Planning for your child’s future is perhaps the most important financial responsibility a parent carries. Whether it is dreaming about her higher education in a top-tier university or ensuring her wedding is everything she wished for, the math can sometimes feel overwhelming.

But what if there was a government-backed “secret weapon” designed specifically to help you turn modest annual savings into a substantial, life-changing corpus?

Enter the Sukanya Samriddhi Account (SSA)—a cornerstone of the ‘Beti Bachao Beti Padhao’ campaign that has become the gold standard for parents looking for security, high returns, and absolute peace of mind.

The Power of 15 Years of Discipline

Many parents mistakenly believe that building a 50-lakh rupee fund requires a massive lump sum upfront. The beauty of the SSA lies in its simplicity and consistency rather than huge, sporadic investments.

According to recent analysis, if you commit to an annual investment of Rs 1,05,000 for a period of 15 years, the power of compounding takes over for the remaining 6 years of the account’s tenure.

- Total Investment: Rs 15.75 lakh over 15 years.

- The Wait: You stop depositing after year 15, but your money continues to grow untouched.

- The Reward: With a steady interest rate of 8.2% per annum (compounded annually), your initial investment balloons into an estimated Rs 50.27 lakh by the time the account matures at the 21-year mark.

Why SSA Stands Out

In a world of volatile market investments, the SSA offers the “triple-threat” of financial safety:

- The “EEE” Tax Advantage: The SSA is one of the few investment vehicles that enjoys an EEE (Exempt-Exempt-Exempt) status. This means your deposits are tax-deductible under Section 80C, the interest earned is tax-free, and the final maturity amount is also free from income tax.

- Unbeatable Stability: As a government-backed small savings scheme, it offers one of the highest interest rates in its category, reviewed quarterly to stay competitive.

- The Compound Effect: By investing consistently for the first 15 years, you allow the account to generate significant interest—roughly Rs 34.52 lakh in the example above—without you having to add another rupee for the final 6 years.

Getting Started

The entry barrier is incredibly low. You can open an account with a minimum deposit of just Rs 250, and you can contribute up to a maximum of Rs 1.5 lakh per financial year.

The interest is calculated based on the lowest balance in your account between the close of the fifth day and the end of the month, and it is credited annually. This makes it an ideal “set-it-and-forget-it” strategy for long-term planning.

Final Thoughts

A 50-lakh corpus isn’t just a number; it’s the freedom to choose the best for your daughter without the stress of financial strain. By leveraging the Sukanya Samriddhi Account early, you aren’t just saving money—you are securing her dreams and providing her with the financial foundation to soar.

Disclaimer: Interest rates for the Sukanya Samriddhi Account are reviewed quarterly by the government. The projections mentioned above are based on the assumption that the interest rate remains constant at 8.2% throughout the tenure.

Decoding Today’s Gold Rush: A Buyer’s Guide to Navigating the Market

If you’ve been keeping an eye on the markets lately, you know that gold isn’t just a shiny accessory—it’s the heartbeat of Indian investment. Whether you are planning for a wedding, looking for a festive gift, or simply bolstering your portfolio, staying updated on daily price shifts is essential. As of today, Friday, July 10,…

Continue Reading Decoding Today’s Gold Rush: A Buyer’s Guide to Navigating the Market

If you are looking for a safe, government-backed harbor for your hard-earned money, the Senior Citizens Savings Scheme (SCSS) and the Post Office Monthly Income Scheme (MIS) are likely at the top of your list. They offer peace of mind, stability, and the reliability of a sovereign guarantee. But when it comes to maximizing your…

Let’s be honest. Most of us know EPF stands for Employees’ Provident Fund, and we know a chunk of our salary goes into it every month. But how many of us actually know exactly how much is in that corpus, or—more importantly—if that promised 8.25% interest has hit our account yet? If you’ve been meaning…

Continue Reading Checkmate Your PF Status: 4 Simple Ways to View Your EPF Balance Right Now

