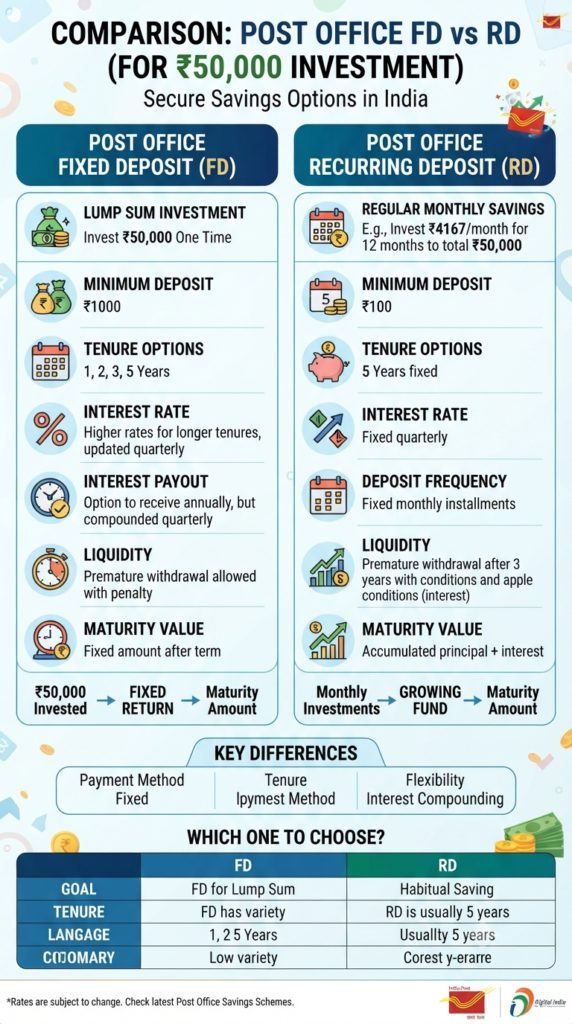

When it comes to putting your money to work, the “Post Office” is often the first place that comes to mind for many of us. It’s reliable, government-backed, and feels like home. But if you have ₹50,000 ready to invest, you might find yourself at a crossroads: Should you go for a Fixed Deposit (FD) or a Recurring Deposit (RD)?

Both are fantastic, safe ways to grow your wealth, but they serve different purposes depending on how you like to handle your money. Let’s break down which one might be the perfect match for your financial goals.

The Fixed Deposit (FD): The “One-and-Done” Powerhouse

Think of the Post Office Time Deposit (FD) as the sprinter of the investment world. You have a lump sum sitting in your account, and you want to lock it away to earn interest without worrying about it every month.

- Best for: When you have a surplus (like a bonus or maturity from another policy) and want to secure it.

- The Vibe: You put in your ₹50,000 once, pick your tenure (1, 2, 3, or 5 years), and let the interest do the heavy lifting.

- The Advantage: It offers higher flexibility in terms of tenure. If you know you’ll need that cash in exactly two years for a specific goal, the FD is your best friend.

The Recurring Deposit (RD): The “Slow and Steady” Builder

The Recurring Deposit is the marathon runner. It’s not about having a large pile of cash today; it’s about building that pile through the power of discipline.

- Best for: Those who don’t have a big lump sum right now but want to invest a part of their monthly income to build a larger corpus over time.

- The Vibe: Instead of parting with ₹50,000 in one go, you might choose to invest, say, roughly ₹4,167 every month for five years. By the end, you haven’t just saved—you’ve grown your wealth through consistent habit.

- The Advantage: It’s a fantastic way to develop financial discipline without feeling the “sting” of a large deduction from your bank balance.

Comparison at a Glance

| Feature | Fixed Deposit (FD) | Recurring Deposit (RD) |

| Investment Style | One-time lump sum | Monthly installments |

| Ideal For | Using surplus cash | Building a habit of saving |

| Tenure | Flexible (1–5 years) | Fixed (5 years) |

| Minimum Entry | ₹1,000 | ₹100/month |

So, Which One Should You Pick?

