If you’ve been active in the stock market lately, you know the feeling all too well: the adrenaline of a high-stakes trade, followed by the sting of a red closing screen. Whether it was a volatile F&O swing, a mistimed intraday gamble, or a long-term delivery position that didn’t pan out, market losses are a bitter pill to swallow.

But here is the silver lining that many investors miss: Your trading losses aren’t just a blow to your portfolio—they can be a powerful tool for your tax planning.

If you are treating your losses as a dead end, you are likely leaving thousands of rupees on the table. Here is how you can leverage your ITR-3 to claim the maximum tax benefits legally and efficiently.

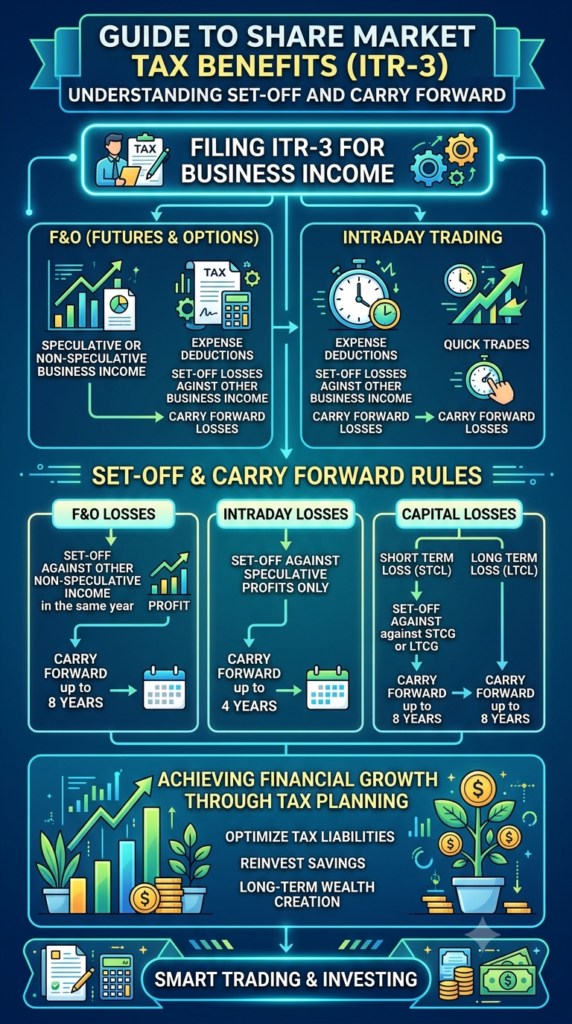

1. Stop Using the Wrong Form (The ITR-3 Advantage)

One of the most common mistakes traders make is filing the wrong ITR form. If you are an individual or HUF engaged in F&O or intraday trading, ITR-3 is your best friend.

Why? Because your trading activity is legally classified as “Profits and Gains of Business or Profession.” Trying to squeeze these into a simplified ITR-4 (presumptive taxation) is a risky move, especially when you are nursing losses. Using the wrong form can block you from reporting those losses correctly, effectively throwing away your future tax relief.

2. Know Your “Loss Personality”

The Income Tax Act doesn’t view all losses equally. Understanding the nature of your trade is the secret to set-off:

- F&O Losses (Non-speculative): These are flexible. You can set them off against your other business income (and even other heads of income, excluding salary) and carry them forward for up to 8 years.

- Intraday Losses (Speculative): These are restricted. They can only be set off against speculative business profit and carried forward for 4 years.

- Delivery Losses (Capital Gains): These follow the rules of STCL (Short-Term Capital Loss) or LTCL (Long-Term Capital Loss), which have their own specific set-off rules against capital gains.

Pro-Tip: Never mix your “investment” ledger with your “trading” ledger. If you treat delivery shares as capital assets sometimes and stock-in-trade other times, the tax authorities will spot the inconsistency. Pick a lane and stay consistent.

3. The “Due Date” Deadline: The Golden Rule

This is the most critical point: If you miss the ITR filing deadline, you lose the right to carry forward your losses.

Even if your income is below the taxable limit, if you want to carry forward your losses to offset future profits, you must file your return within the due date under Section 139(1). A late-filed return is a lost opportunity to save tax for the next 8 years. Treat your tax filing date with the same urgency you treat a margin call.

