For many senior citizens, Fixed Deposits (FDs) aren’t just a financial instrument—they are the bedrock of peace of mind. When you’ve worked hard all your life, you want your savings to work just as hard for you, safely and predictably.

But with so many options, how do you decide where to park your hard-earned money? Today, we are breaking down a comparison between two financial giants—State Bank of India (SBI) and HDFC Bank—specifically looking at how they perform for senior citizens on investments of ₹10 lakh, ₹20 lakh, and ₹30 lakh.

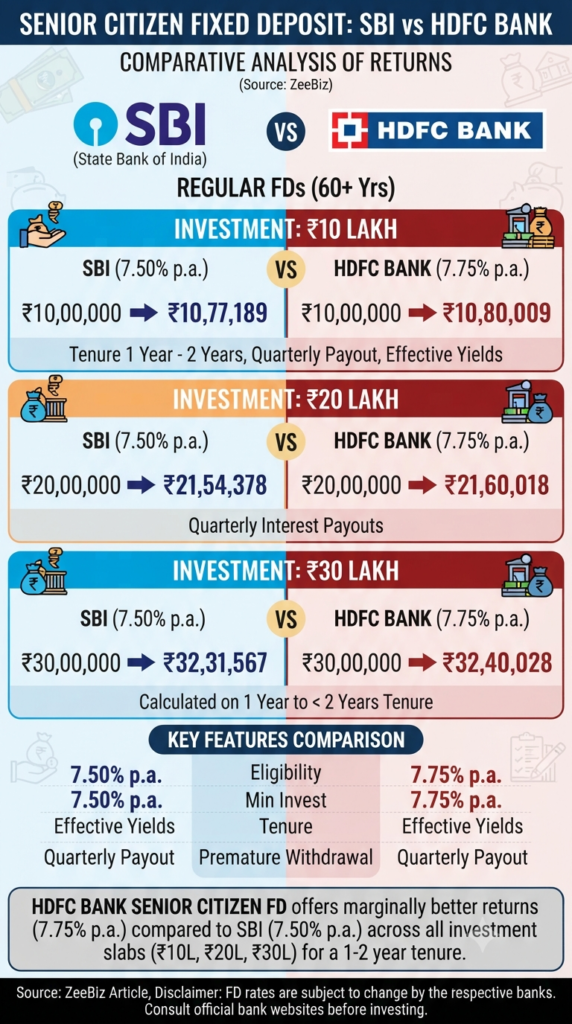

The Numbers Game: How They Compare

If you are looking at a tenure of 1 year to less than 2 years with quarterly interest payouts, the interest rates tell an interesting story.

Currently, HDFC Bank offers an interest rate of 7.75% per annum for senior citizens, while SBI offers 7.50% per annum for the same category. While a 0.25% difference might seem small, it can certainly add up depending on your investment amount.

Here is how your investment could potentially grow across different slabs:

| Investment Amount | SBI Return (7.50% p.a.) | HDFC Bank Return (7.75% p.a.) |

| ₹10 Lakh | ₹10,77,189 | ₹10,80,009 |

| ₹20 Lakh | ₹21,54,378 | ₹21,60,018 |

| ₹30 Lakh | ₹32,31,567 | ₹32,40,028 |

Key Takeaways for Your Financial Planning

- Higher Returns: Based on the current interest rates for a 1-2 year tenure, HDFC Bank offers marginally better returns compared to SBI across all investment slabs.

- Safety and Tenure: Both institutions are major players in the Indian banking sector. The calculations provided are based on a tenure of 1 year to less than 2 years.

- Flexibility: Both banks provide options for quarterly interest payouts, which can be a great way to manage regular cash flow for your daily expenses.

A Note Before You Decide

While the numbers give us a clear direction, remember that FD rates are subject to change based on the policies of the respective banks. Before you finalize your decision, it is always a wise move to visit the official websites of both banks or speak with your bank branch manager to get the most updated rates and terms.

Ultimately, the “better” bank is the one that fits your personal financial goals, comfort level, and banking preferences. Happy investing!

Disclaimer: This article is for informational purposes only. Fixed deposit interest rates are subject to change. Please consult with the respective banks or a financial advisor before making any investment decisions.

Save Smartly: A July 2026 Guide to Recurring Deposit Interest Rates

When you’re staring at the fruit bowl wondering which snack will do your heart the most good, it’s easy to feel torn. Do you reach for the convenient banana or the zesty, refreshing orange? Both are nutritional powerhouses, but they bring different strengths to your cardiovascular game. Let’s break down how these two favorites measure…

Continue Reading Heart-Healthy Snacking: The Battle of the Fruits

Buying a home is one of life’s biggest milestones. For most people, it’s not just a house—it’s a long-term investment in their future and a place to build a life. But with such a massive price tag, a fundamental question arises: Should I save up and pay cash, or should I take out a home…

Continue Reading The Ultimate Showdown: Is it Better to Buy Your Dream Home with Cash or a Mortgage?

