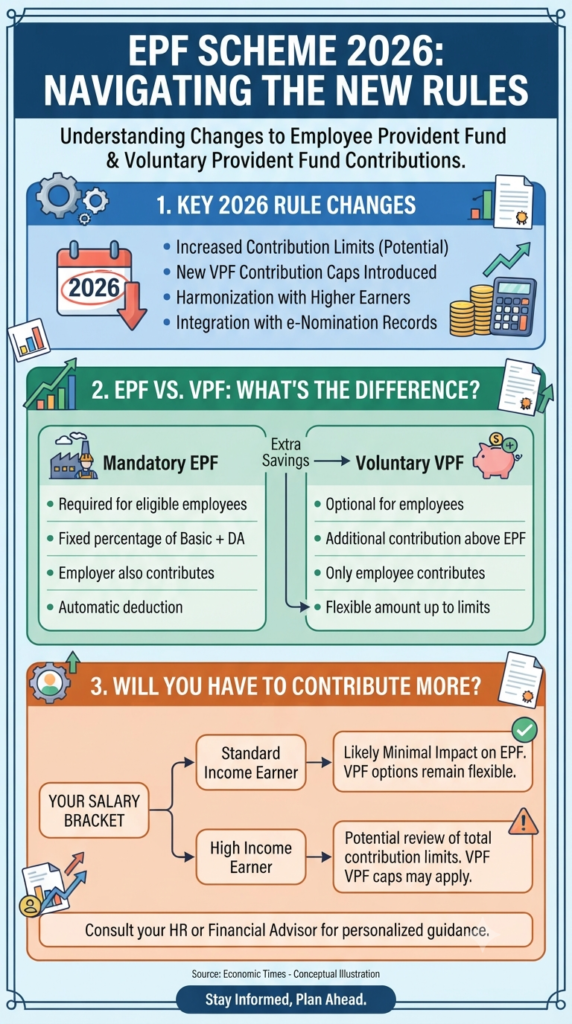

If you’ve been scrolling through financial news lately, you’ve probably noticed the buzz around the “EPF Scheme 2026” updates. It’s the kind of topic that sounds dry until you realize it directly affects how much of your hard-earned money stays in your pocket today versus how much gets tucked away for your future.

With the new rules coming into play, the chatter about potential contribution limits and VPF (Voluntary Provident Fund) caps has left many employees wondering: Am I going to have to contribute more? Is my retirement planning about to change overnight?

Let’s break it down without the financial jargon.

The Big Picture: What’s Actually Changing?

The core idea behind the 2026 updates isn’t to make your life difficult; it’s about harmonization. The authorities are essentially looking to streamline the contribution framework to ensure there’s a clearer structure for both standard and high-income earners.

Key themes you should be aware of include:

- Potential Contribution Adjustments: While the basics of EPF remain familiar, there are shifts in how caps are being viewed, particularly for those who aggressively use VPF.

- A Focus on Higher Earners: If you are in a higher salary bracket, the new rules are more likely to impact you, specifically regarding how total contributions—EPF plus VPF—are treated.

- Seamless Integration: The system is leaning heavily into digital efficiency, meaning your e-nomination records and contribution tracking are becoming more tightly linked.

EPF vs. VPF: A Quick Refresher

It’s easy to confuse the two, but think of it this way: EPF is your mandatory foundation, and VPF is your optional “booster” pack.

- Mandatory EPF: This is the non-negotiable slice of your basic salary plus Dearness Allowance that goes into your retirement fund. Your employer matches this, and it happens automatically.

- Voluntary VPF: This is where you take the driver’s seat. You choose to contribute above and beyond your mandatory EPF to build a larger corpus. It’s flexible, it’s voluntary, and until now, it’s been a favorite tool for tax-efficient savings.

So, Will You Have to Contribute More?

This is the million-dollar question. The short answer? It depends on who you are.

- For the Standard Income Earner: You likely won’t see a massive disruption. The mandatory EPF structure is staying the course, and your ability to save remains largely intact.

- For the High Income Earner: This is where you need to pay attention. If you’ve been maxing out your VPF contributions to take advantage of tax benefits, the new rules might introduce caps on how much you can contribute across your total EPF and VPF portfolio.

What Should You Do Now?

