Let’s be honest. When we daydream about retirement, the images aren’t of spreadsheets and calculators. They are visions of sun-drenched beaches, uninterrupted time for hobbies, and the freedom to travel without a ticking clock.

But here’s the reality check: that freedom comes with a price tag. Recently, financial experts have suggested that for a comfortable lifestyle, a retirement corpus in the range of ₹8.1 Crore to ₹10.8 Crore might be necessary for someone spending ₹1 lakh a month today.

That number can feel like a punch to the gut. It’s enormous. It’s intimidating. And for many, it feels completely out of reach.

But don’t panic. Panic doesn’t build wealth; strategy does. That massive number isn’t a wall; it’s just a very high mountain that you can climb with the right guide. That’s exactly what this infographic is—a strategic roadmap to securing your golden years.

Let’s break it down, step by step.

Step 1: Define Your Retirement Goals (The “Why”)

You wouldn’t start a road trip without knowing your destination, right? Retirement is the same. The size of your corpus depends entirely on the lifestyle you want.

- Lifestyle: Are you aiming for a simple life of gardening and local volunteering, or a luxury lifestyle of international travel and fine dining?

- Location: Retiring in a quiet suburb is very different from retiring in a bustling metro.

- Travel: How often, and how far, do you want to fly?

Actionable Tip: Don’t just think about it. Write down your vision. A clear “why” makes the “how” much easier to stomach.

Step 2: Estimate Your Required Corpus (The “What”)

Now, we put math to your vision. This is where that ₹8.1–₹10.8 Crore figure comes from. It’s not a random guess; it’s a calculation based on three critical factors:

- Your Current Expenses: You start with your baseline (e.g., ₹1 lakh/month).

- Inflation: This is the silent killer. At a modest 6% inflation rate, the cost of living doubles roughly every 12 years. The ₹1 lakh lifestyle you have today will cost you ₹2 lakh in 12 years, and ₹4 lakh in 24 years. Your retirement pot needs to account for this staggering rise in costs.

- Life Expectancy: Thanks to modern medicine, we are living longer. Your retirement could last 30 years or more. Your money needs to outlive you.

Step 3: Start Saving Early & Invest (The “How”)

This is the single most important piece of the puzzle. Time is your greatest asset.

- The Power of Compounding: This is magic. When you invest early, your money earns returns, and then those returns earn returns. A small amount invested in your 20s will grow to be exponentially larger than a much larger amount invested in your 40s.

- Consistent Contributions: It’s not about timing the market; it’s about time in the market. Regular, disciplined investing, like a monthly SIP (Systematic Investment Plan), is the most effective way to build wealth.

The Takeaway: The best time to start investing was yesterday. The second-best time is today.

Step 4: Choose Right Asset Allocation (The “Engine”)

You can’t just keep your money in a savings account. Inflation will eat it alive. You need your money to work harder for you. This is where asset allocation comes in—spreading your investments across different “buckets” to balance risk and return.

- Equities (Growth): The growth engine. Historically, equities provide the highest long-term returns, essential for beating inflation and building that multi-crore corpus. The infographic recommends a significant allocation (e.g., 40%–60%) here for long-term growth.

- Debt (Stability): The safety net. This includes bonds and fixed income. It offers stability and preserves capital, protecting you from the volatility of the stock market. (e.g., 30%–40%).

- Alternatives/Gold (Hedge): The insurance policy. Gold and real estate act as a hedge against inflation and currency fluctuations, adding another layer of security. (e.g., 10%–20%).

Step 5: Monitor and Rebalance Periodically (The “Check-up”)

Your life isn’t static, and the market isn’t either. This plan isn’t “set it and forget it.”

- Life Events: A promotion, a child’s education, an inheritance—all of these change your financial picture.

- Market Changes: If the stock market soars, your equity allocation will grow beyond your target, making your portfolio riskier. If it drops, your allocation will shrink.

- Rebalancing: At least once a year, you need to “rebalance.” This means selling some of what has done well and buying more of what has lagged, bringing your portfolio back to your target allocation. It forces you to “buy low and sell high.”

Step 6: Secure Retirement Income (The “Paycheck”)

All the accumulation in the world is for one purpose: to provide you with a paycheck when you stop working.

