If you’re the kind of person who treats your bank fixed deposit (FD) like a “set it and forget it” tool, I have a question for you: When was the last time you actually checked the interest rate?

For many of us, FDs are the ultimate safe harbor. We put our hard-earned money into our trusted, big-name bank, watch the tenure tick by, and feel content. But in the current financial landscape of July 2026, staying with the status quo might be quietly costing you money.

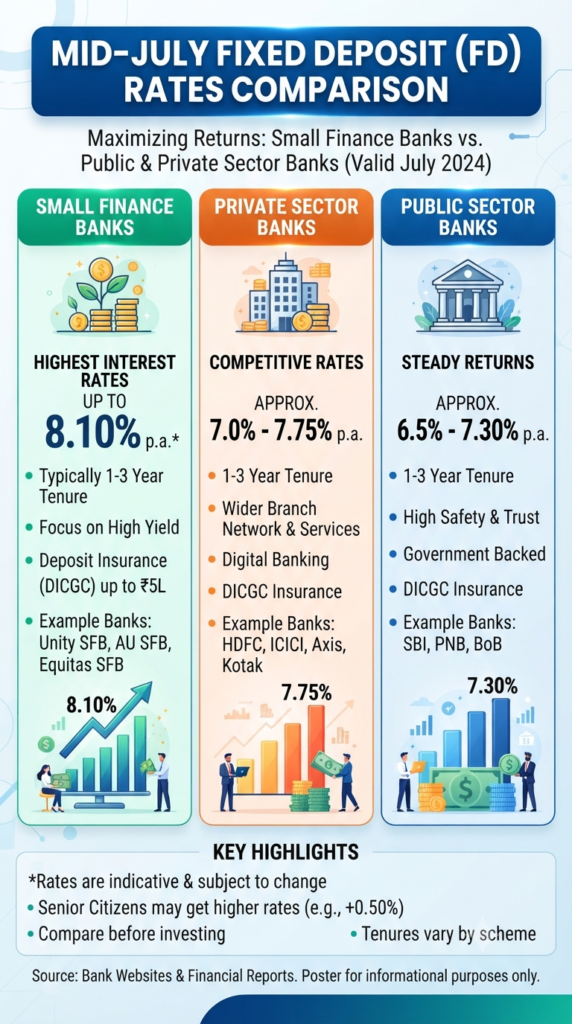

The latest data shows a fascinating divide in the banking world. While major public and private sector banks continue to be the pillars of stability, a different breed of lender is currently holding the crown for the best returns: Small Finance Banks (SFBs).

The Rate Gap: What the Numbers Say

Right now, if you are looking at the major public sector giants, you’re likely seeing rates hovering in the 6.45% to 6.75% range. Private sector banks are putting up a stronger fight, typically landing between 7.0% and 7.5%.

However, if you look toward Small Finance Banks, the story changes. We are seeing rates reaching up to 8.1% for regular depositors.

Think about the math for a second. That gap—often more than a full percentage point—might seem small on paper, but over a two- or three-year tenure, it adds up to a significant difference in your maturity proceeds.

Why Small Finance Banks Are So Competitive

You might be wondering, “If they are ‘small,’ are they safe?”

It’s a valid concern. Small Finance Banks are niche institutions designed to reach underserved sectors, but they are fully regulated by the Reserve Bank of India (RBI). Just like the “big guys,” deposits in these banks are covered by the DICGC (Deposit Insurance and Credit Guarantee Corporation) insurance, which protects your principal and interest up to ₹5 lakh per bank.

They offer these higher rates because they are hungry for deposits to grow their loan books. They aren’t trying to out-advertise the massive brands; they are trying to out-value them.

Your “Action Plan” for July 2026

Before you rush to open a new account, here is how you should think about your next move:

- Don’t Just Chase the Headline Rate: An 8.1% return is fantastic, but it’s not the only factor. Consider the tenure that suits your goals. Is your money truly free to be locked away for 666 days, or do you need liquidity sooner?

- Use the “Insurance” Rule: If you have a large sum to invest, consider splitting it across a few different institutions. By keeping your deposits within the ₹5 lakh limit per bank, you maximize the protection offered by DICGC.

- Check the Fine Print: Often, the highest advertised rates are for specific “special” tenures. Always check if that specific tenure aligns with when you actually need the money back.

- Consider the “Big Picture”: If you value the convenience of having your salary account, credit card, and home loan all in one place, a big private or public sector bank might still be your best fit. But for your extra savings—the money earmarked for growth—the specialized lenders are currently unbeatable.

The Bottom Line

The financial market is highly competitive right now, and that’s great news for you. You don’t have to settle for the default option. Take ten minutes this weekend to look at the rate charts, compare the institutions, and make sure your money is working as hard as you worked to earn it.