Don’t panic and don’t make rash decisions. Instead:

- Check Your Current Contributions: Log into your EPF portal and see what percentage you are currently contributing to VPF.

- Speak to Your HR: They are the ones who will be implementing these technical changes on the payroll side. They can tell you exactly how the new rules will reflect on your monthly payslip.

- Consult a Financial Advisor: If you were relying on VPF as a core pillar of your retirement strategy, it’s time to see if you need to pivot your extra savings into other instruments like PPF, NPS, or mutual funds to maintain your wealth-building momentum.

The Bottom Line: Change can feel overwhelming, but staying informed is the best defense against confusion. The goal of these 2026 rules is long-term stability—make sure your personal financial plan is built to handle the shifts.

Stay informed, and keep planning ahead.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Tax laws and EPF regulations are subject to change. Always consult with a qualified financial advisor regarding your personal financial situation.

The 8th Pay Commission Buzz: What Could It Mean for Your Paycheck?

Planning for your child’s future is perhaps the most important financial responsibility a parent carries. Whether it is dreaming about her higher education in a top-tier university or ensuring her wedding is everything she wished for, the math can sometimes feel overwhelming. But what if there was a government-backed “secret weapon” designed specifically to help…

Continue Reading The Secret to Building a Rs 50 Lakh Corpus for Your Daughter’s Future

