If you’ve been meticulously planning your retirement and using the Voluntary Provident Fund (VPF) as your go-to “set it and forget it” investment vehicle, you’re not alone. It’s a favorite for conservative investors who love the safety, the government backing, and those consistent returns that often outshine standard savings instruments.

But, if you’ve been pumping significant portions of your salary into VPF to maximize your corpus, you might have noticed a shift in how your statement looks since 2021. The “tax-free” nature of VPF isn’t quite as blanket as it used to be.

Let’s break down the “₹2.5 Lakh Threshold” rule without the jargon, so you can decide if it still makes sense for your financial strategy.

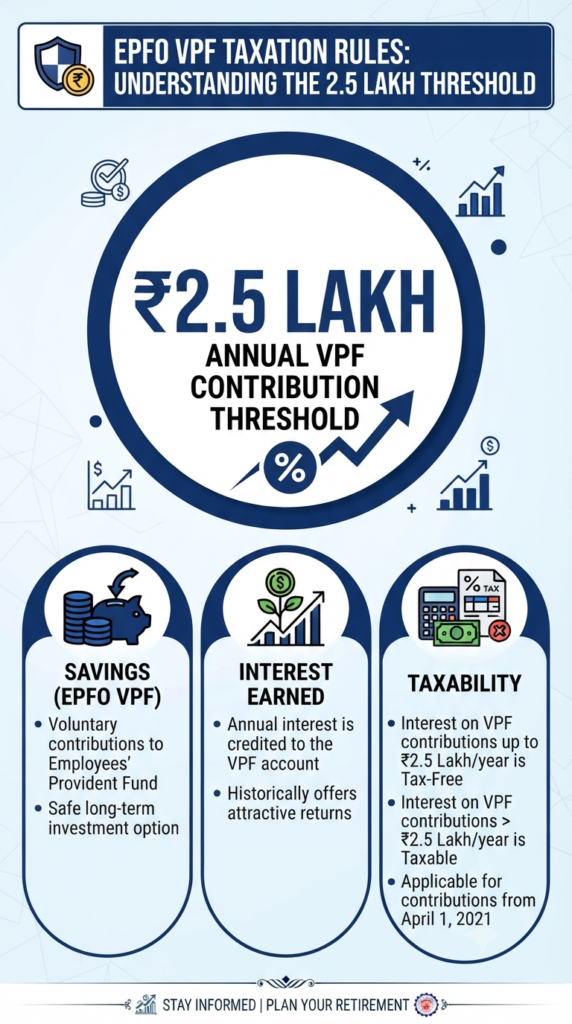

The New Reality: The 2.5 Lakh Limit

Historically, VPF was a haven where your contributions and the interest they generated were entirely tax-free. However, to curb tax-free accumulation for high-income earners, the government introduced a cap.

Here is the simple version:

- The Cap: Your total annual EPF contribution (that’s your mandatory 12% contribution + any voluntary VPF contributions) is now tracked against a ₹2,50,000 annual limit.

- The Catch: If your combined annual contribution crosses that ₹2.5 lakh mark, any interest earned on the amount exceeding that threshold is no longer tax-free.

- The Cost: That excess interest is added to your annual taxable income and taxed according to your personal income tax slab.

Note: If you work for an organization where the employer does not contribute to the EPF, this threshold is actually doubled to ₹5,00,000.

How It Looks on Paper

To keep things transparent, the EPFO now effectively maintains your provident fund account in two “buckets”:

- Non-Taxable Contribution Account: This tracks everything up to your ₹2.5 lakh threshold. The interest here remains blissfully tax-free.

- Taxable Contribution Account: This is where the excess contributions go. Any interest generated by this specific bucket is flagged for taxation.

Is VPF Still Worth It?

It’s easy to get discouraged when you see the word “taxable,” but don’t close your VPF account just yet. Here is why it remains a solid choice for many:

- Still a Powerhouse: VPF continues to offer the same attractive interest rates as the standard EPF (currently 8.25% p.a.). Even after paying tax on that excess interest, it often remains more competitive than many other debt instruments.

- Section 80C Benefits: Your VPF contributions still qualify for tax deductions under Section 80C, up to ₹1.5 Lakhs. That’s an immediate tax saving that applies regardless of whether the interest is taxable or not.

- Discipline: The biggest benefit of VPF isn’t just the math—it’s the forced savings mechanism. By deducting it directly from your salary, you ensure your retirement corpus grows before you even have a chance to spend that money elsewhere.

