For many employees in India, the Employees’ Provident Fund (EPF) represents a critical financial safety net. With recent updates from the Employees’ Provident Fund Organisation (EPFO), understanding how and when you can access these funds is more important than ever.

Whether you are planning for major life milestones or navigating an unexpected emergency, knowing the rules is the first step toward smart financial management.

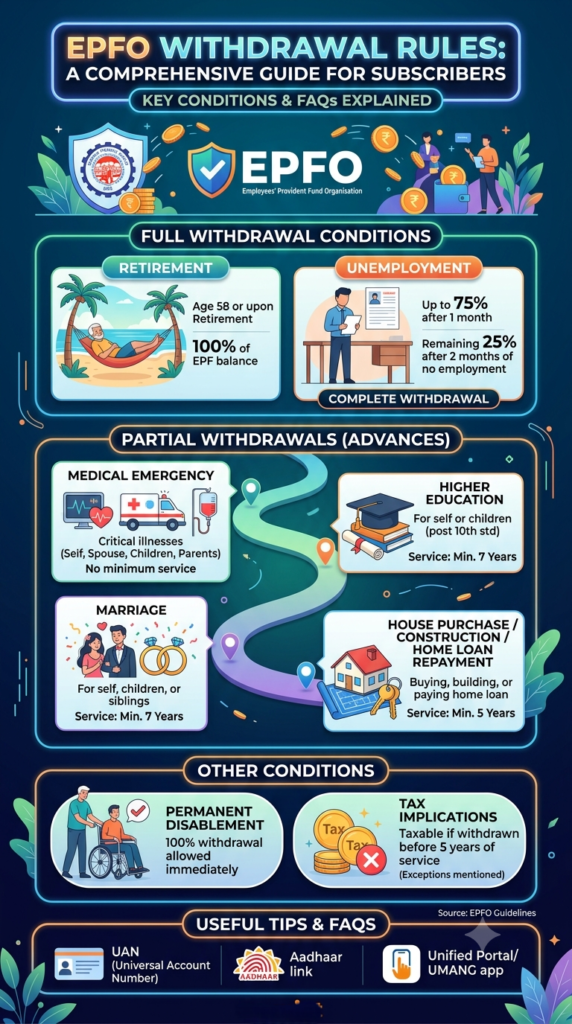

Understanding the “Eligible Balance”

A common question among subscribers is whether they can withdraw 100% of their provident fund. While the EPFO allows for significant access, the current framework encourages members to maintain a portion of their corpus. You are essentially eligible to withdraw up to 75% of your current balance, with the remaining 25% serving as a buffer. This strategy is designed to ensure that you continue to benefit from the competitive interest rate—currently 8.25% per annum—and the power of compounding to secure your long-term retirement goals.

When Can You Withdraw?

The EPFO categorizes withdrawals into full settlements and partial advances:

- Full Withdrawal: Generally permitted upon retirement (at age 58) or in cases of unemployment. If you resign from a job, you are eligible to withdraw after a mandatory two-month waiting period.

- Partial Withdrawals (Advances): These are designed to provide liquidity for specific life needs. Members can tap into their PF for:

- Medical Emergencies: Available for self, spouse, children, or parents, with no minimum service requirement.

- Higher Education: Available for self or children after completion of the 10th standard, provided the member has at least 7 years of service.

- Marriage: Applicable for self, children, or siblings, requiring a minimum of 7 years of service.

- Housing: Funds can be used for purchasing or constructing a house or repaying a home loan, with a minimum service requirement of 5 years.

Important Considerations: Tax and Digital Access

Before applying for a withdrawal, keep these administrative details in mind:

- Tax Implications: If you withdraw your EPF after less than five years of service and the accumulated amount exceeds ₹50,000, TDS (Tax Deducted at Source) may be applicable. Providing your PAN is essential; failing to do so may result in TDS being deducted at the maximum marginal rate of 34.606%.

