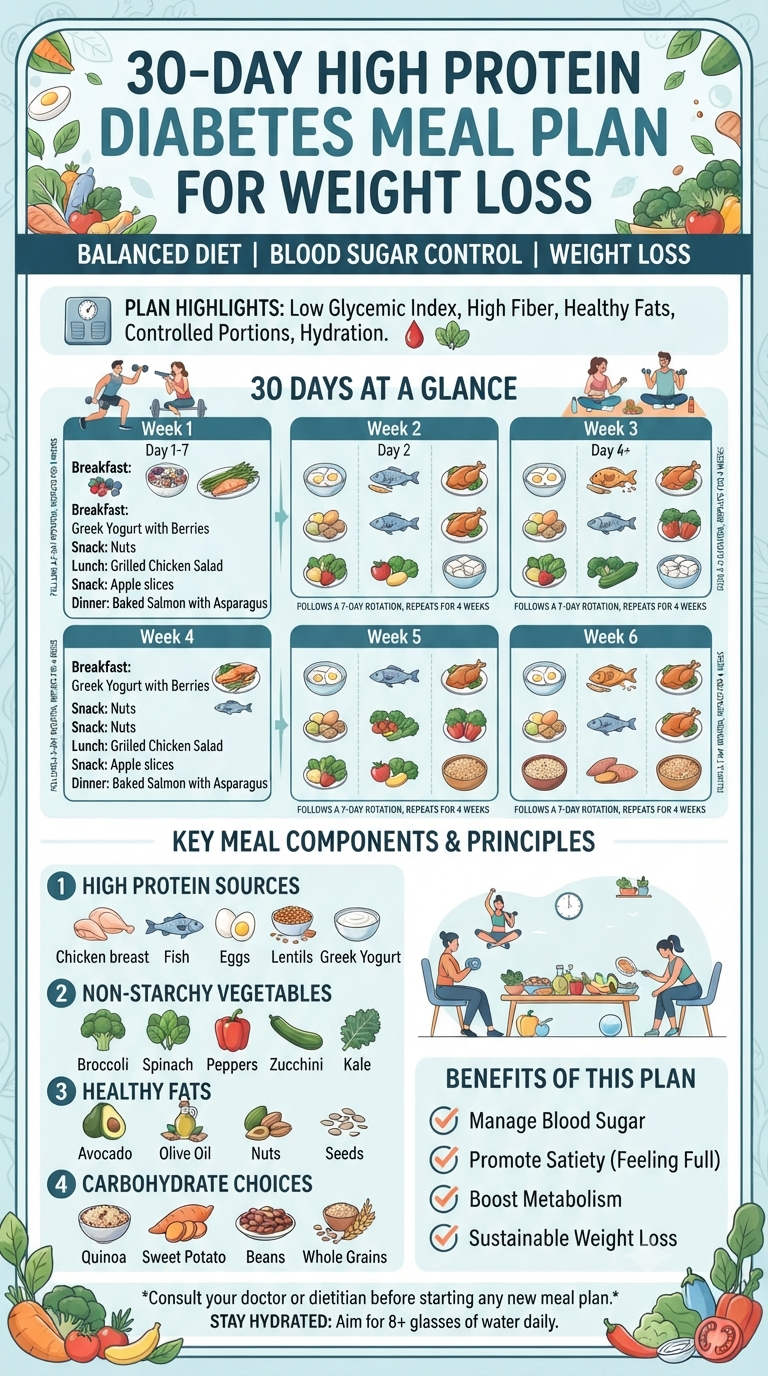

When it comes to health, we’re often bombarded with quick fixes and extreme restrictions. But what if the secret to managing blood sugar and achieving weight loss wasn’t about deprivation, but about intentional, high-protein nourishment? If you’ve been looking for a way to reset your habits without feeling constantly hungry, a high-protein, diabetes-friendly approach might…