4. Is an Audit Looming?

A common myth is that having a loss triggers a tax audit. Not necessarily.

A tax audit is usually triggered by your turnover, not your profit/loss. Remember, for F&O and intraday, your turnover isn’t the total contract value—it’s the sum of the absolute differences (absolute profit + absolute loss). Only when you cross specific turnover thresholds (generally ₹1 crore, or ₹10 crore if you meet the 5% digital transaction criteria) does the audit requirement kick in.

The Bottom Line

Trading is a business. Like any business, you need to keep impeccable records of your broker statements, exchange charges, and even the portion of your internet bill used for trading.

Don’t let a bad trading year define your financial future. By filing correctly, classifying your transactions accurately, and staying within the legal deadlines, you can transform this year’s “red” into next year’s “tax-free” cushion.

Disclaimer: Tax laws are intricate and highly dependent on your personal financial facts. This article is for informational purposes and should not be considered professional tax advice. Always consult with a qualified Chartered Accountant to align your filing strategy with your specific situation.

Navigating the New Normal: 5 Key Updates to the Senior Citizen Savings Scheme (SCSS) from July 2026

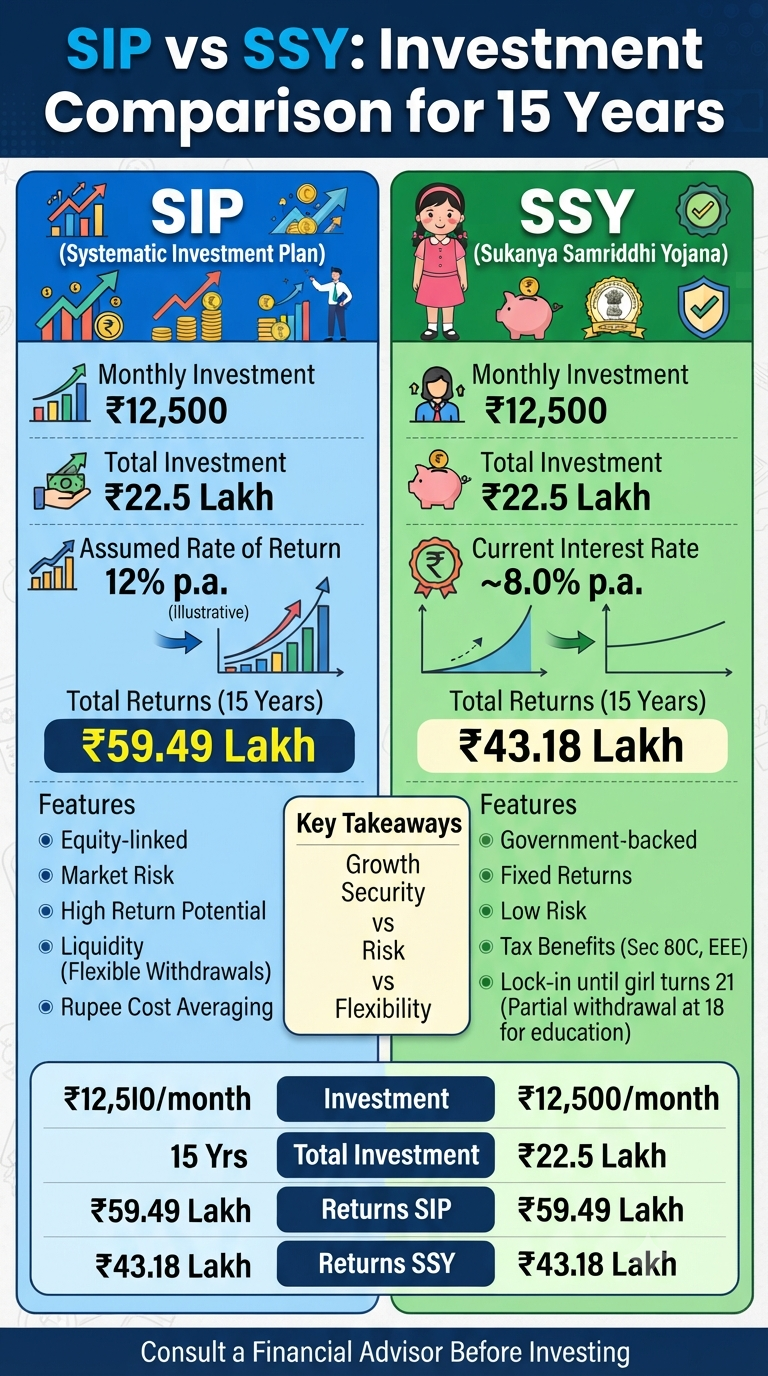

Investing for the future is crucial, and choosing the right investment avenue can make a significant difference in achieving your financial goals. Two popular options in India are the Systematic Investment Plan (SIP) and the Sukanya Samriddhi Yojana (SSY). Let’s delve into a detailed comparison to help you make an informed decision. SIP: Equity-linked and…

Continue Reading SIP vs. SSY: A Detailed Comparison for a Secure Financial Future

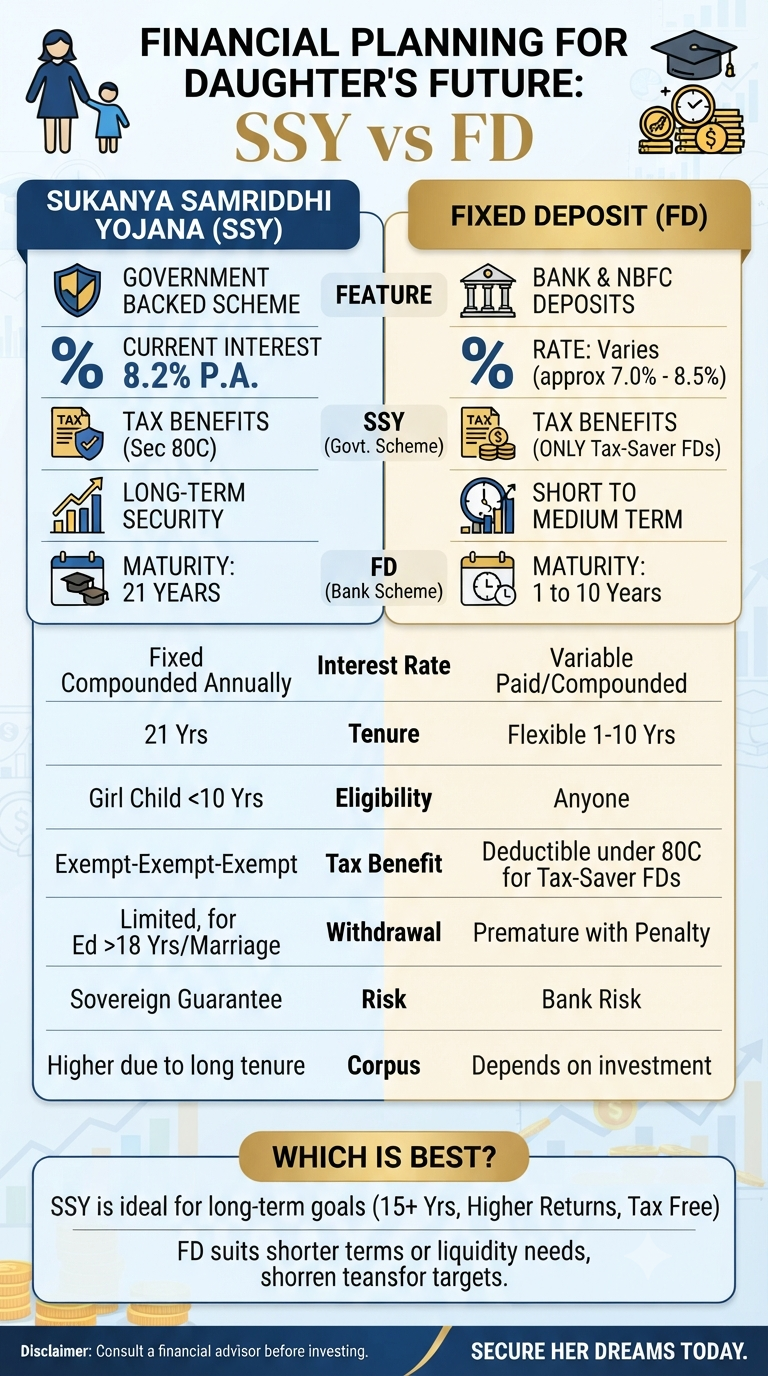

As parents, we are constantly looking ahead. We dream of our daughter’s college graduation, her first steps into a career, and perhaps her wedding day. But dreams, while priceless, require pragmatic financial planning to become reality. When it comes to securing a financial corpus for a girl child in India, two names inevitably pop up…