- Streamlined Access: To simplify the process, the auto-settlement limit has been increased to ₹5 lakh, which can help eligible members receive their funds within just three days.

- Digital Tools: Ensure your Universal Account Number (UAN) is active and linked with your Aadhaar and bank account. This connectivity allows for a “composite claim,” which removes the need for employer attestation on your application form.

Note: The EPFO periodically conducts system upgrades. Always check the official website or the UMANG app for any service downtime before planning your withdrawal request.

Planning for Life After Your PPF Matures: Your 3 Smart Options

Are you tired of watching your hard-earned savings get eaten away by inflation? Many of us are constantly on the lookout for the perfect balance between growing our wealth and keeping it safe. In a world full of volatile market trends, there is a certain peace of mind that comes with government-backed investments. As we…

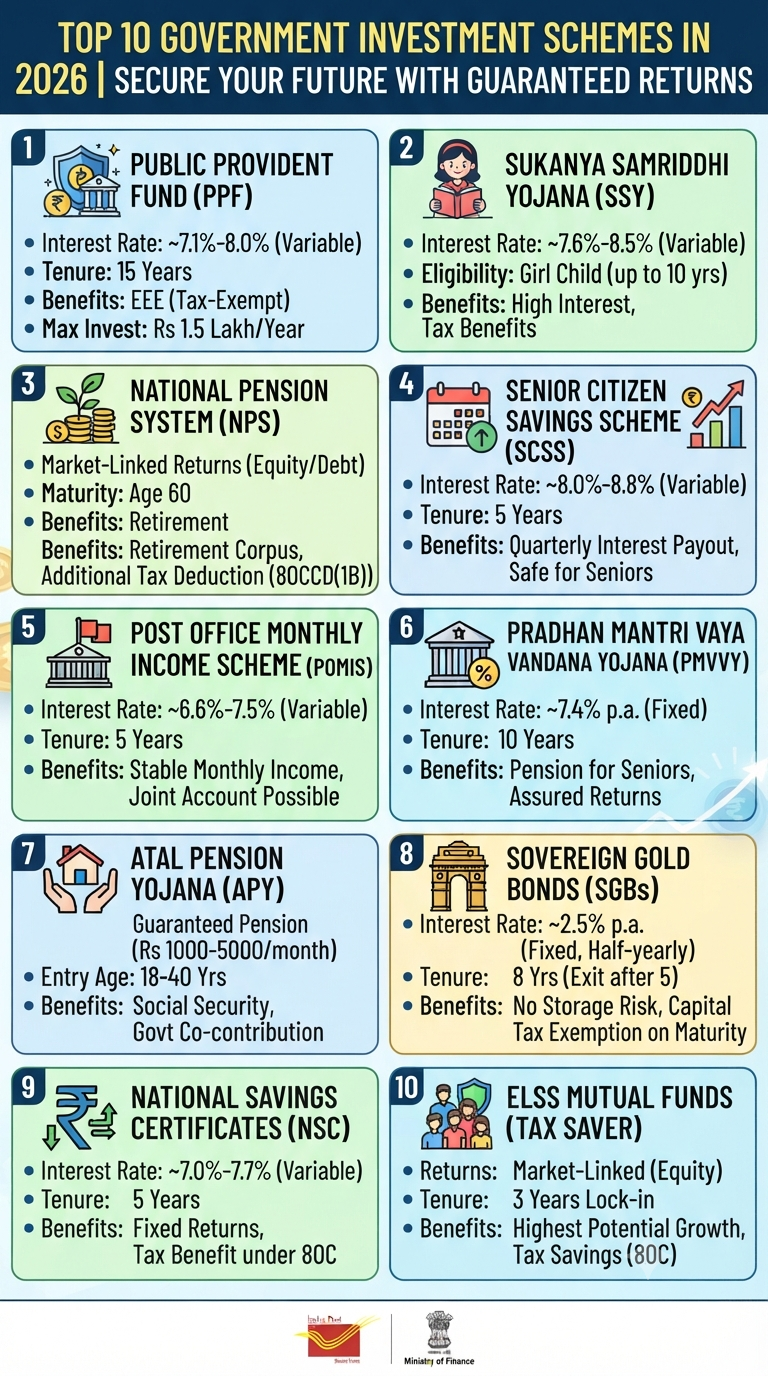

Continue Reading Secure Your Future: Top 10 Government Investment Schemes to Consider in 2026