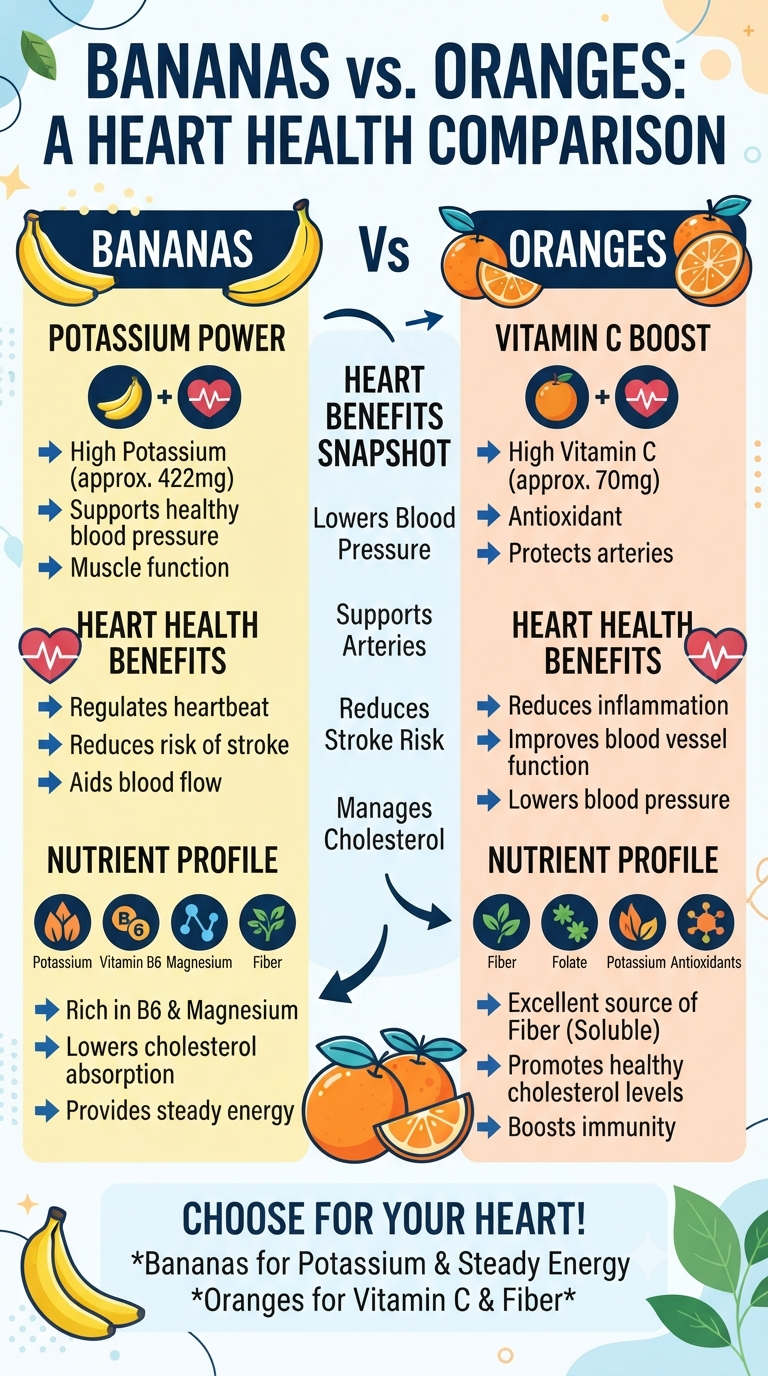

When you’re staring at the fruit bowl wondering which snack will do your heart the most good, it’s easy to feel torn. Do you reach for the convenient banana or the zesty, refreshing orange? Both are nutritional powerhouses, but they bring different strengths to your cardiovascular game. Let’s break down how these two favorites measure…