Continue Reading Secure Her Dreams: Decystifying the SSY vs. FD Battle for Your Daughter’s Future

We’ve all been there—staring at the bank balance, feeling the familiar squeeze of anxiety, and wondering when things will finally get easier. Often, we treat money problems purely as a logistical issue: we need more income, less debt, or a better budget. But what if the key to financial freedom isn’t just found in a…

Continue Reading From Scarcity to Abundance: 5 Daily Rituals to Unlock True Financial Prosperity

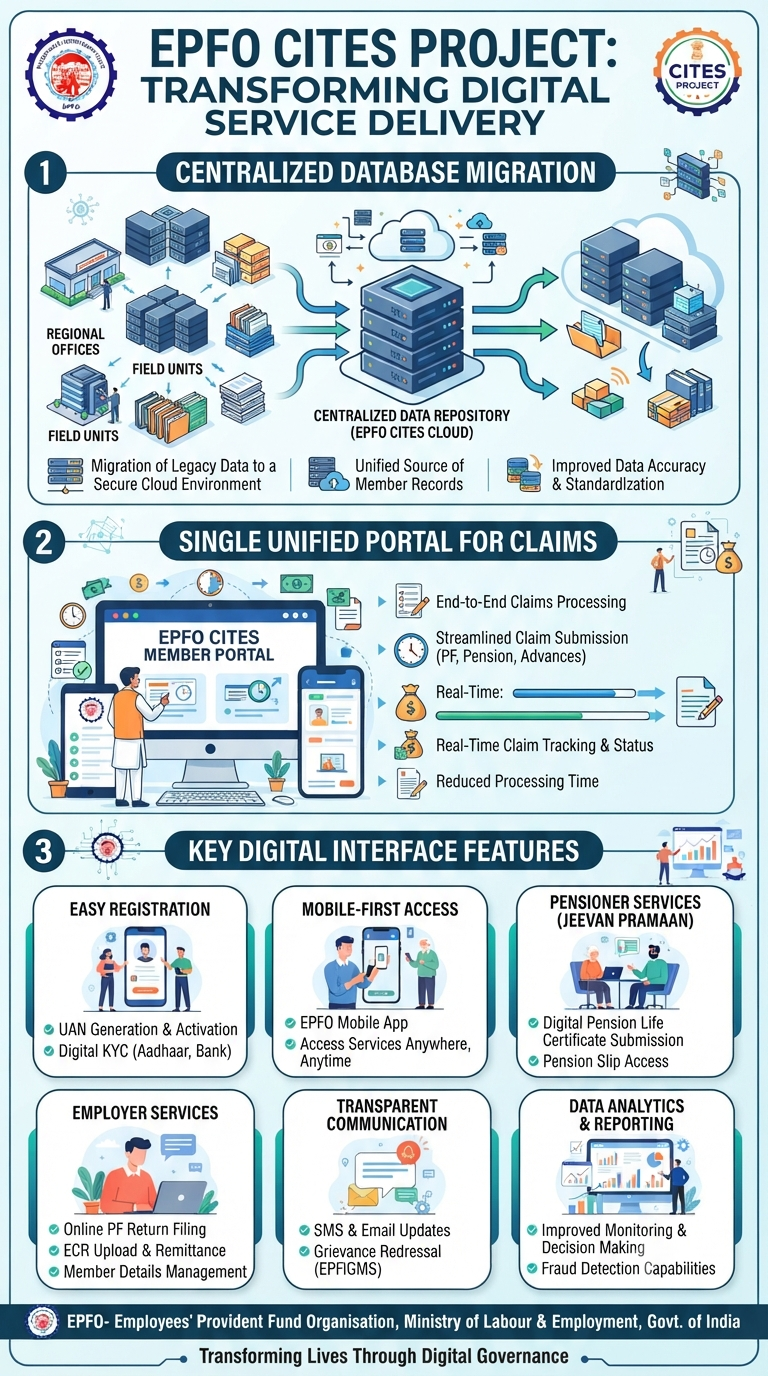

For decades, interacting with the Employees’ Provident Fund Organisation (EPFO) often felt like