In today’s volatile financial landscape, where stock markets can swing wildly and inflation constantly erodes the value of idle cash, finding a safe harbor for your savings is more important than ever. But what if that safe harbor could also provide a significant, guaranteed return? If you are sitting on a surplus of funds—perhaps a…

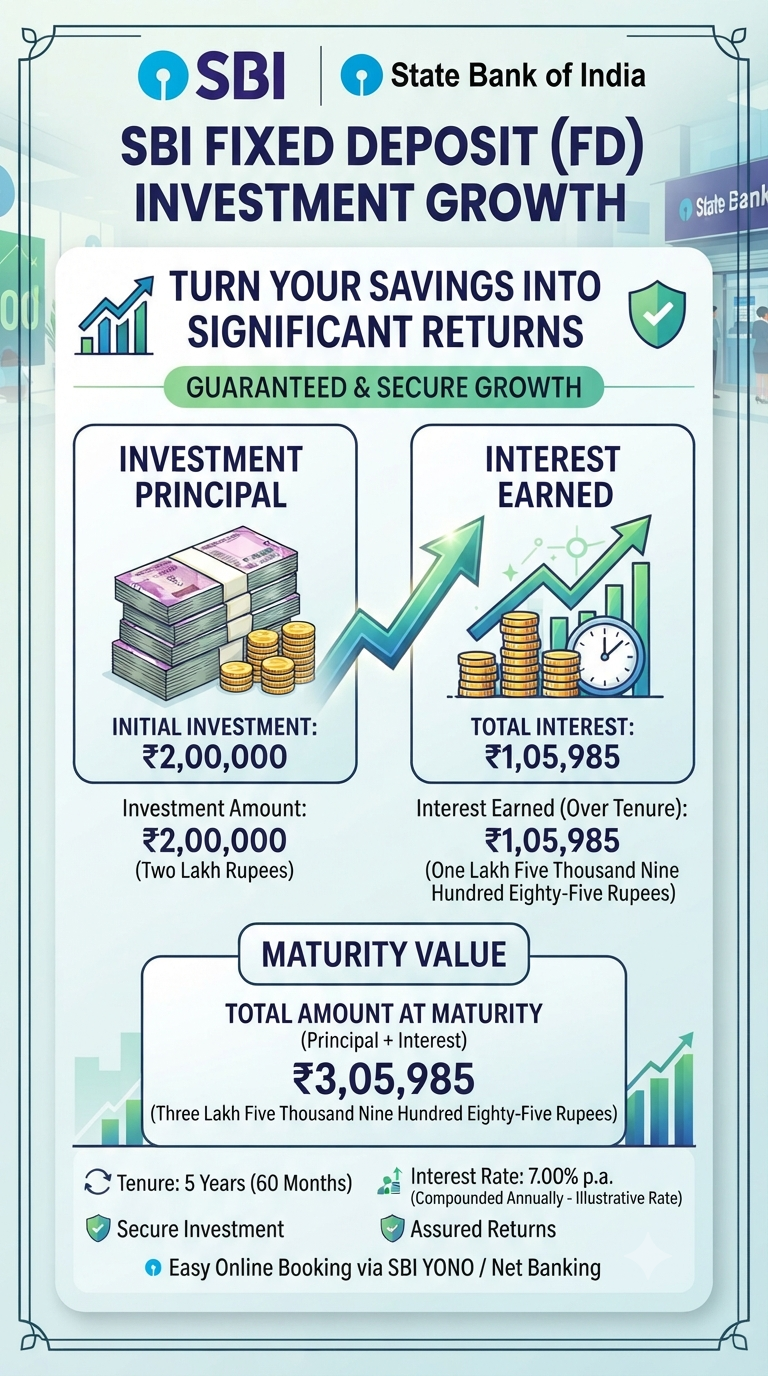

Continue Reading Turn ₹2 Lakhs into ₹3+ Lakhs: A Smart Investor’s Guide to SBI Fixed Deposits