- Systematic Withdrawals: Instead of pulling out lump sums, you set up a regular monthly withdrawal from your corpus.

- Annuities: You invest a portion of your corpus with an insurance company in exchange for a guaranteed, regular income stream for life.

- Pension: Any existing pension acts as a base layer of security.

Final Thoughts: From Intimidation to Inspiration

Yes, an ₹8.1 Crore corpus is a big number. But when you break it down into these six logical, actionable steps, it transforms from a source of anxiety into a clear path forward.

Retirement planning isn’t a sprint; it’s a marathon. You don’t run it by sprinting from the start line. You run it by pacing yourself, staying disciplined, and trusting your training. This infographic is your training plan. The beach is waiting. Let’s get to work.

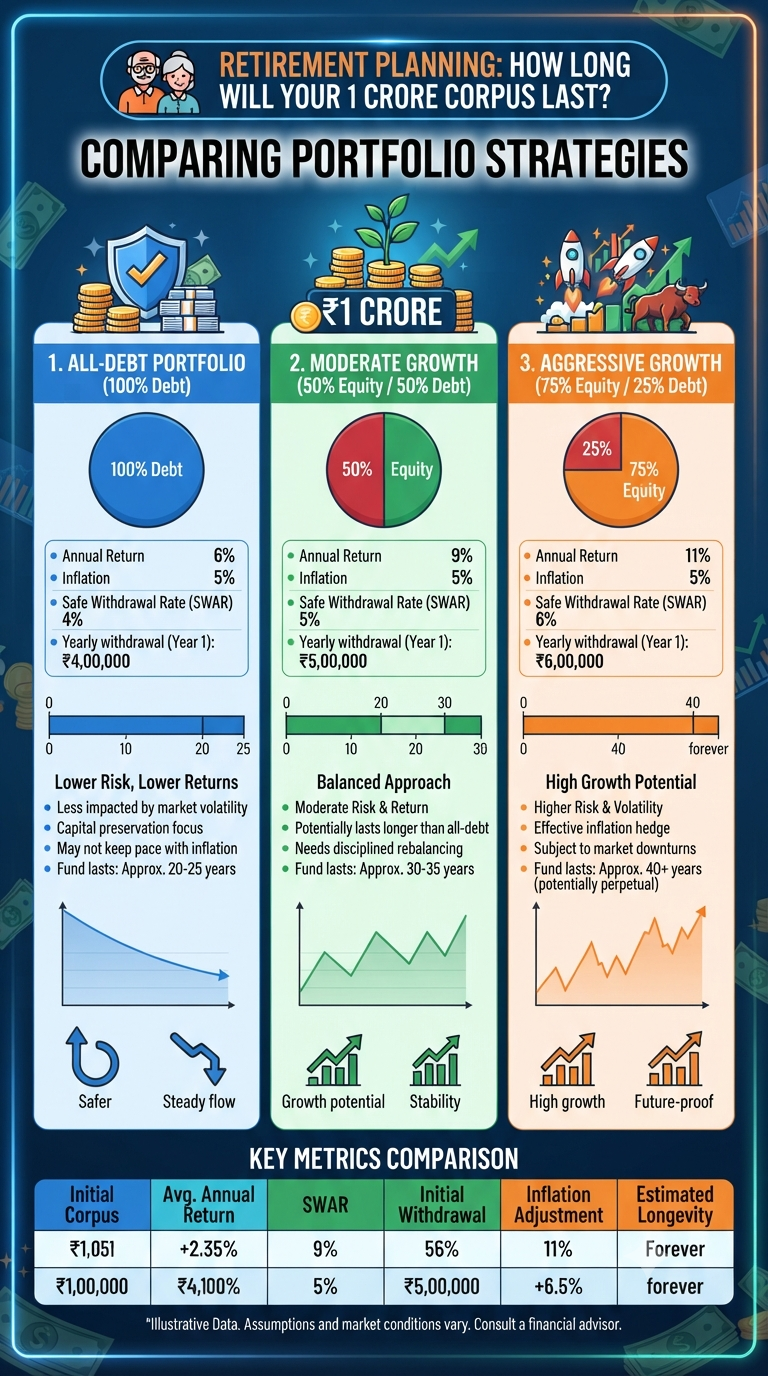

Double Your Money Safely: A Deep Dive into Kisan Vikas Patra (KVP)

Hitting that ₹1 Crore milestone feels like a massive achievement, doesn’t it? It’s the number we all dream of when we think about hanging up our boots and trading the morning commute for leisurely mornings. But as you sit back and look at that accumulated wealth, a nagging question often creeps in: Will this actually…

Continue Reading Retirement Planning: Can Your ₹1 Crore Nest Egg Stand the Test of Time?