It really comes down to your current financial stage:

- Choose the FD if: You have the ₹50,000 sitting in your savings account right now. Locking it into a Term Deposit ensures you earn a solid, predictable return, and it’s perfect if you have a specific date in the future when you know you’ll need that money back.

- Choose the RD if: Your goal is to start saving. If you find that the money at the end of the month just “disappears,” the RD is your secret weapon. It forces you to prioritize your future self every single month.

Final Thoughts

There is no “better” scheme—there is only the scheme that fits your life right now. Whether you choose the immediate satisfaction of a Fixed Deposit or the steady growth of a Recurring Deposit, you are making a smart move toward financial security.

Ready to start? Visit your nearest post office or check the official India Post website to get the latest interest rates before you commit!

Disclaimer: Interest rates and terms are subject to change by the Department of Posts. Always consult with a post office official for the most current information before finalizing your investment.

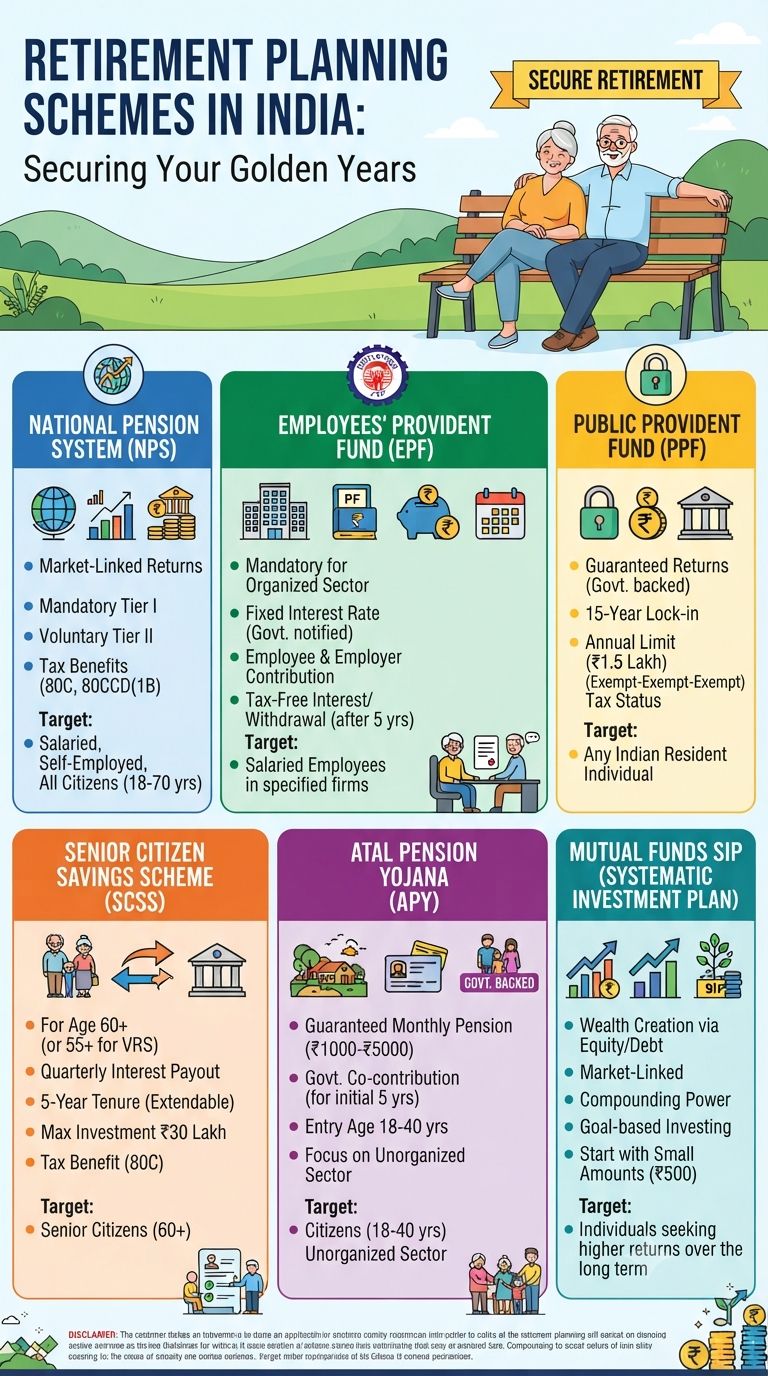

Securing Your Golden Years: The Ultimate Guide to Retirement Planning in India

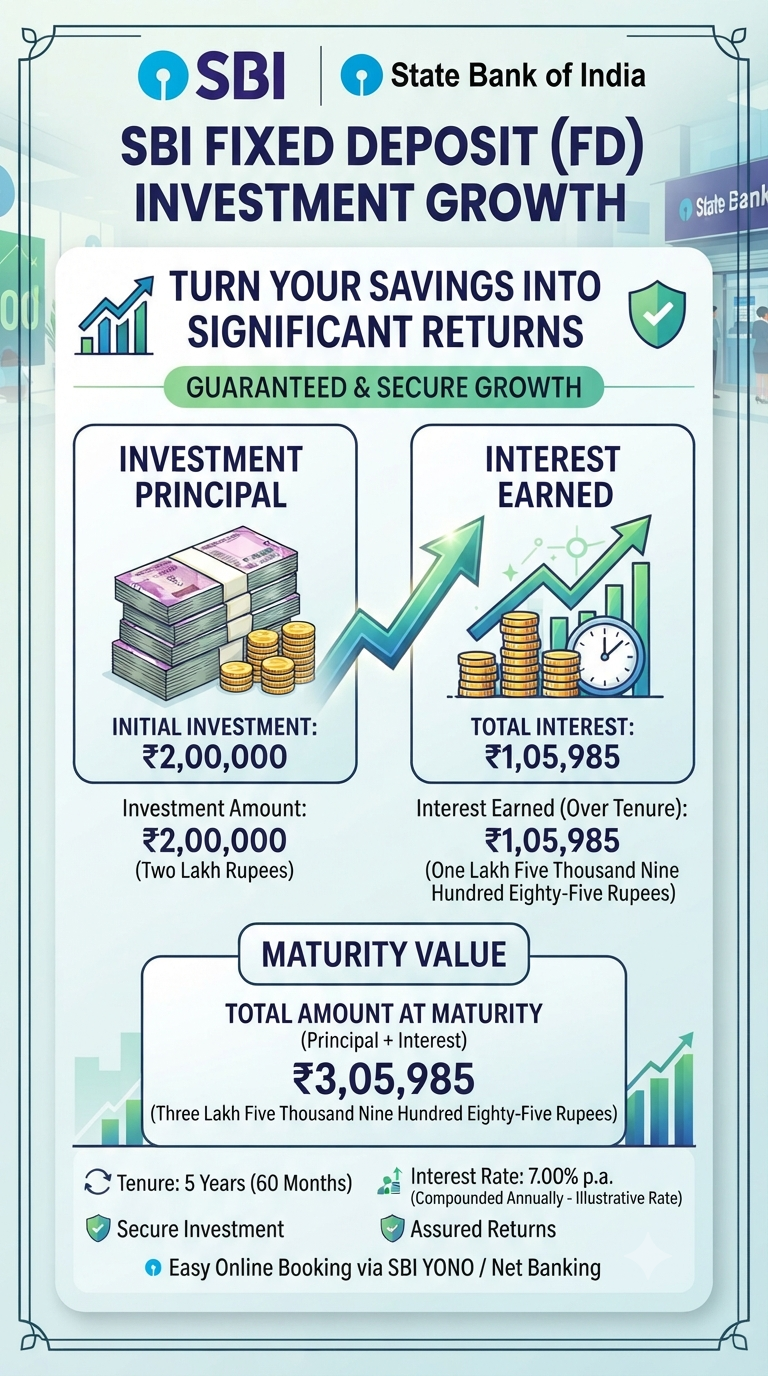

In today’s volatile financial landscape, where stock markets can swing wildly and inflation constantly erodes the value of idle cash, finding a safe harbor for your savings is more important than ever. But what if that safe harbor could also provide a significant, guaranteed return? If you are sitting on a surplus of funds—perhaps a…