When it comes to putting your money to work, the “Post Office” is often the first place that comes to mind for many of us. It’s reliable, government-backed, and feels like home. But if you have ₹50,000 ready to invest, you might find yourself at a crossroads: Should you go for a Fixed Deposit (FD)…

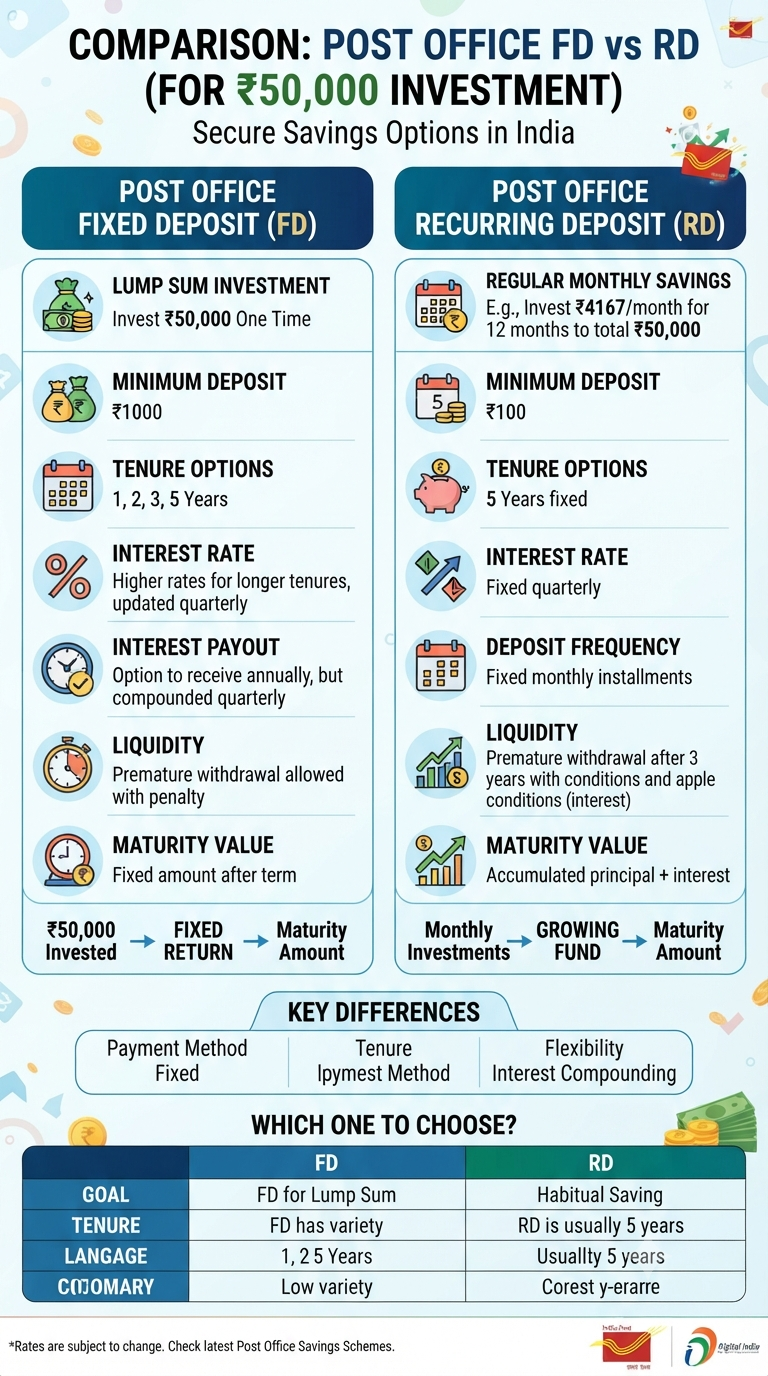

Continue Reading Invest Wisely: Choosing Between Post Office FD and RD for Your Savings