Continue Reading Heart-Healthy Snacking: The Battle of the Fruits

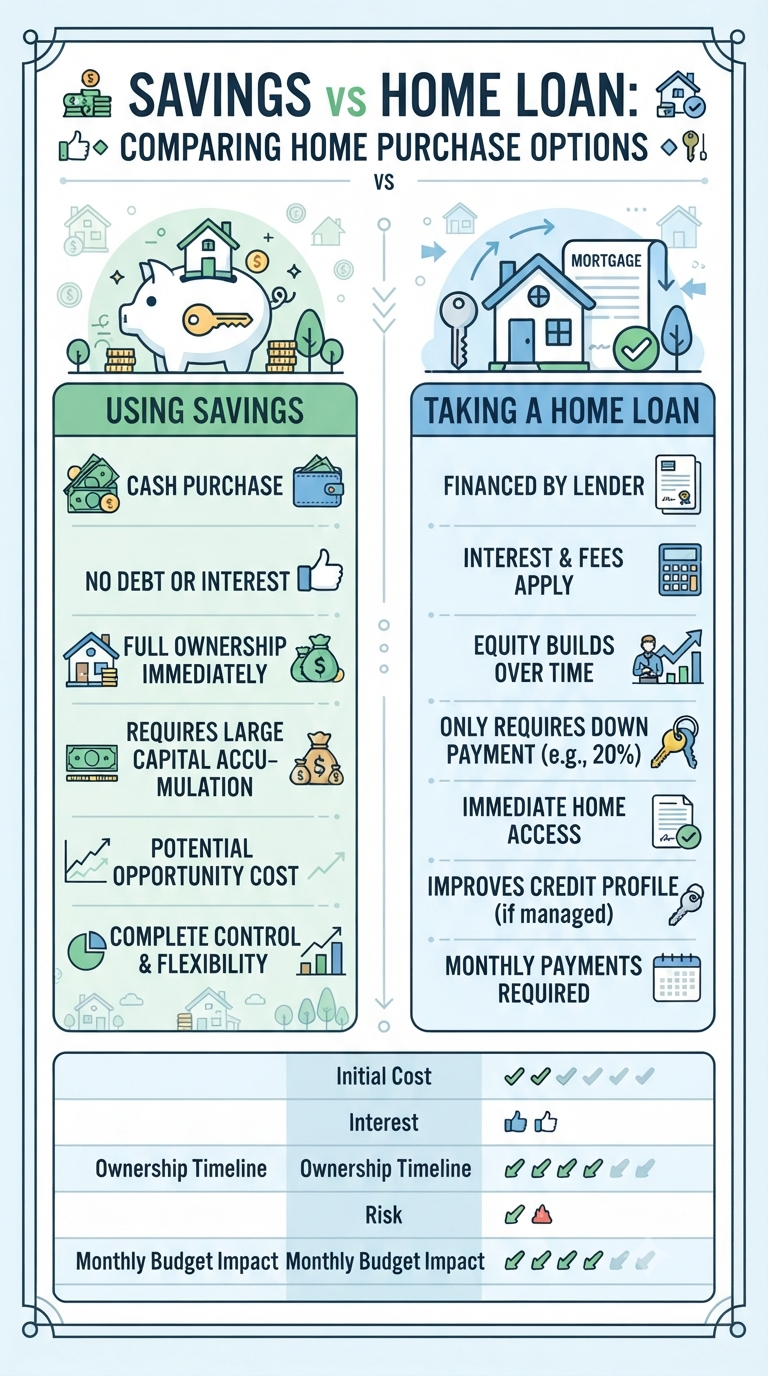

Buying a home is one of life’s biggest milestones. For most people, it’s not just a house—it’s a long-term investment in their future and a place to build a life. But with such a massive price tag, a fundamental question arises: Should I save up and pay cash, or should I take out a home…

Continue Reading The Ultimate Showdown: Is it Better to Buy Your Dream Home with Cash or a Mortgage?