Continue Reading Turn ₹2 Lakhs into ₹3+ Lakhs: A Smart Investor’s Guide to SBI Fixed Deposits

Retirement is not just a destination; it is a meticulously planned journey. While we spend our working lives building careers and managing daily expenses, the most critical investment we make is the one for our future selves. In India, the landscape of retirement planning has evolved significantly, offering a mix of government-backed security and market-linked…

Continue Reading Securing Your Golden Years: The Ultimate Guide to Retirement Planning in India

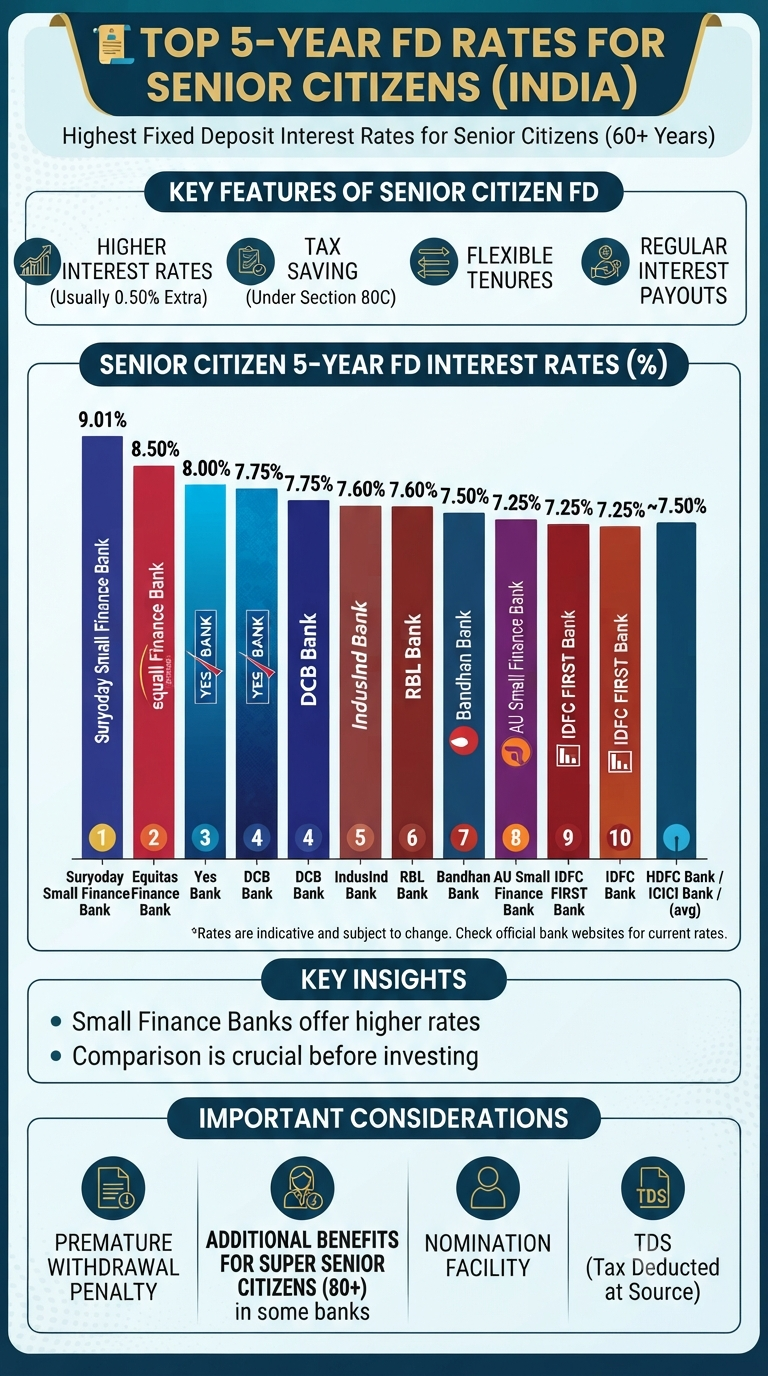

Retirement should be a time of relaxation, travel, and spending quality time with loved ones—not worrying about finances. For many senior citizens in India, Fixed Deposits (FDs) have long been the bedrock of a safe and secure investment strategy. They offer guaranteed returns, capital preservation, and the peace of mind that comes with knowing your…