stepping back in time. Between the mountain of physical paperwork, the anxiety of waiting for transfer approvals, and the occasional need to visit regional offices just to check a status update, the system was ripe for a modern evolution. Well, that evolution…

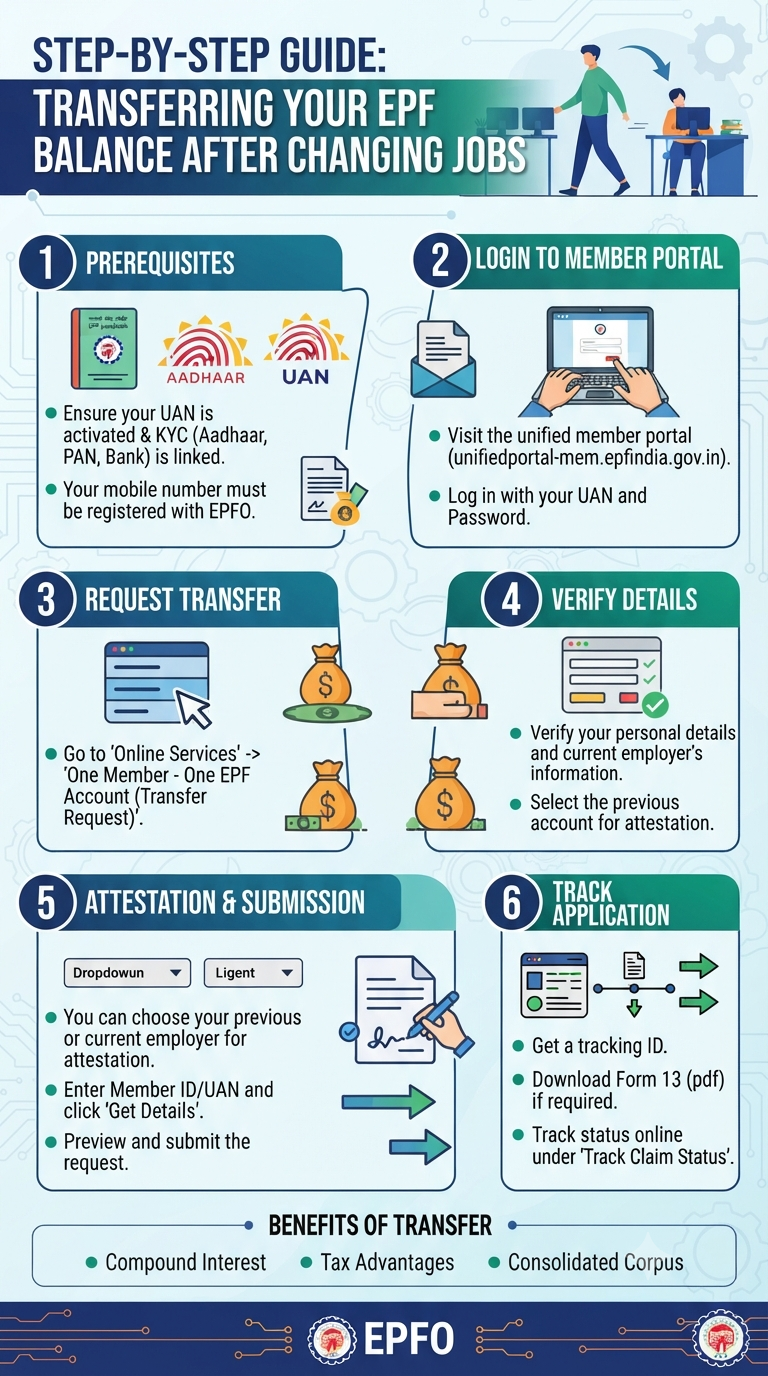

Switching jobs is an exciting milestone, but it often brings a laundry list of administrative tasks. One of the most important, yet frequently overlooked, responsibilities is managing your Employees’ Provident Fund (EPF). Leaving your old PF account dormant can cause complications down the line. The good news? The EPFO has revamped its member portal to…