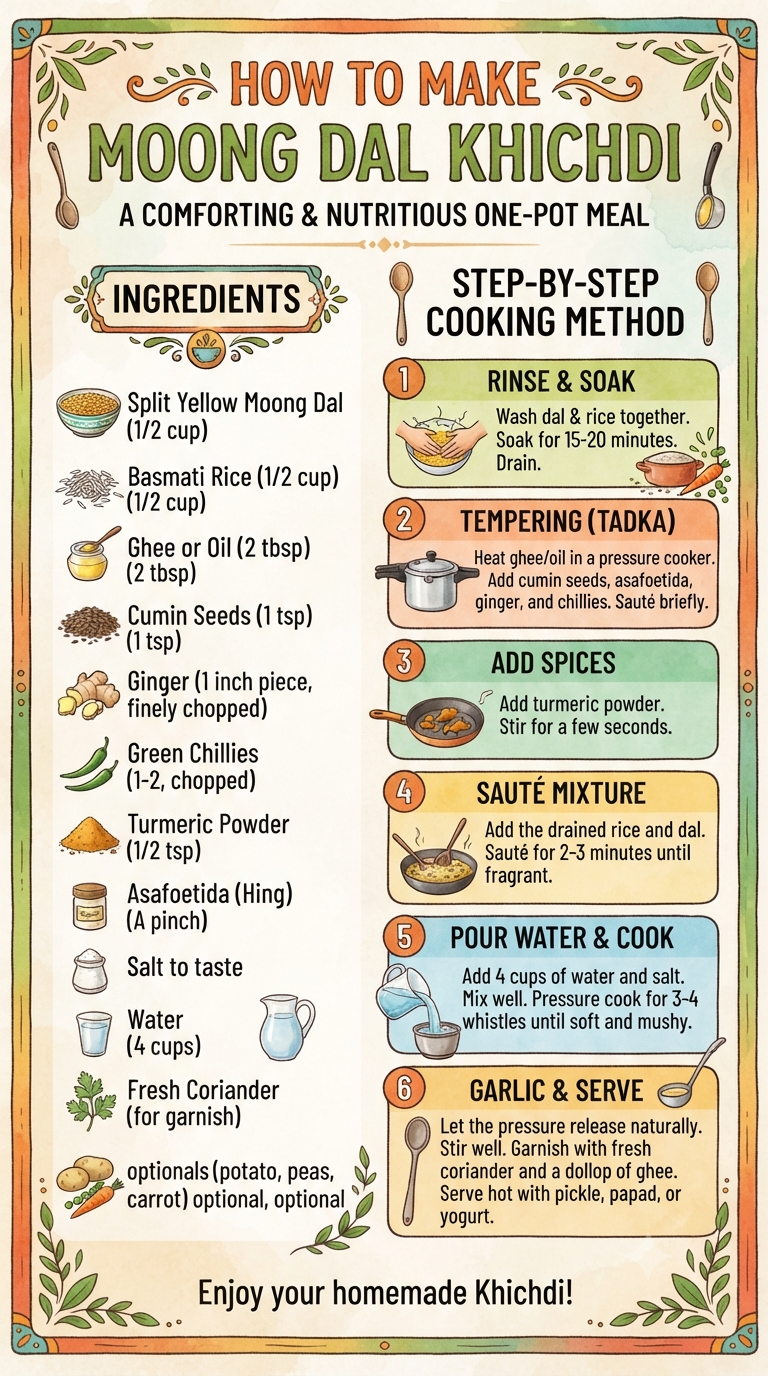

In our fast-paced lives, finding a meal that is both deeply comforting and genuinely healthy can feel like searching for a unicorn. We often default to heavy, overly processed foods when we crave comfort, only to feel sluggish and regretful afterward. But what if I told you there’s a dish that is the culinary equivalent…