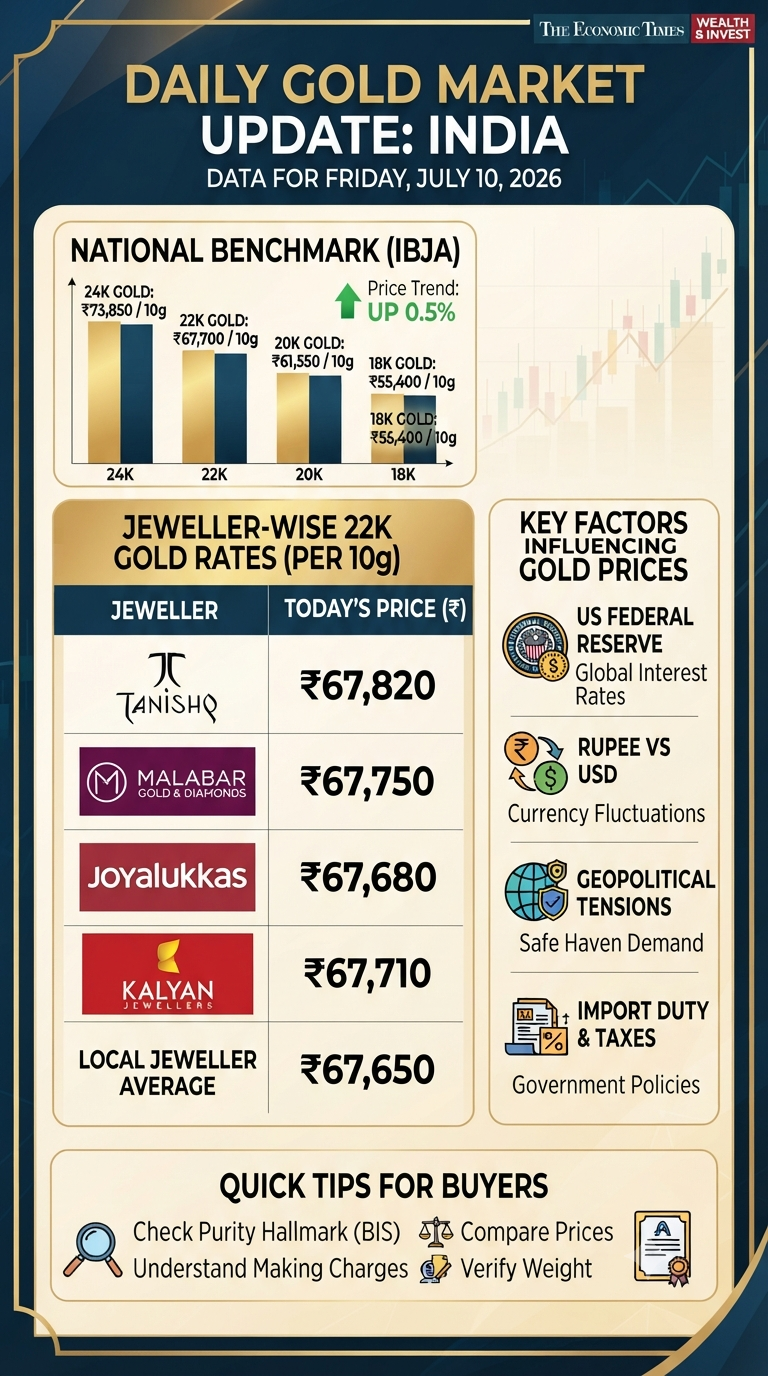

If you’ve been keeping an eye on the markets lately, you know that gold isn’t just a shiny accessory—it’s the heartbeat of Indian investment. Whether you are planning for a wedding, looking for a festive gift, or simply bolstering your portfolio, staying updated on daily price shifts is essential. As of today, Friday, July 10,…

Continue Reading Decoding Today’s Gold Rush: A Buyer’s Guide to Navigating the Market

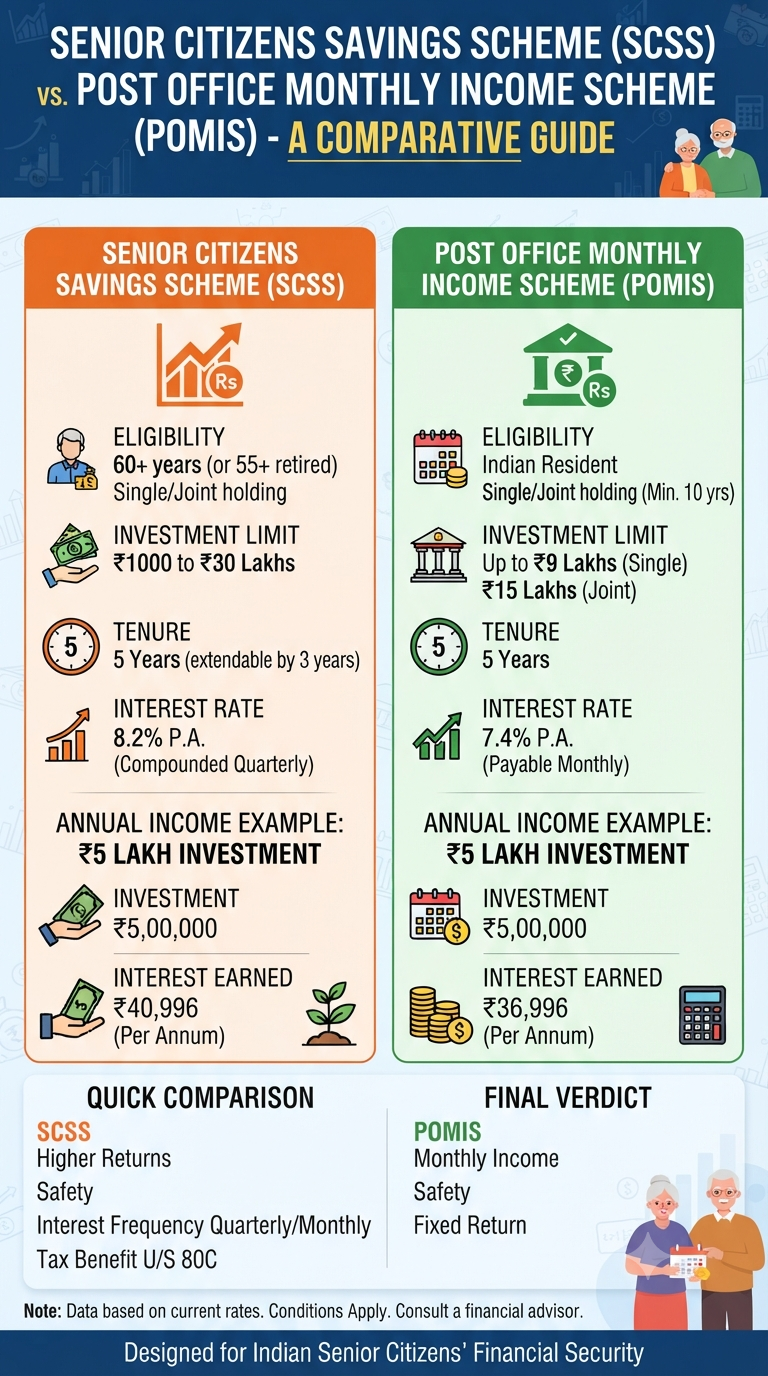

If you are looking for a safe, government-backed harbor for your hard-earned money, the Senior Citizens Savings Scheme (SCSS) and the Post Office Monthly Income Scheme (MIS) are likely at the top of your list. They offer peace of mind, stability, and the reliability of a sovereign guarantee. But when it comes to maximizing your…