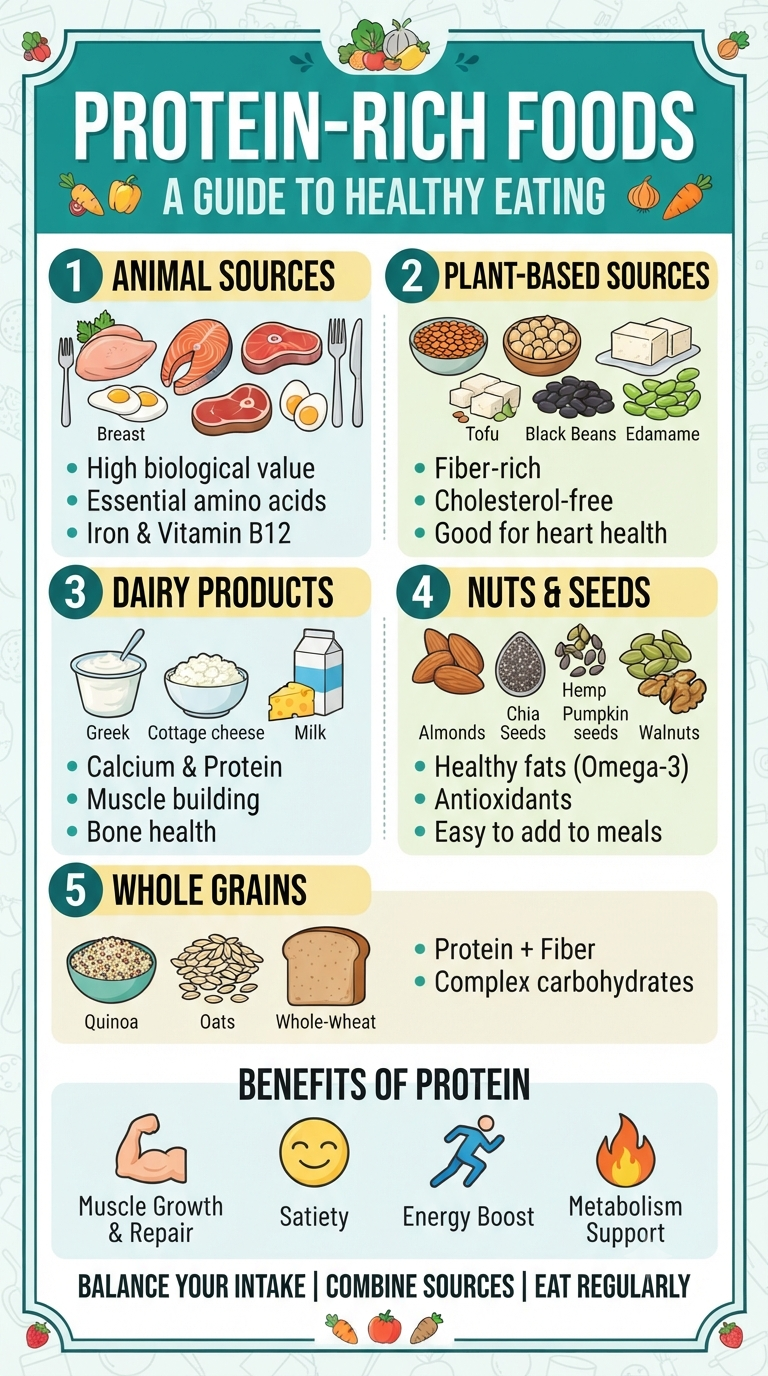

We often hear about the importance of protein, but do you know why it’s truly the MVP of your diet? Protein is the essential building block for our bodies—it’s responsible for everything from repairing muscles after a tough workout to keeping us feeling full and satisfied throughout a busy day. Whether you are looking to…

