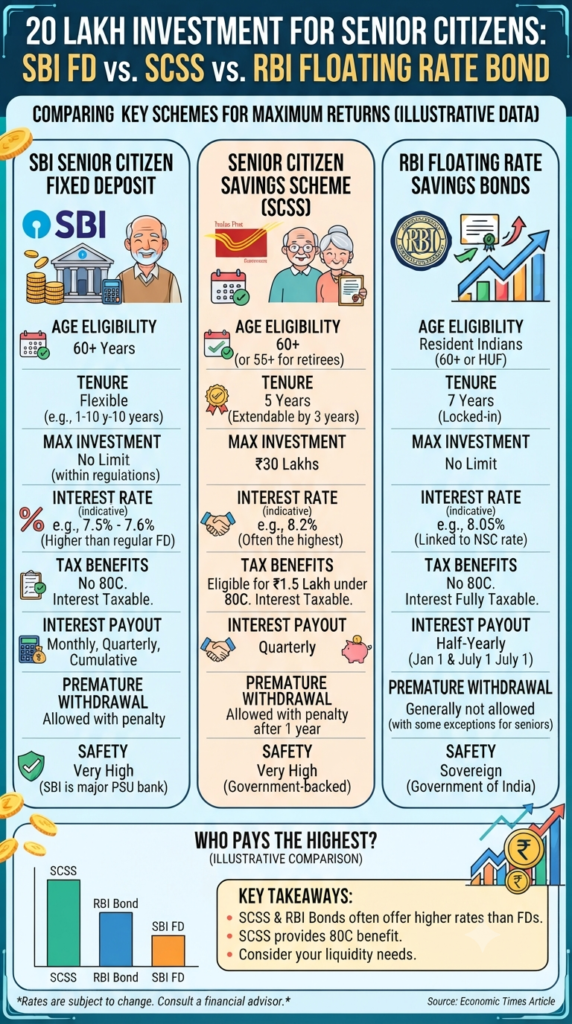

For many senior citizens, retirement isn’t just about ending a long career—it’s about transitioning into a lifestyle where every rupee works as hard as they once did. If you have a corpus of ₹20 lakh and are looking for a blend of stability and steady income, you’ve likely found yourself staring at three of the most popular options in India: SBI Senior Citizen Fixed Deposits (FDs), the Senior Citizens Savings Scheme (SCSS), and the RBI Floating Rate Savings Bonds.

But which one actually puts the most money in your pocket, and which one fits your specific needs? Let’s break it down.

The Contenders at a Glance

1. Senior Citizens Savings Scheme (SCSS)

The “gold standard” for many, the SCSS is government-backed and widely favored for its reliable quarterly payouts.

- The Yield: Currently offering approximately 8.2% per annum.

- The Math: Investing ₹20 lakh here could fetch you roughly ₹41,000 every quarter, translating to about ₹13,667 per month.

- The Edge: It offers the benefit of Section 80C tax deductions, making it a tax-efficient choice for many. However, do keep in mind there is a maximum investment cap of ₹30 lakh per person.

2. RBI Floating Rate Savings Bonds

If you are looking for a sovereign-backed, low-risk option and don’t mind a slightly longer commitment, these bonds are a compelling choice.

- The Yield: These currently offer around 8.05% per annum. Unlike the SCSS, the rate is linked to the National Savings Certificate (NSC) and is reset every six months.

- The Math: An investment of ₹20 lakh would generate an annual interest of ₹1.61 lakh. Because interest is paid half-yearly, you’d receive ₹80,500 every six months—roughly ₹13,417 per month.

- The Edge: There is no maximum investment limit, making it ideal if you have a larger corpus.

3. Bank Fixed Deposits (e.g., SBI)

The traditional favorite, FDs are the definition of “set it and forget it” for many retirees.

- The Yield: Rates fluctuate based on tenure, but for a 5-year senior citizen FD, current rates hover around 7.05%.

- The Math: With a 7.05% rate on ₹20 lakh, you would receive roughly ₹35,250 every quarter, or about ₹11,750 monthly.