For any salaried professional, that email from HR announcing a salary hike—or better yet, a change that boosts your monthly take-home pay—is usually a cause for celebration. We all love a little extra breathing room in our monthly budget to cover rising costs, splurge on a vacation, or simply enjoy a higher standard of living…

Continue Reading More Cash Today or Millions Tomorrow? Decoding the Proposed EPF Change

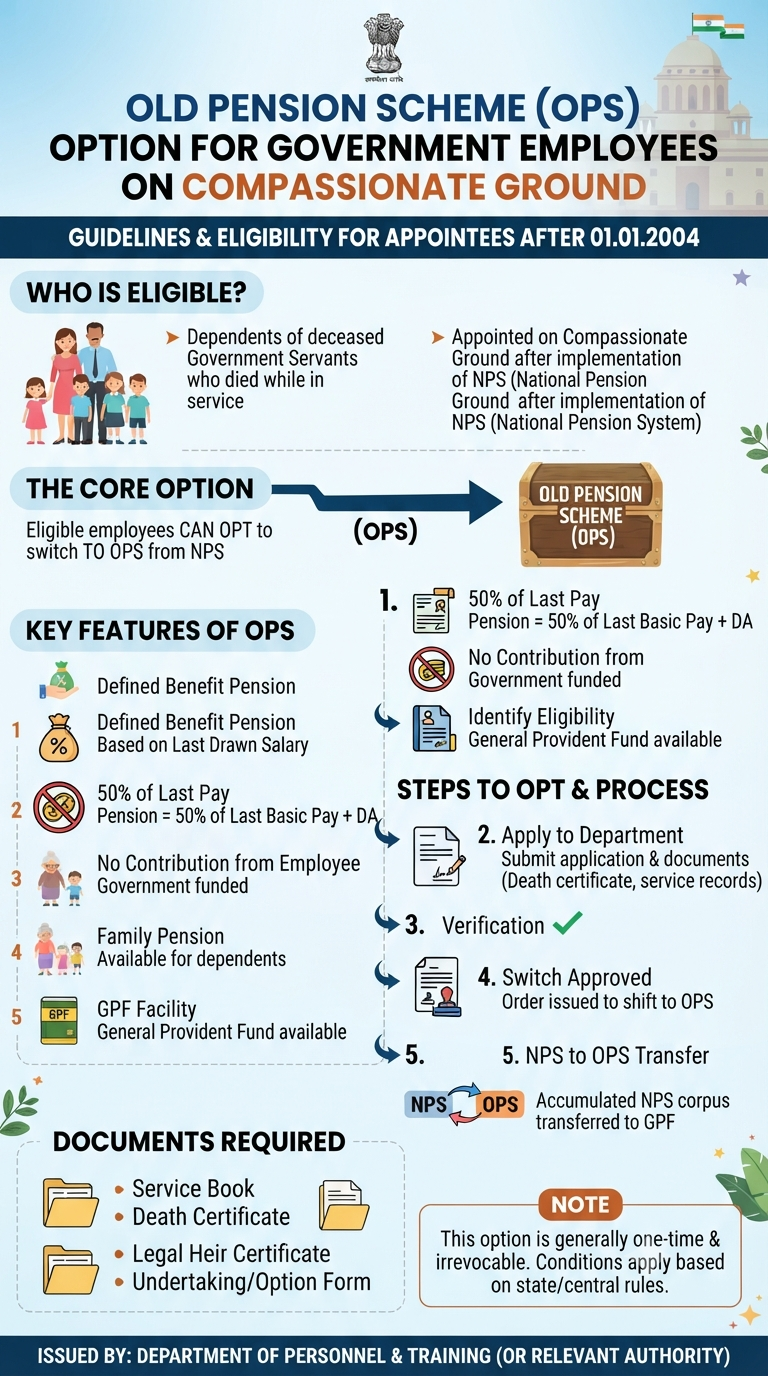

For thousands of government employees who entered service through the compassion of a family-related appointment, the transition into their careers was often marked by a bureaucratic “what-if.” Many had applied for their positions before the cutoff of December 2003, only to join service after the National Pension System (NPS) had already taken hold in January…