Let’s be honest. Most of us know EPF stands for Employees’ Provident Fund, and we know a chunk of our salary goes into it every month. But how many of us actually know exactly how much is in that corpus, or—more importantly—if that promised 8.25% interest has hit our account yet? If you’ve been meaning…

Continue Reading Checkmate Your PF Status: 4 Simple Ways to View Your EPF Balance Right Now

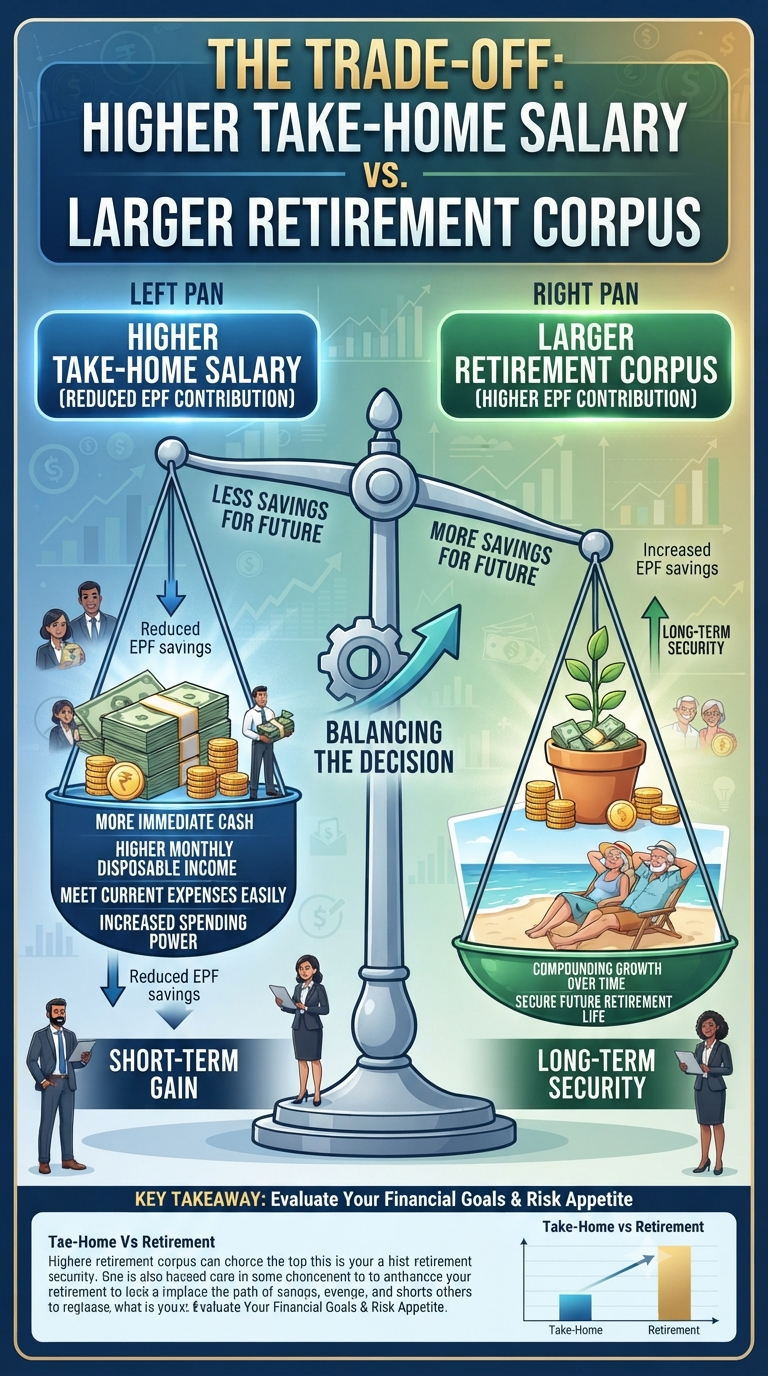

For any salaried professional, that email from HR announcing a salary hike—or better yet, a change that boosts your monthly take-home pay—is usually a cause for celebration. We all love a little extra breathing room in our monthly budget to cover rising costs, splurge on a vacation, or simply enjoy a higher standard of living…