Continue Reading Power Up Your Plate: The Ultimate Guide to Protein-Rich Eating

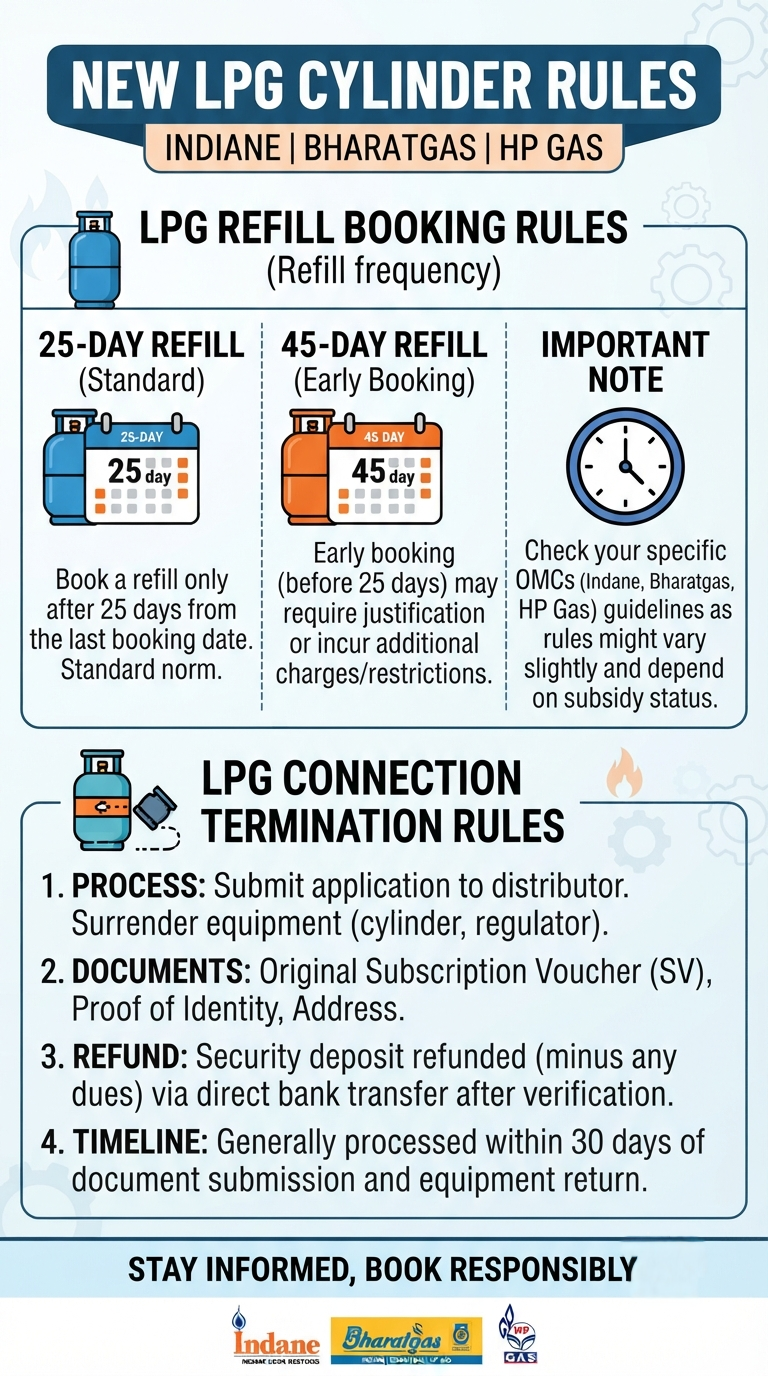

Are you finding the latest updates on LPG cylinder bookings and connections a bit confusing? Whether you use Indane, Bharat Gas, or HP Gas, staying on top of these guidelines is essential for a seamless kitchen experience. The government and oil marketing companies have introduced several changes over the past few months to streamline distribution.…