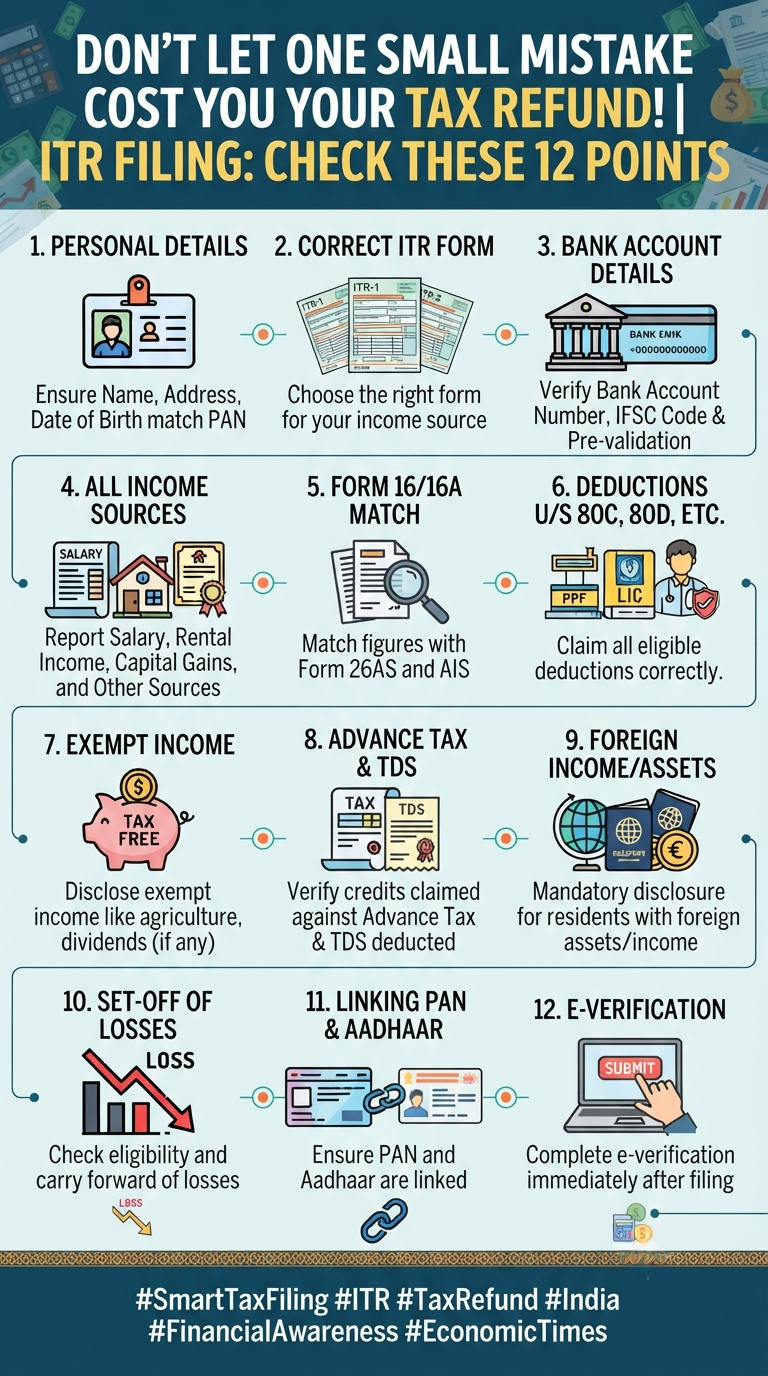

Filing your Income Tax Return (ITR) can often feel like a chore—a necessary evil that we rush through just to get it off our to-do list. But here is the reality: a single typo or a missed detail can be the difference between getting a swift tax refund and getting stuck in a bureaucratic nightmare.…

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.