The Bottom Line

The VPF is still a robust, safe, and effective tool for long-term wealth creation. This tax rule isn’t meant to punish the average investor; it’s a guardrail for those with very high contributions.

Before you make any changes, look at your current contribution levels and your overall tax bracket. For many, the simplicity and reliable returns of the VPF still outweigh the tax impact on that excess interest. As always, review your goals, consult with your tax advisor, and keep building that retirement nest egg.

Disclaimer: This article is for informational purposes only and does not constitute financial or tax advice. Please consult with a qualified professional regarding your specific financial situation.

The Great Salary Shift: Decoding the Labour Codes and the EPF Cap Myth

When you’re staring at the fruit bowl wondering which snack will do your heart the most good, it’s easy to feel torn. Do you reach for the convenient banana or the zesty, refreshing orange? Both are nutritional powerhouses, but they bring different strengths to your cardiovascular game. Let’s break down how these two favorites measure…

Continue Reading Heart-Healthy Snacking: The Battle of the Fruits

Buying a home is one of life’s biggest milestones. For most people, it’s not just a house—it’s a long-term investment in their future and a place to build a life. But with such a massive price tag, a fundamental question arises: Should I save up and pay cash, or should I take out a home…

Continue Reading The Ultimate Showdown: Is it Better to Buy Your Dream Home with Cash or a Mortgage?

Let’s be honest: tracking down old Provident Fund (PF) accounts from past jobs feels like a chore no one wants to tackle. Between the mountain of forms, the fear of losing service history, and the sheer time it takes, many of us just leave our old accounts sitting idle. But what if you could clean…

Continue Reading Say Goodbye to Paperwork: How to Consolidate Your EPF Accounts Online