- The Edge: FDs offer unmatched flexibility in payout options (monthly, quarterly, or cumulative) and are incredibly easy to manage through your existing bank account.

The Verdict: How to Choose?

When deciding where to park your ₹20 lakh, consider these three pillars:

- Your Tax Strategy: If you still have room under your Section 80C limit, the SCSS provides a double-win of decent returns and tax savings.

- Your Liquidity Needs: FDs often provide the most flexibility if you think you might need to withdraw funds early (though penalties may apply). Meanwhile, RBI Bonds have a 7-year lock-in period, though they do offer specific early exit options for seniors.

- Your Risk Appetite: If safety is your absolute priority, remember that both the SCSS and RBI Bonds carry the backing of the Government of India, offering sovereign safety.

Final Thought: There is no “one size fits all” in retirement planning. Many savvy investors choose to diversify their ₹20 lakh across these instruments—keeping some in an accessible FD for emergencies, and the rest in SCSS or RBI Bonds to lock in higher interest rates.

Disclaimer: Interest rates and tax rules are subject to change. Always consult with a financial advisor to tailor these options to your personal tax bracket and long-term goals.

Good News for Central Government Employees: July 2026 DA Hike Expectations Soar!

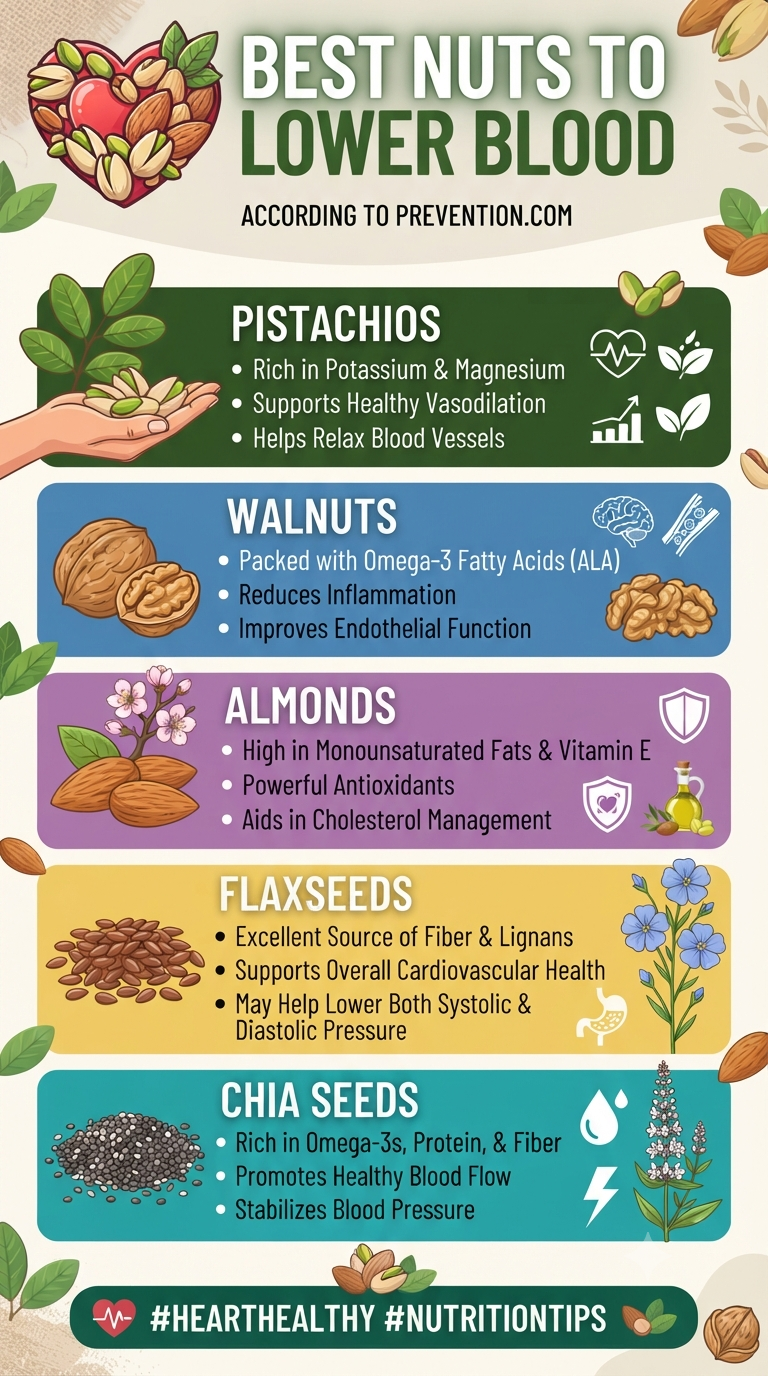

When it comes to maintaining a healthy heart, what you put on your plate matters—a lot. While we often think of major dietary overhauls to manage blood pressure, sometimes the most effective changes are the simplest ones. It turns out, reaching for a handful of nature’s smallest snacks might be one of the best things…

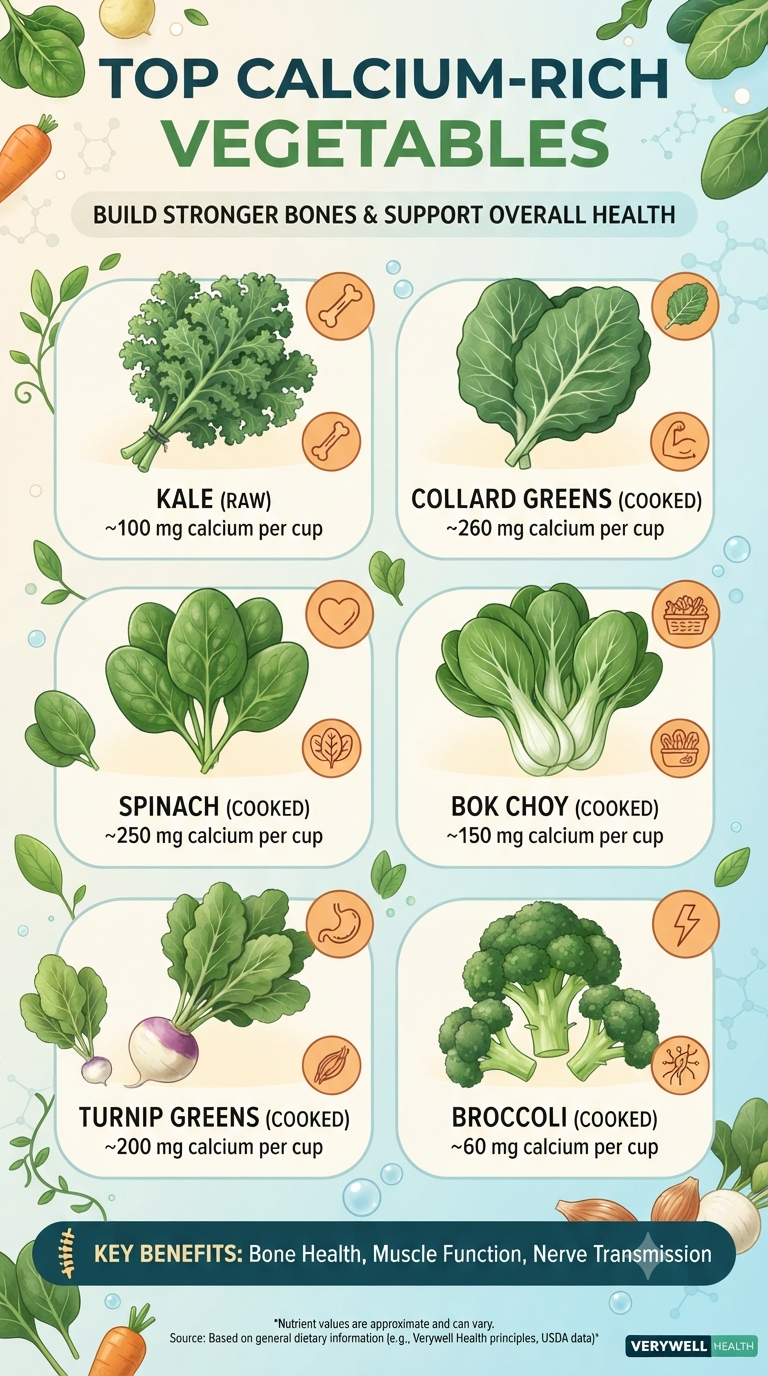

When we think of calcium, our minds often jump straight to a tall, frosty glass of milk or a wedge of cheddar. It’s the classic advice we’ve been given since childhood. But what if you aren’t a fan of dairy, or your body simply doesn’t agree with it? The good news is that you don’t…