We have all been there—that uncomfortable, tight feeling in your stomach after a heavy meal. Bloating and gas are incredibly common, but they can certainly put a damper on your day. While it might be tempting to reach for store-bought remedies, sometimes the best solutions are hiding right in your kitchen pantry. If you are…

Continue Reading Gas Relief in a Glass: 5 Simple Drinks to Ease Bloating Fast

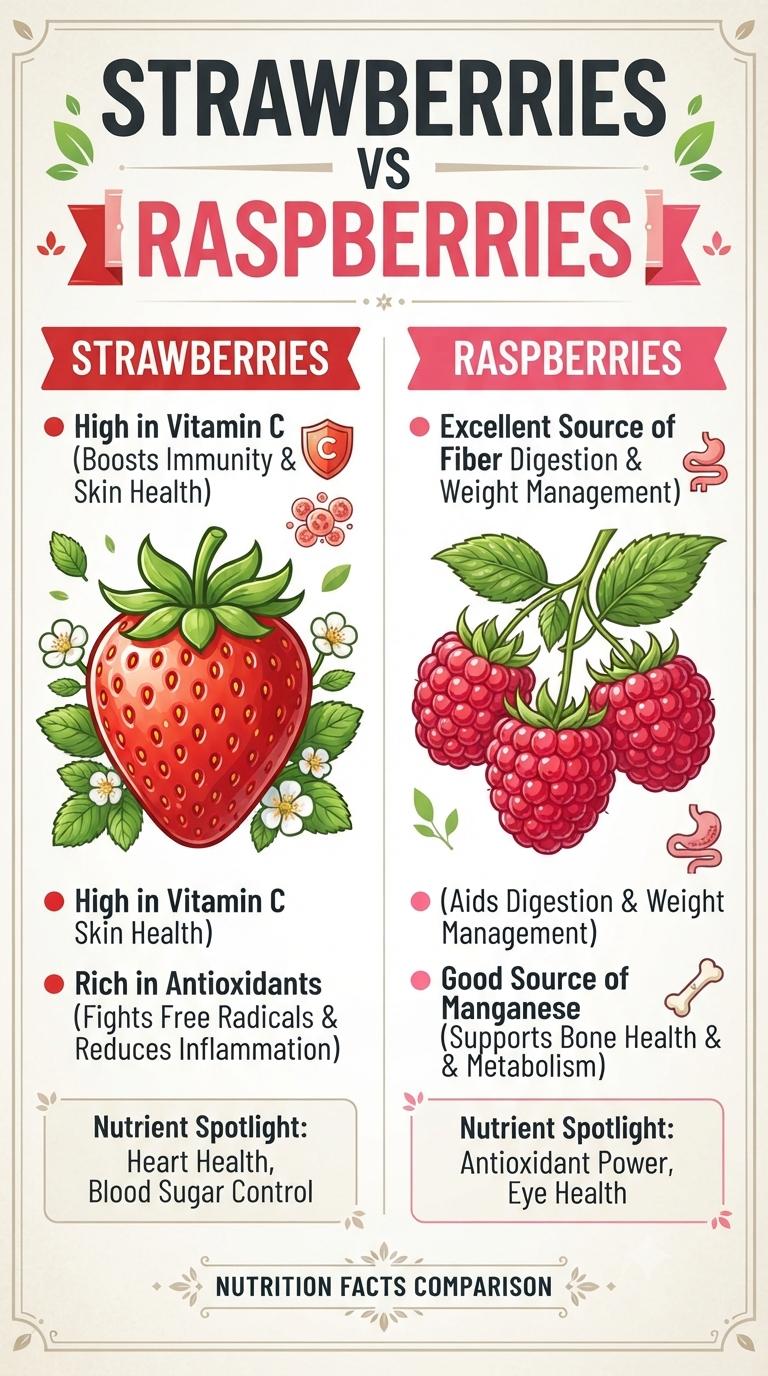

When it comes to the produce aisle, it’s easy to find yourself in a standoff. You’re standing there, basket in hand, weighing the vibrant, glossy red of a punnet of strawberries against the delicate, complex structure of a pint of raspberries. They’re both delicious, they’re both beautiful, and they both scream “summer.” But if you’ve…