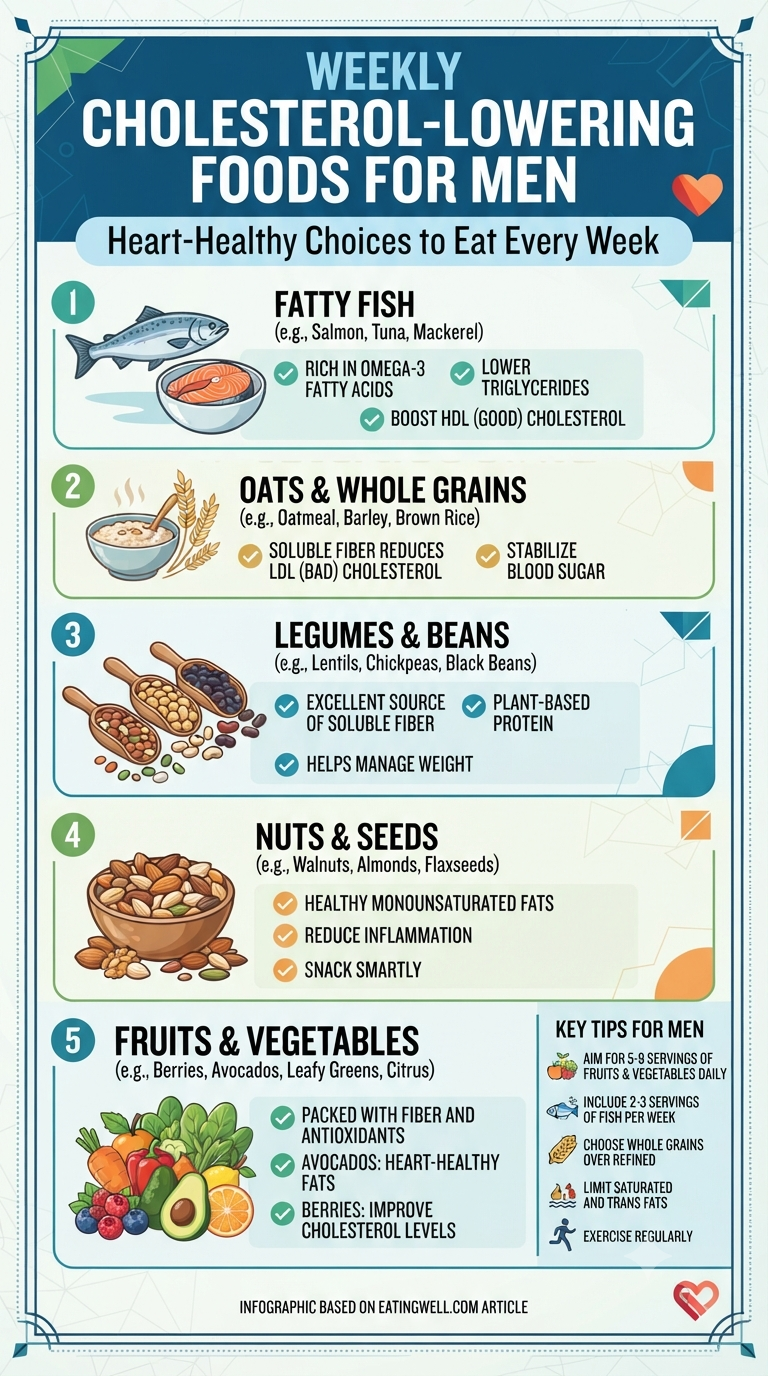

When it comes to longevity, men often focus on building muscle or increasing stamina, but there is a silent powerhouse that deserves just as much attention: your cholesterol levels. Managing cholesterol isn’t just about what you don’t eat—it’s about what you do add to your plate. If you’re looking for a simple, actionable way to…

Continue Reading Take Control of Your Heart Health: 5 Simple Foods to Add to Your Weekly Routine

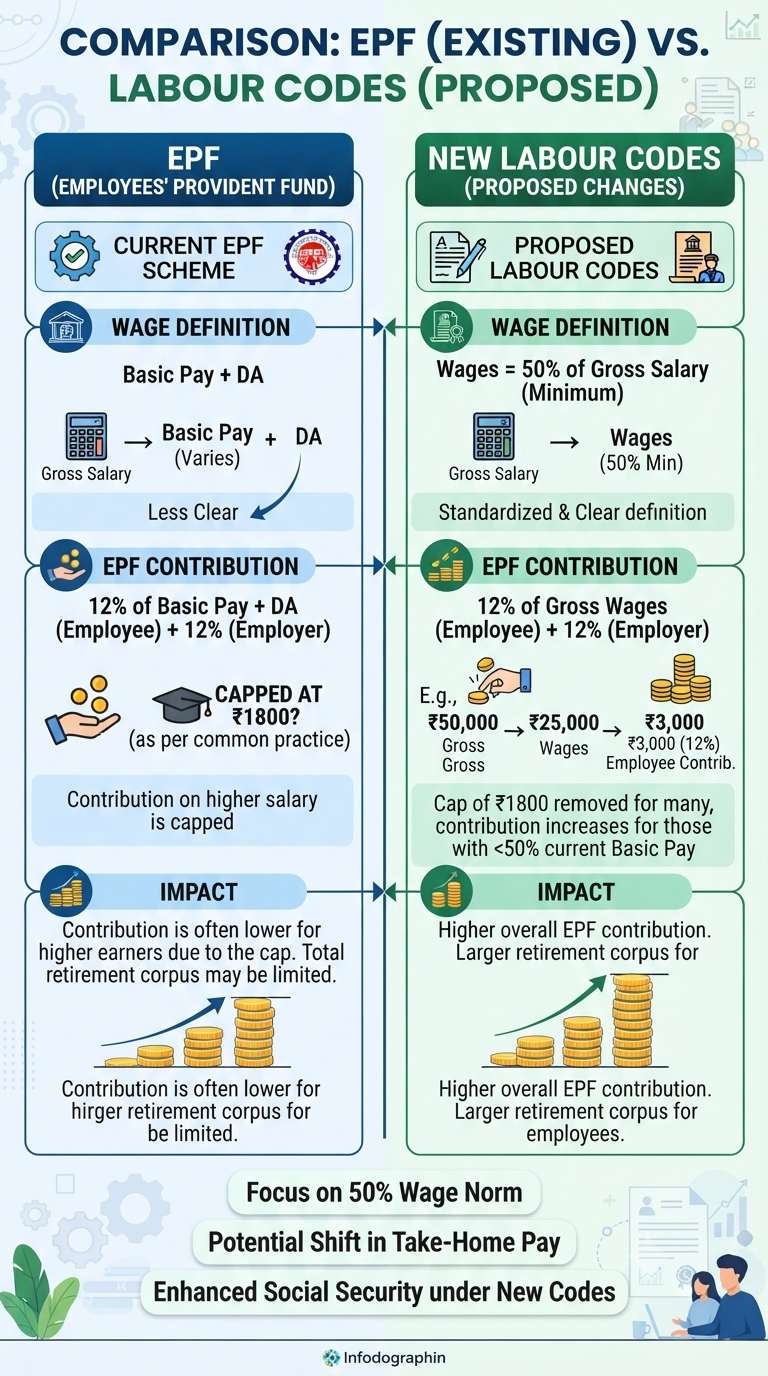

If you’ve recently opened your payslip with a sense of bewilderment, you aren’t alone. Between the buzz surrounding India’s new Labour Codes and the persistent questions about that mysterious ₹1,800 Provident Fund (PF) cap, the world of personal finance can feel like a labyrinth. But what exactly is changing, and more importantly, what does it…