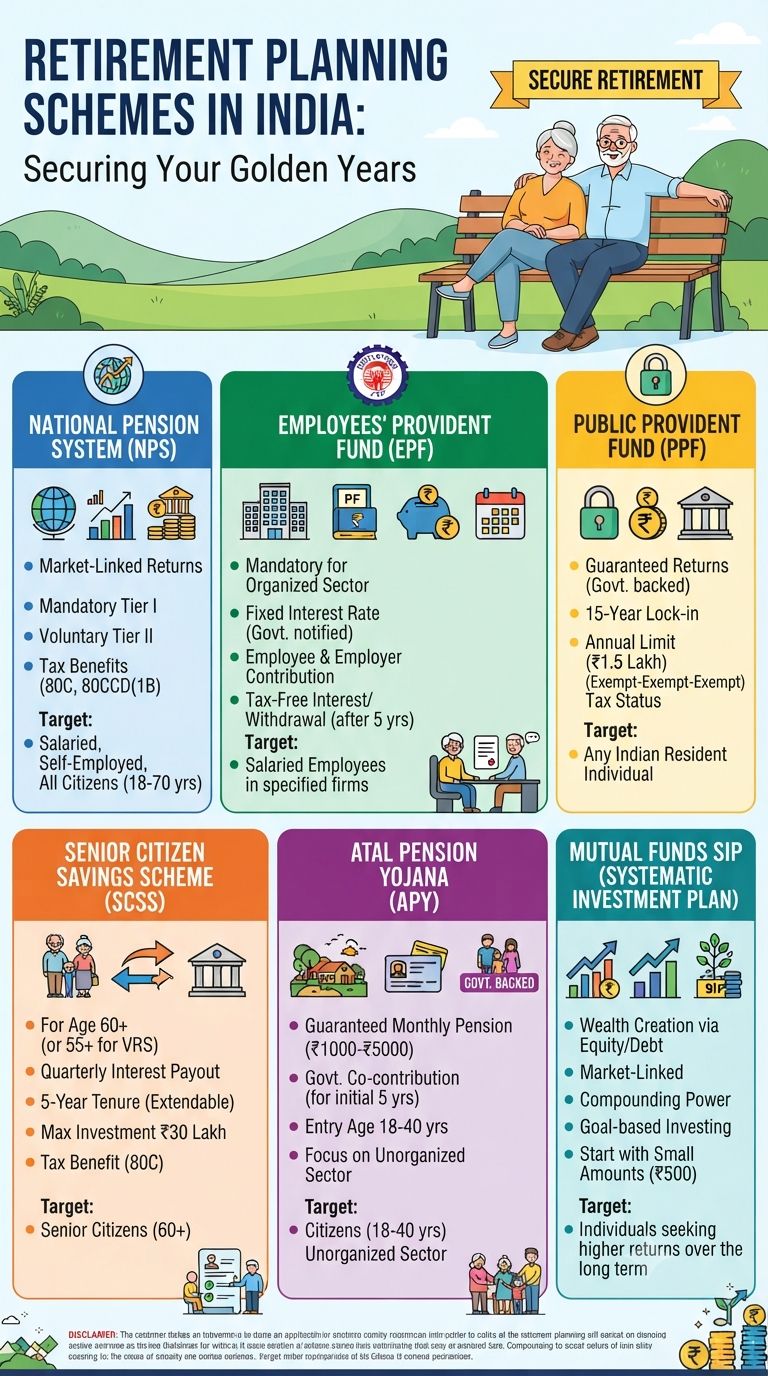

Retirement is not just a destination; it is a meticulously planned journey. While we spend our working lives building careers and managing daily expenses, the most critical investment we make is the one for our future selves. In India, the landscape of retirement planning has evolved significantly, offering a mix of government-backed security and market-linked…