We all crave that perfect, soft, and glossy smile, but let’s be honest—our lips are high-maintenance. Because the skin on our lips is incredibly thin and delicate, they are often the first part of our face to show signs of dryness, flaking, or cracking. While the market is flooded with synthetic balms and treatments, nature…

Continue Reading Unlock Your Best Smile: The Ultimate Guide to Naturally Soft and Hydrated Lips

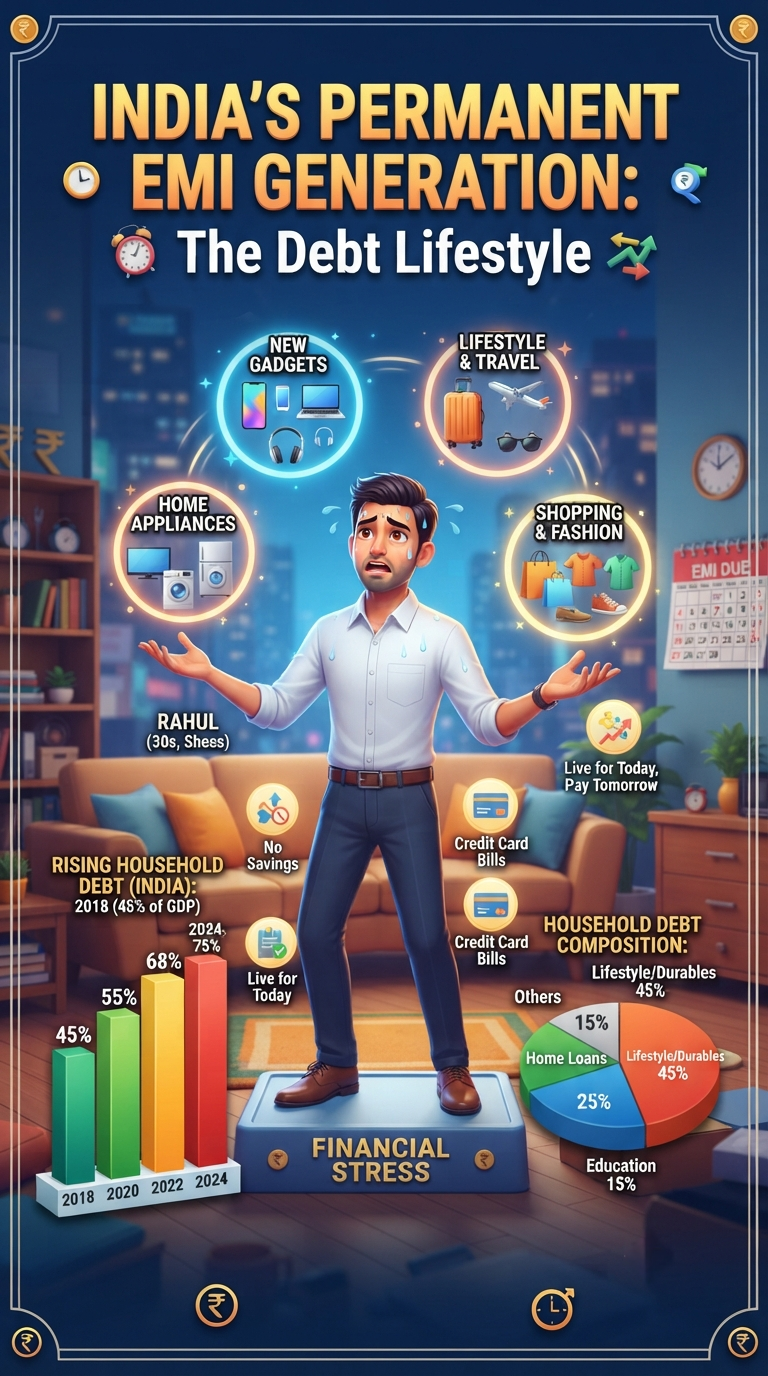

Have you ever noticed how your salary seems to evaporate the moment it hits your bank account? You work hard all month, but by the time you’ve paid off your credit card bill, the EMI for that smartphone you bought six months ago, and the installment for your last vacation, there’s barely enough left to…

Continue Reading The “Always-On” EMI Trap: Why Your Salary Is Disappearing Before You Even Get It

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.