Continue Reading More Cash Today or Millions Tomorrow? Decoding the Proposed EPF Change

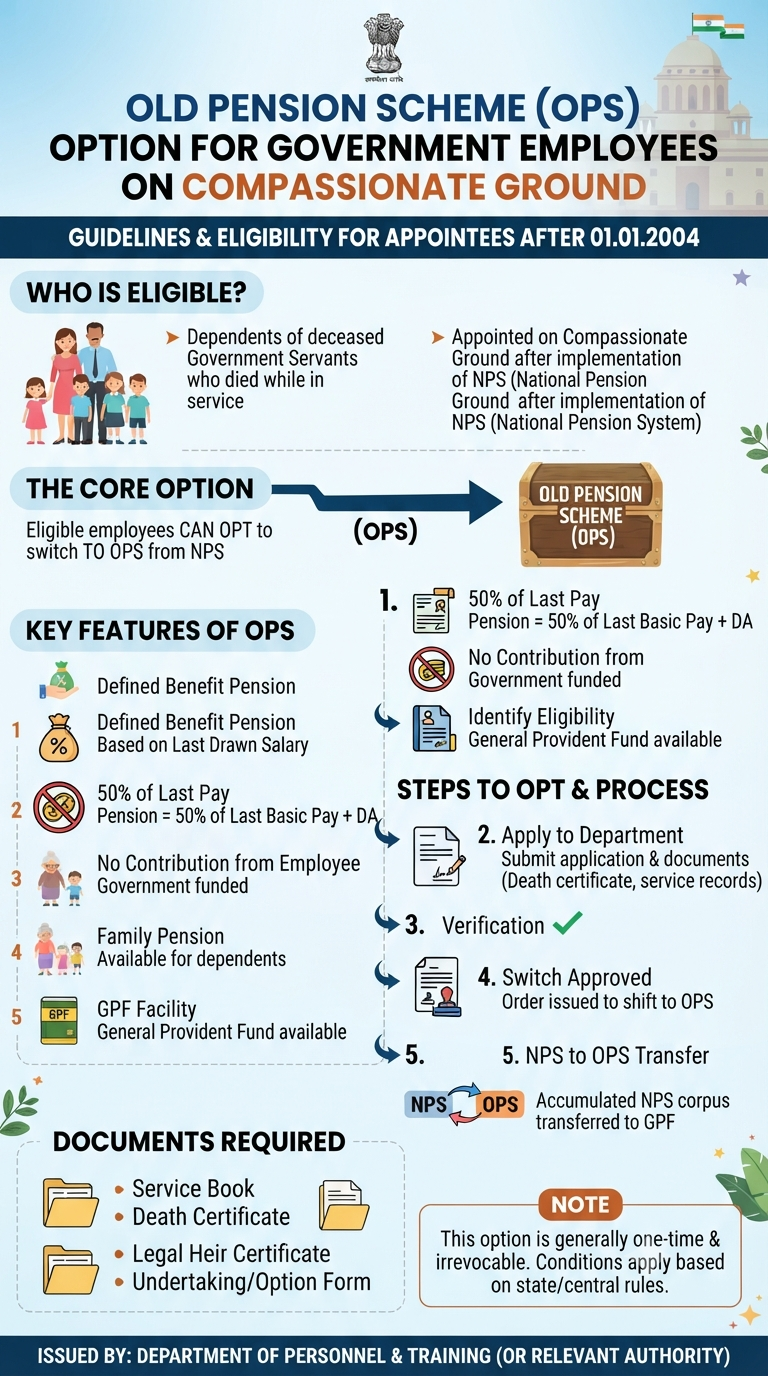

For thousands of government employees who entered service through the compassion of a family-related appointment, the transition into their careers was often marked by a bureaucratic “what-if.” Many had applied for their positions before the cutoff of December 2003, only to join service after the National Pension System (NPS) had already taken hold in January…

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.