Continue Reading Beyond Dairy: The Green Way to Stronger Bones

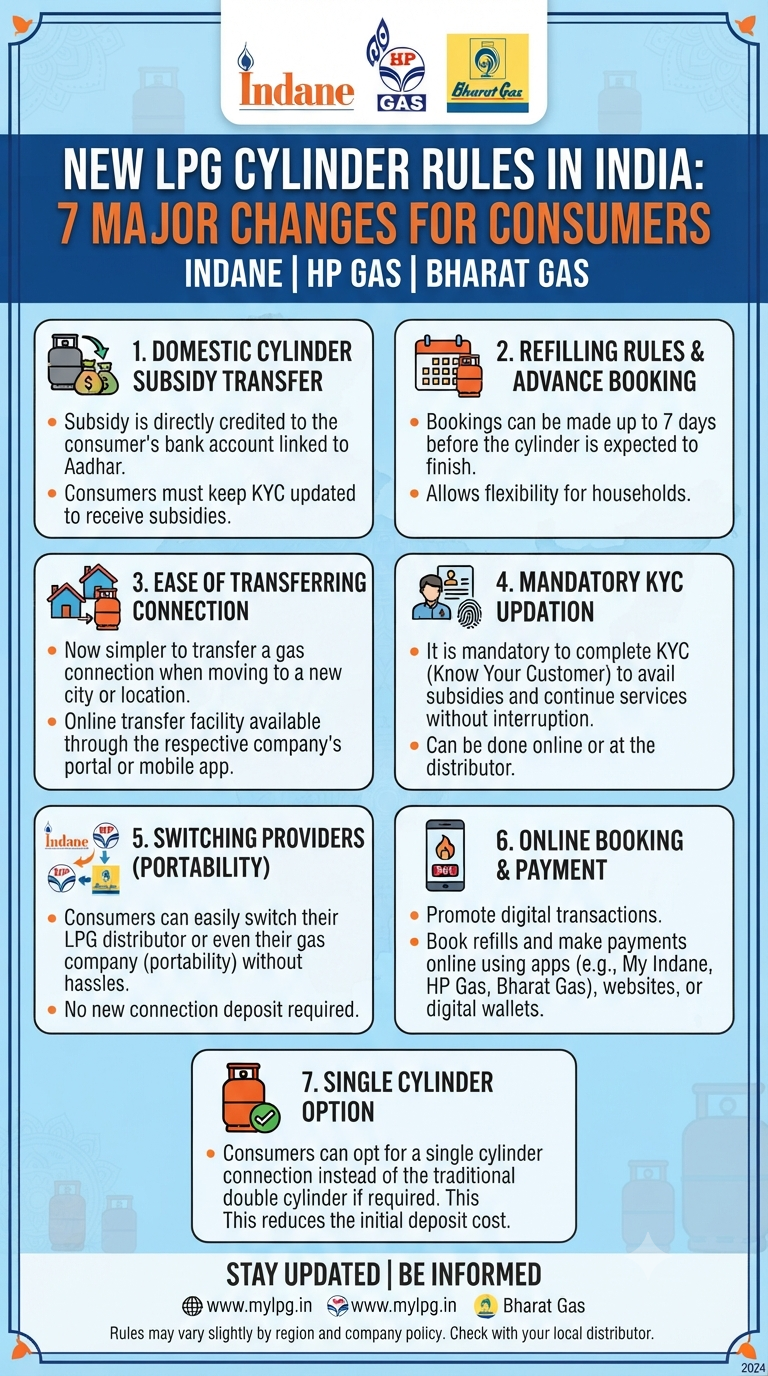

If you are a household consumer in India using Indane, HP Gas, or Bharat Gas, keeping up with changing policies can sometimes feel like a chore. However, staying informed is the best way to ensure you never face a disruption in your cooking gas supply or miss out on your hard-earned subsidies. Recent updates to…