After all, your savings shouldn’t be sleeping—they should be growing.

Disclaimer: Interest rates are indicative and subject to change based on bank policies. Always verify the latest rates on the official bank websites before investing. This article is for informational purposes and does not constitute formal financial advice.

Magnesium vs. Melatonin: Which One Actually Wins the Battle for Better Sleep?

For millions of employees across India, the Employees’ Provident Fund (EPF) is more than just a mandatory deduction—it’s the bedrock of a secure retirement. So, when the EPFO passbook portal goes down for maintenance, it’s understandable that anxiety levels spike. After all, your passbook is the window into your financial future. The good news? The…

Filing your Income Tax Return (ITR) is one of those annual financial chores that often feels daunting. We scramble for Form 16s, look for investment proofs, and hope we haven’t missed anything. But what if there was a “cheat sheet” that held nearly all the information the Income Tax Department already has about your financial…

Continue Reading Why Your Annual Information Statement (AIS) is Your Best Friend Before Filing ITR

Retirement often feels like a distant milestone—something to worry about “later.” But what if you could visualize that “later” right now? Imagine hitting age 60 with a solid ₹3 crore corpus. It’s not just a number on a screen; it’s the key to your financial independence, the bridge to your passions, and the ultimate safety…

Continue Reading Retire Rich: How a ₹3 Crore Corpus Can Power Your Dream Life

You’ve done your homework. You’ve read the financial news, listened to the podcasts, and decided it’s time to secure your financial future. To build a robust, resilient portfolio, you adopt a “more is merrier” strategy, buying into several different mutual funds to ensure you are diversified. But here is a hard truth that many investors…

Continue Reading The Illusion of Choice: Are You Trapped in the Mutual Fund Overlap Web?