Continue Reading New Job? Here’s How to Seamlessly Transfer Your EPF Balance

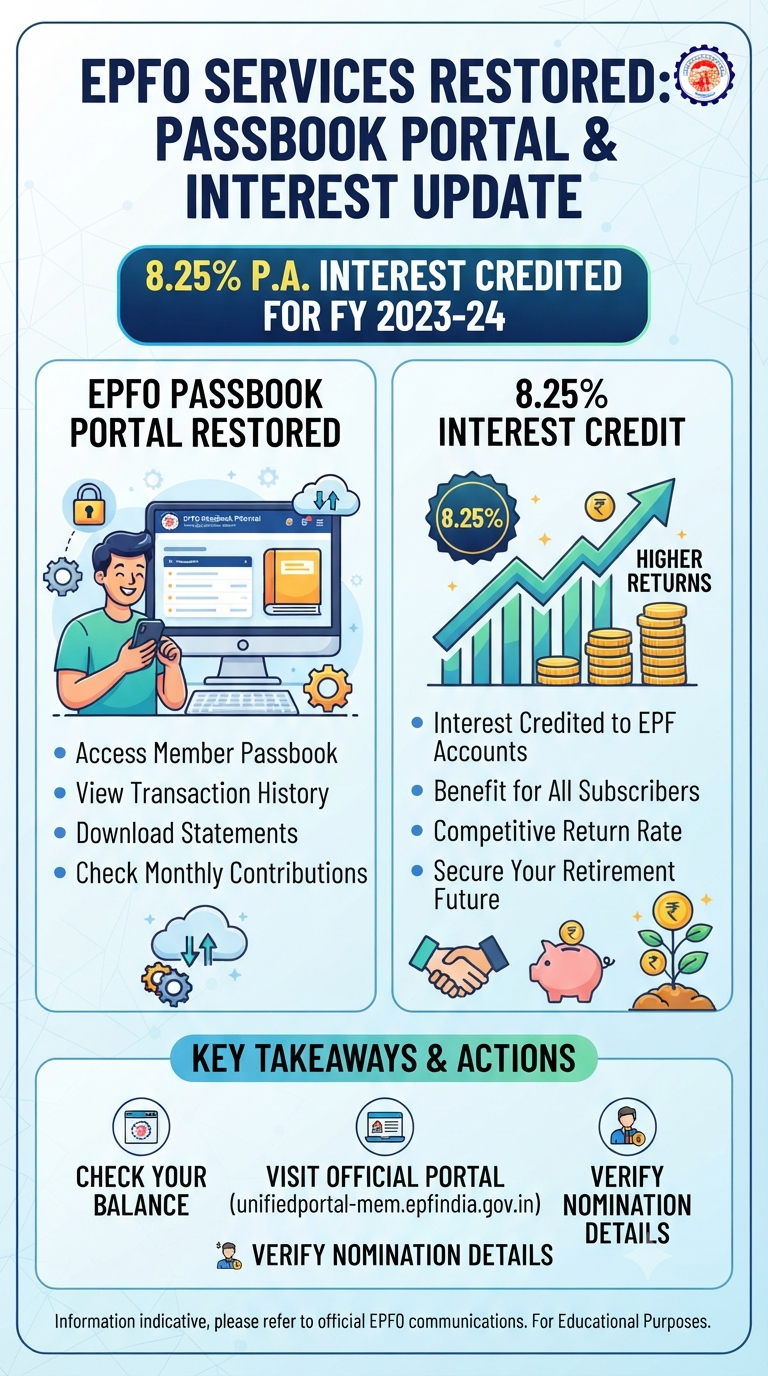

For millions of employees across India, the Employees’ Provident Fund (EPF) is more than just a mandatory deduction—it’s the bedrock of a secure retirement. So, when the EPFO passbook portal goes down for maintenance, it’s understandable that anxiety levels spike. After all, your passbook is the window into your financial future. The good news? The…

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.