Continue Reading New LPG Rules Simplified: 7 Major Changes You Need to Know

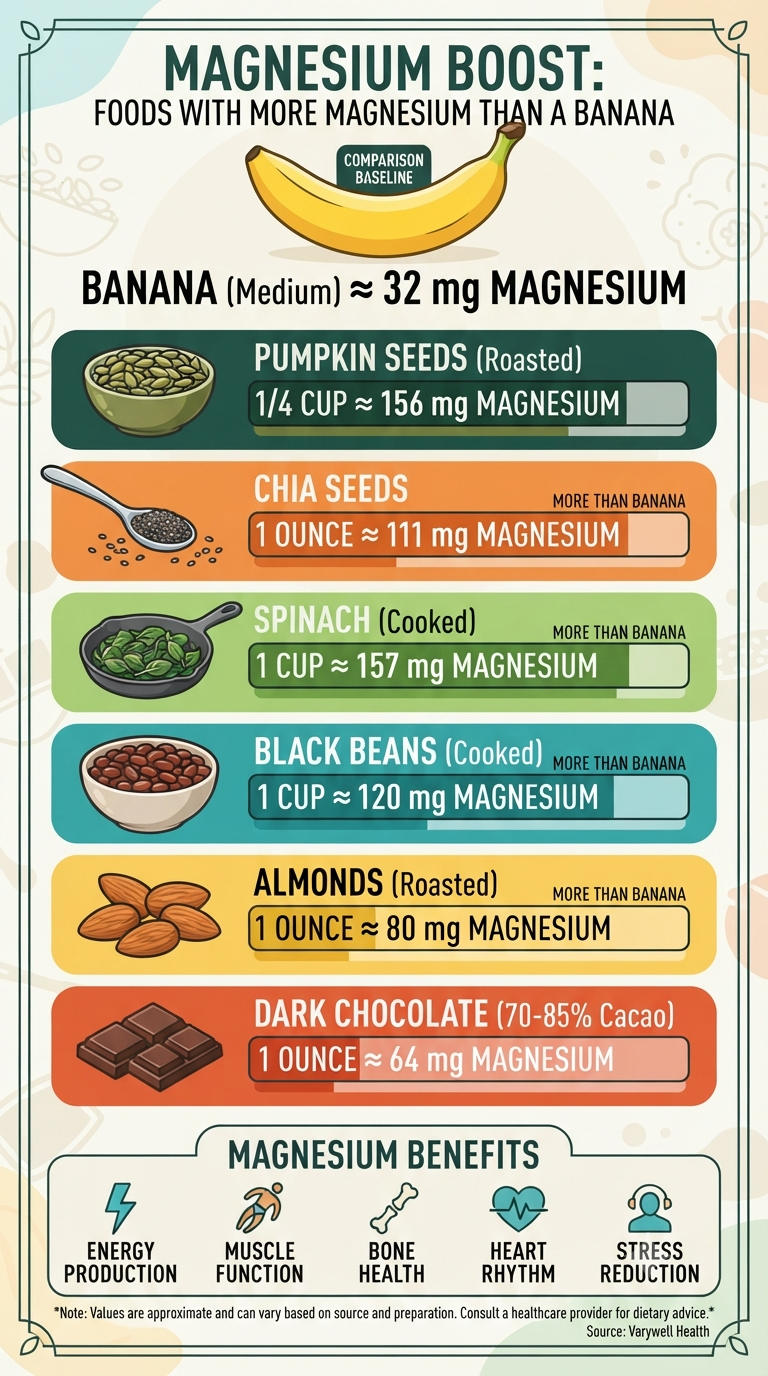

When we think of magnesium-rich foods, the humble banana often takes center stage. It’s convenient, affordable, and—let’s be honest—it’s been marketed as the go-to fruit for potassium and magnesium for decades. But did you know that your banana might actually be underperforming when it comes to your daily magnesium needs? Magnesium is an unsung hero…