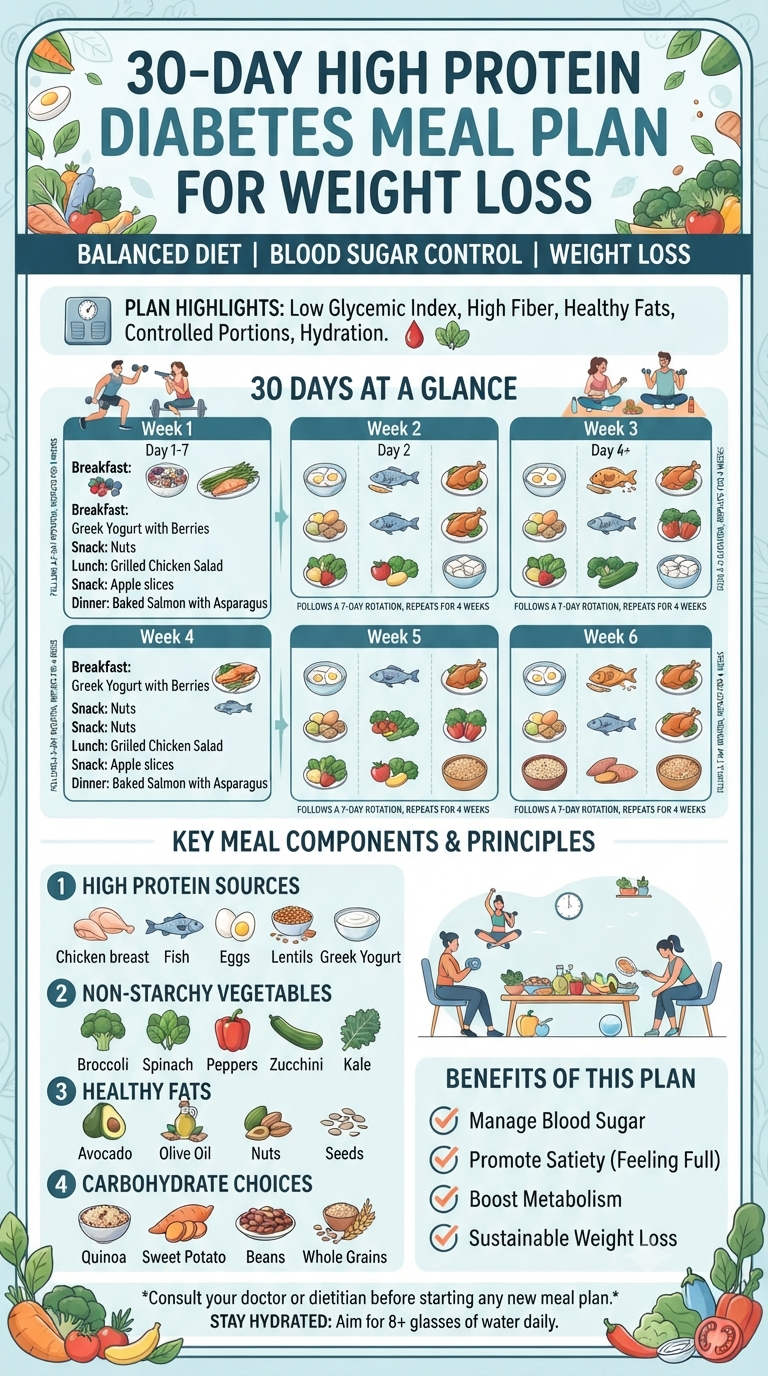

When it comes to health, we’re often bombarded with quick fixes and extreme restrictions. But what if the secret to managing blood sugar and achieving weight loss wasn’t about deprivation, but about intentional, high-protein nourishment? If you’ve been looking for a way to reset your habits without feeling constantly hungry, a high-protein, diabetes-friendly approach might…

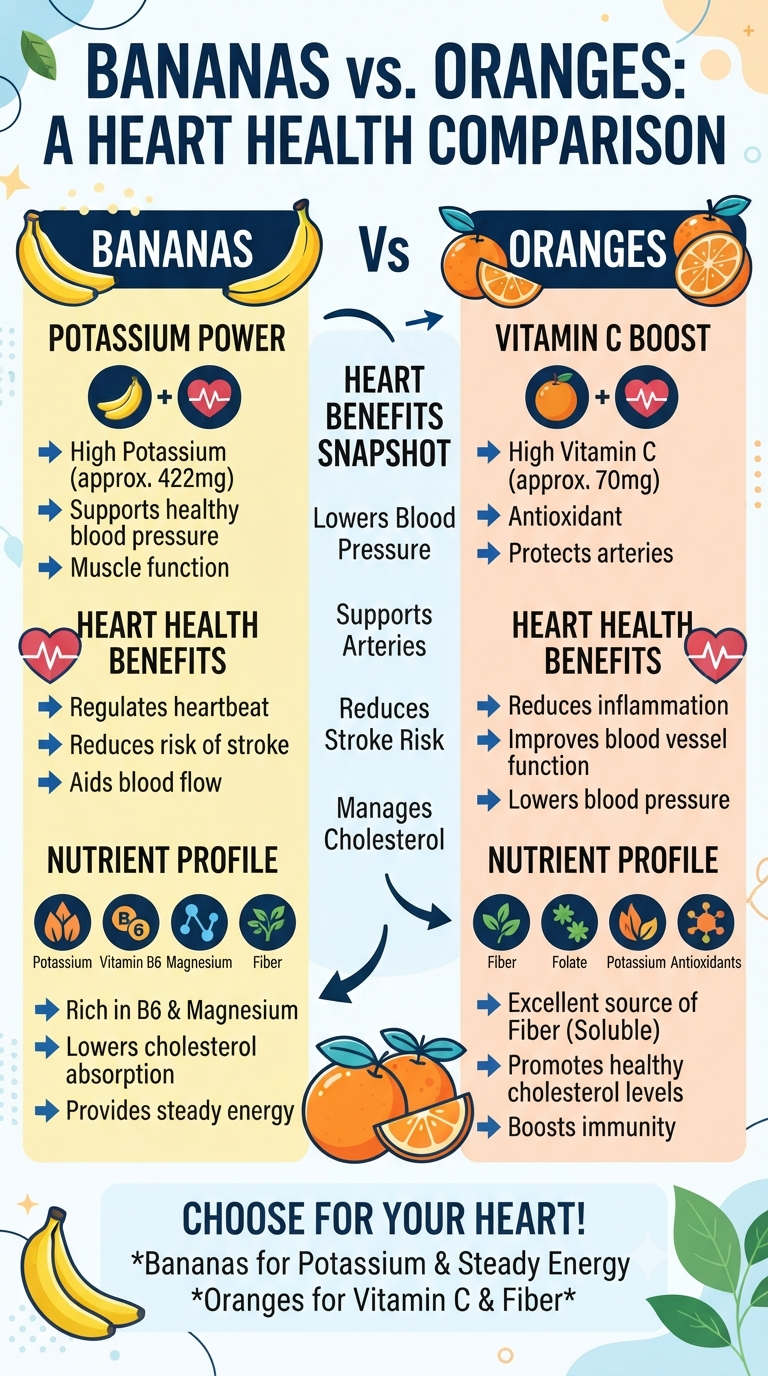

When you’re staring at the fruit bowl wondering which snack will do your heart the most good, it’s easy to feel torn. Do you reach for the convenient banana or the zesty, refreshing orange? Both are nutritional powerhouses, but they bring different strengths to your cardiovascular game. Let’s break down how these two favorites measure…

Continue Reading Heart-Healthy Snacking: The Battle of the Fruits

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.