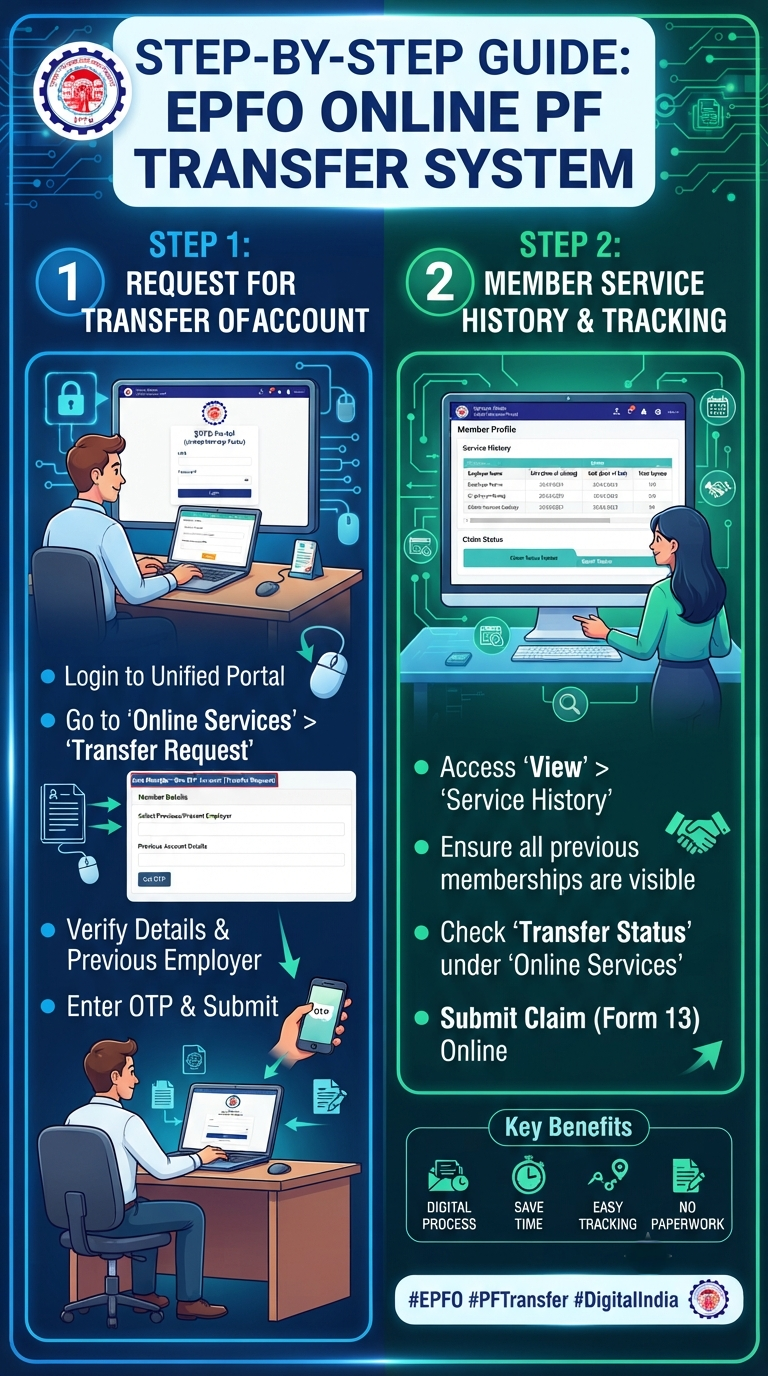

Let’s be honest: tracking down old Provident Fund (PF) accounts from past jobs feels like a chore no one wants to tackle. Between the mountain of forms, the fear of losing service history, and the sheer time it takes, many of us just leave our old accounts sitting idle. But what if you could clean…

Continue Reading Say Goodbye to Paperwork: How to Consolidate Your EPF Accounts Online

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.