Continue Reading Move Over, Banana: The Surprising Foods That Pack More Magnesium

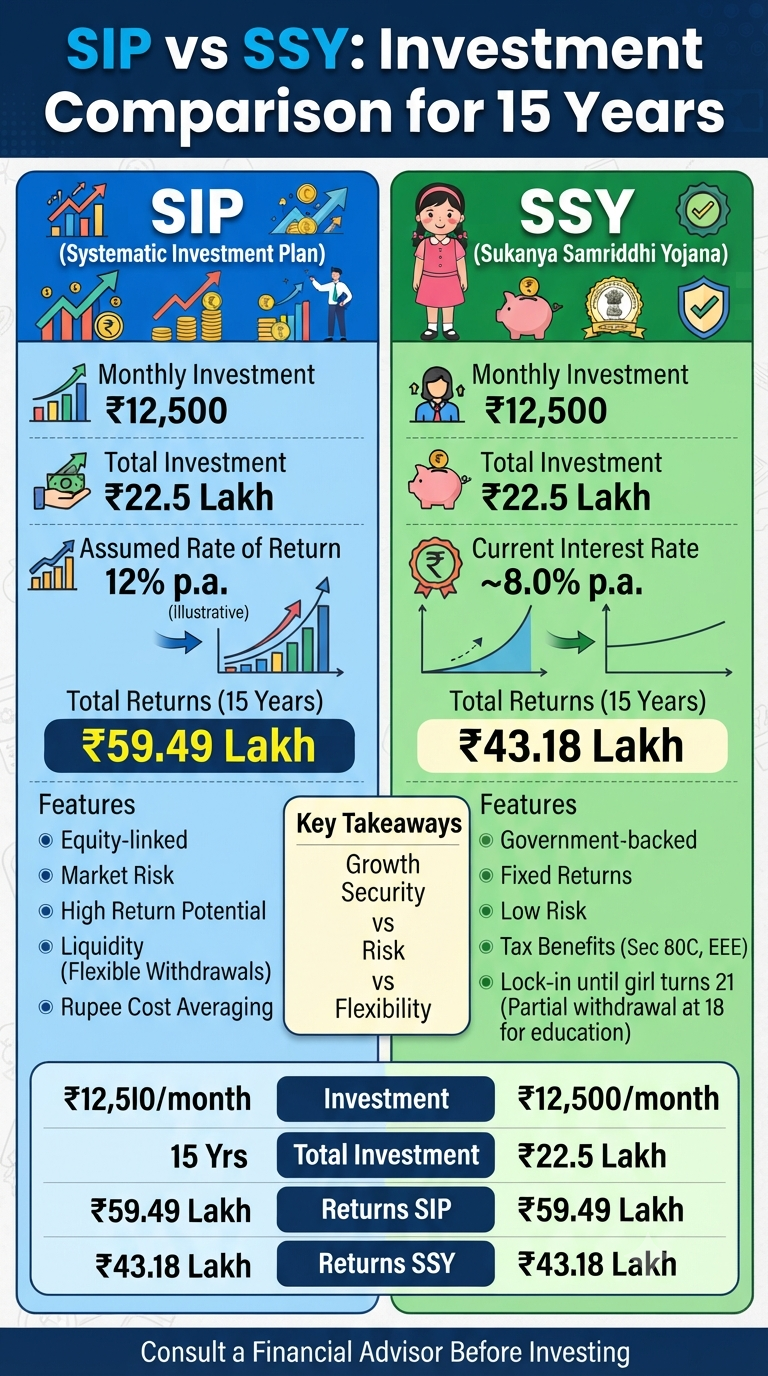

Investing for the future is crucial, and choosing the right investment avenue can make a significant difference in achieving your financial goals. Two popular options in India are the Systematic Investment Plan (SIP) and the Sukanya Samriddhi Yojana (SSY). Let’s delve into a detailed comparison to help you make an informed decision. SIP: Equity-linked and…