Continue Reading Securing Your Golden Years: The Ultimate Guide to Retirement Planning in India

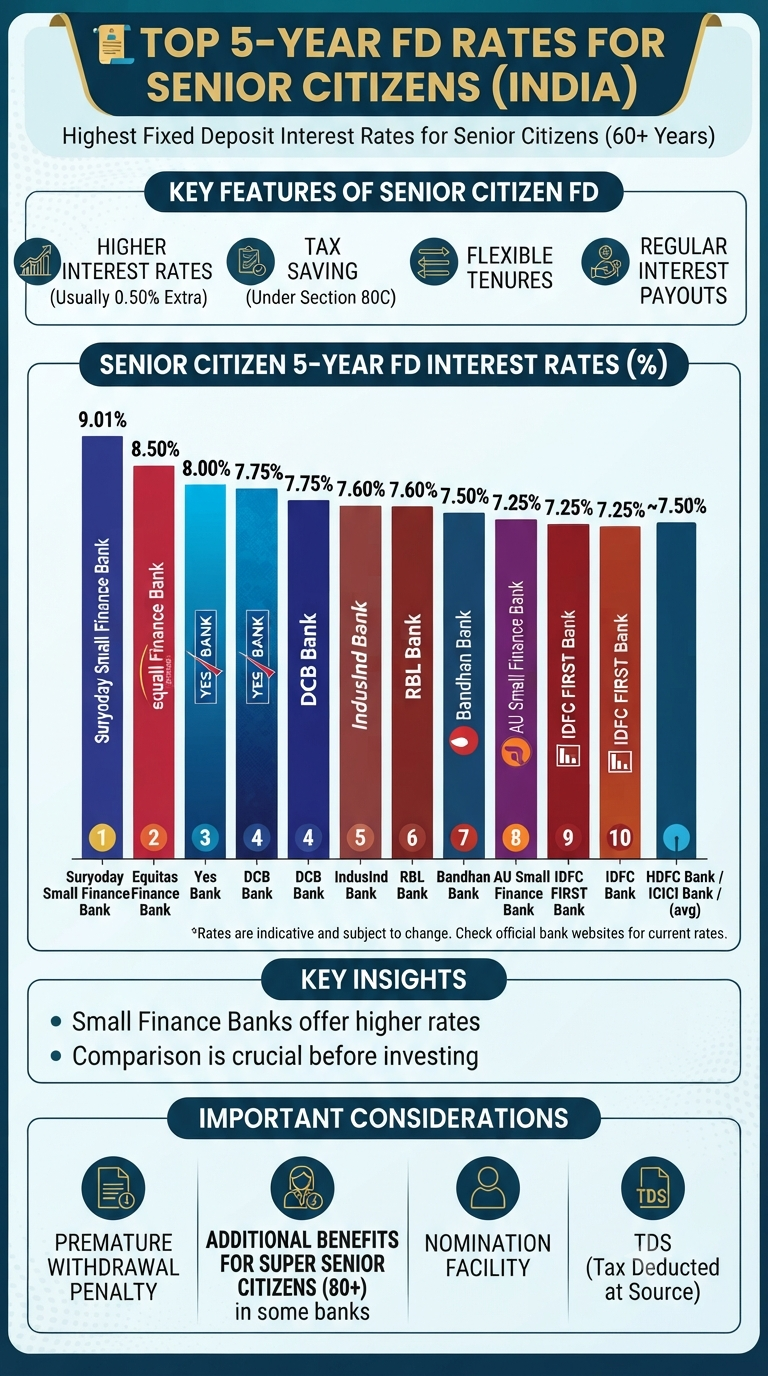

Retirement should be a time of relaxation, travel, and spending quality time with loved ones—not worrying about finances. For many senior citizens in India, Fixed Deposits (FDs) have long been the bedrock of a safe and secure investment strategy. They offer guaranteed returns, capital preservation, and the peace of mind that comes with knowing your…