Continue Reading The Great Salary Shift: Decoding the Labour Codes and the EPF Cap Myth

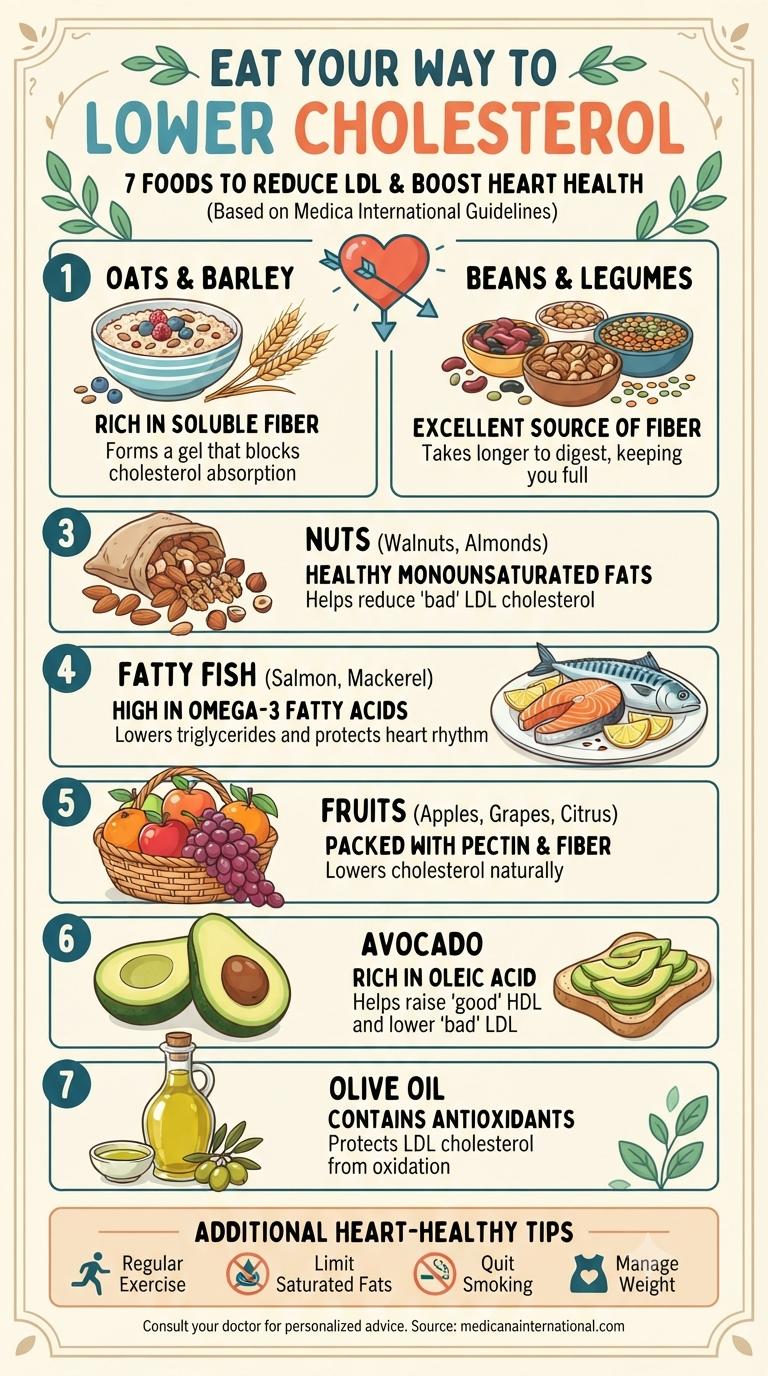

We often hear that “you are what you eat,” and when it comes to heart health, this couldn’t be more true. Cholesterol is a vital substance our bodies use to build cells and produce hormones. However, when levels of low-density lipoprotein (LDL)—often called the “bad” cholesterol—climb too high, it can increase our risk for cardiovascular…

Continue Reading Eat Your Way to a Healthier Heart: A Simple Guide to Lowering Cholesterol

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.