Continue Reading SIP vs. SSY: A Detailed Comparison for a Secure Financial Future

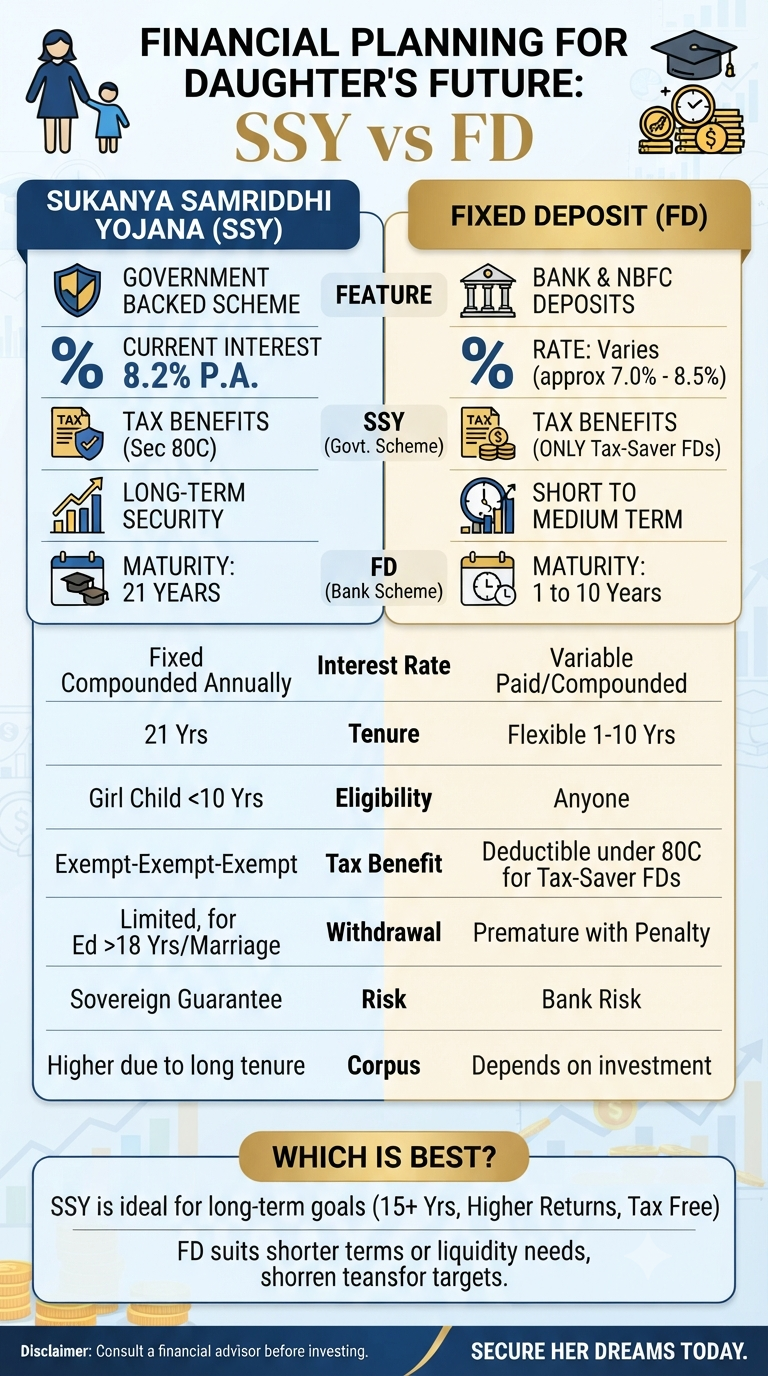

As parents, we are constantly looking ahead. We dream of our daughter’s college graduation, her first steps into a career, and perhaps her wedding day. But dreams, while priceless, require pragmatic financial planning to become reality. When it comes to securing a financial corpus for a girl child in India, two names inevitably pop up…

Continue Reading Secure Her Dreams: Decystifying the SSY vs. FD Battle for Your Daughter’s Future

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.