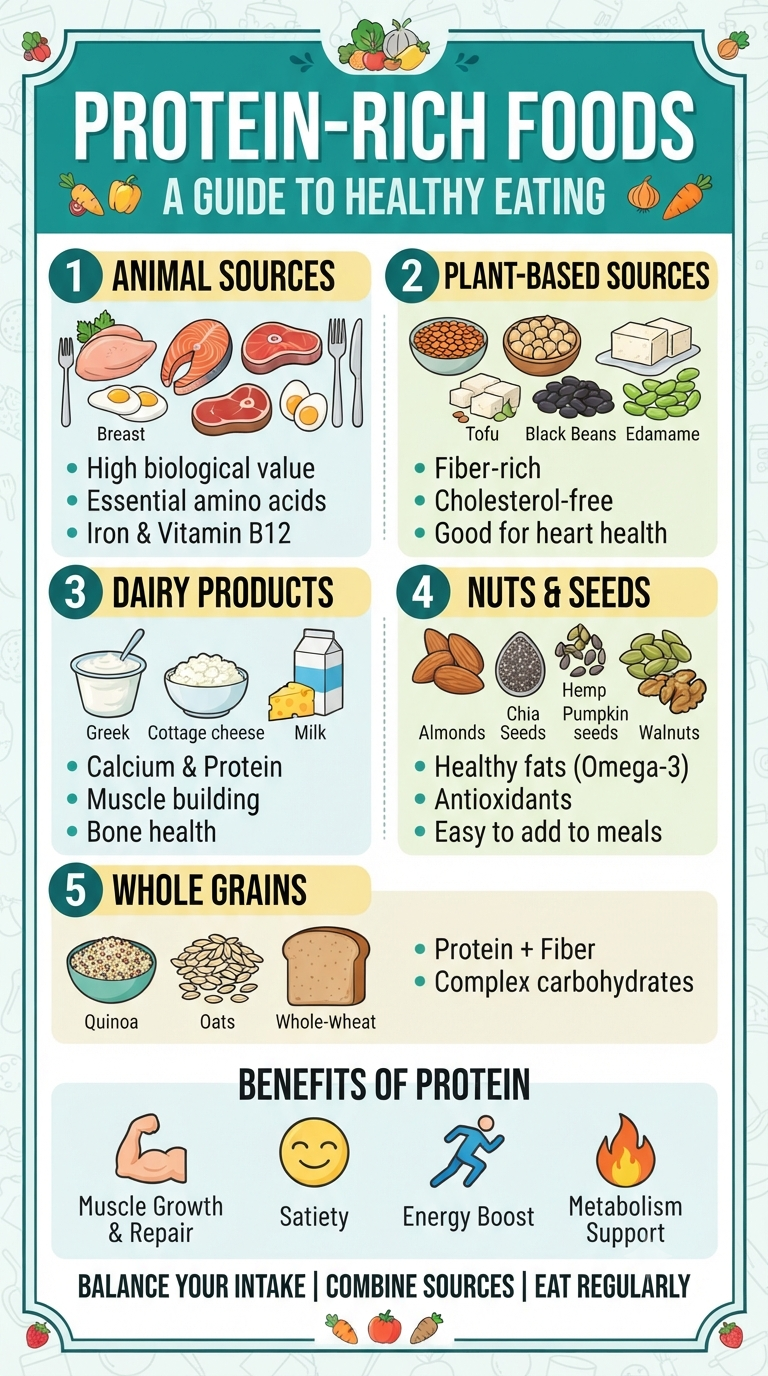

We often hear about the importance of protein, but do you know why it’s truly the MVP of your diet? Protein is the essential building block for our bodies—it’s responsible for everything from repairing muscles after a tough workout to keeping us feeling full and satisfied throughout a busy day. Whether you are looking to…

Continue Reading Power Up Your Plate: The Ultimate Guide to Protein-Rich Eating

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.