Continue Reading Everything You Need to Know About the New LPG Cylinder Rules

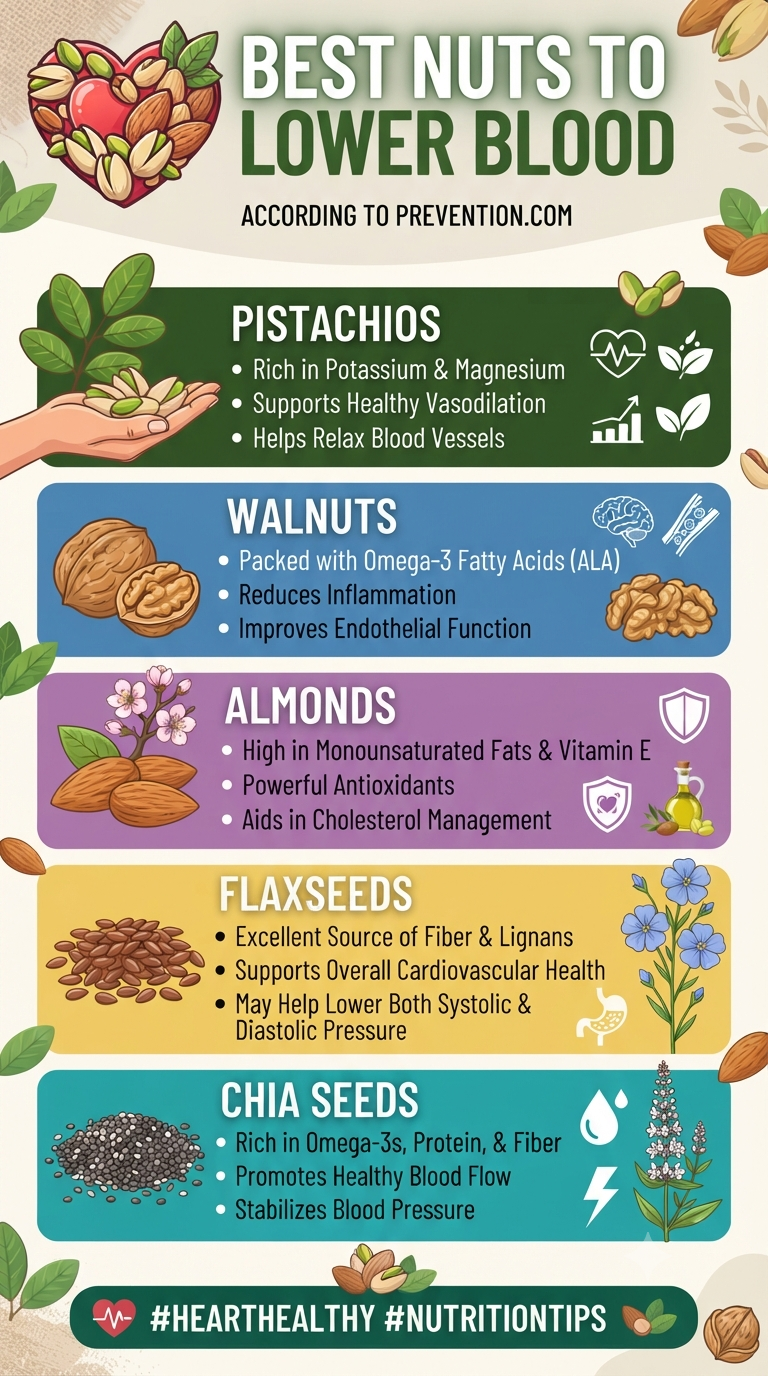

When it comes to maintaining a healthy heart, what you put on your plate matters—a lot. While we often think of major dietary overhauls to manage blood pressure, sometimes the most effective changes are the simplest ones. It turns out, reaching for a handful of nature’s smallest snacks might be one of the best things…

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.