Let’s be honest: tracking down old Provident Fund (PF) accounts from past jobs feels like a chore no one wants to tackle. Between the mountain of forms, the fear of losing service history, and the sheer time it takes, many of us just leave our old accounts sitting idle. But what if you could clean…

Continue Reading Say Goodbye to Paperwork: How to Consolidate Your EPF Accounts Online

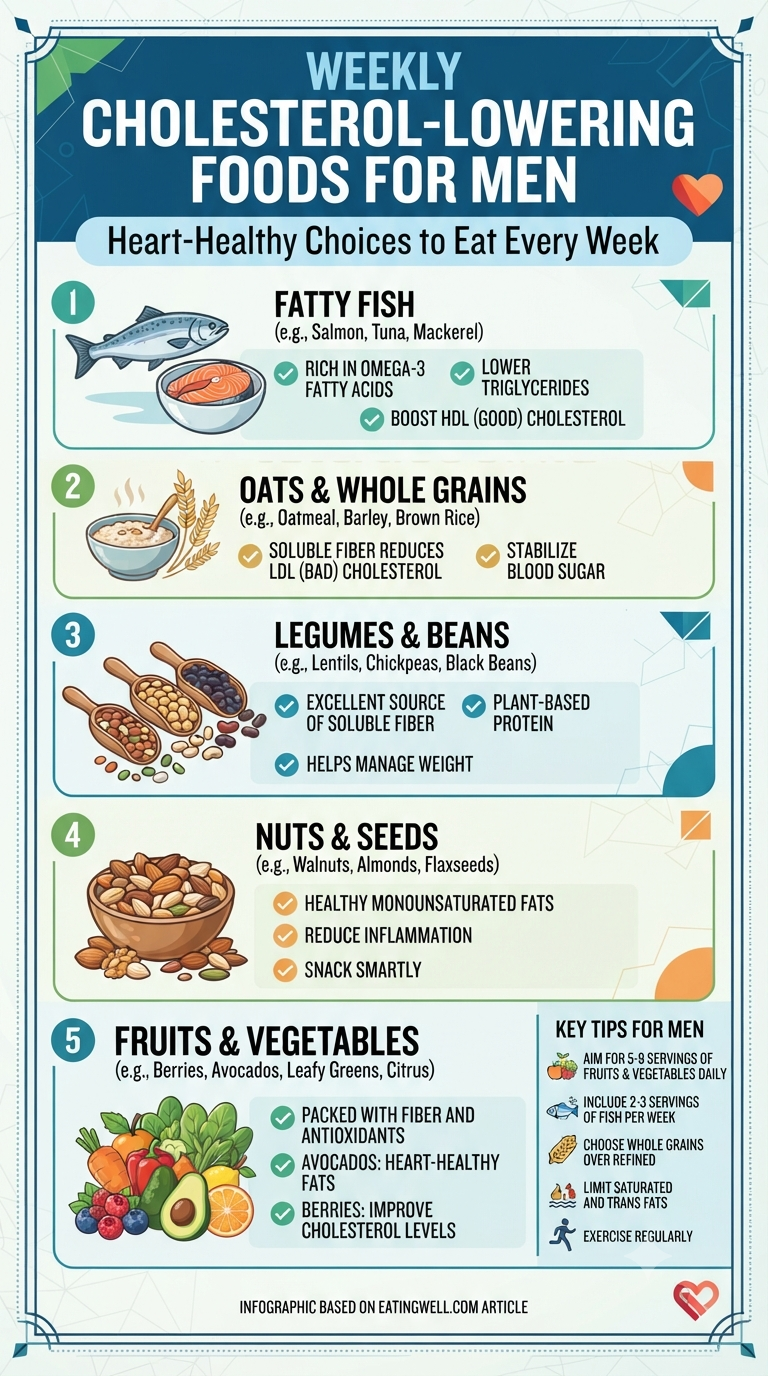

When it comes to longevity, men often focus on building muscle or increasing stamina, but there is a silent powerhouse that deserves just as much attention: your cholesterol levels. Managing cholesterol isn’t just about what you don’t eat—it’s about what you do add to your plate. If you’re looking for a simple, actionable way to…

Continue Reading Take Control of Your Heart Health: 5 Simple Foods to Add to Your Weekly Routine

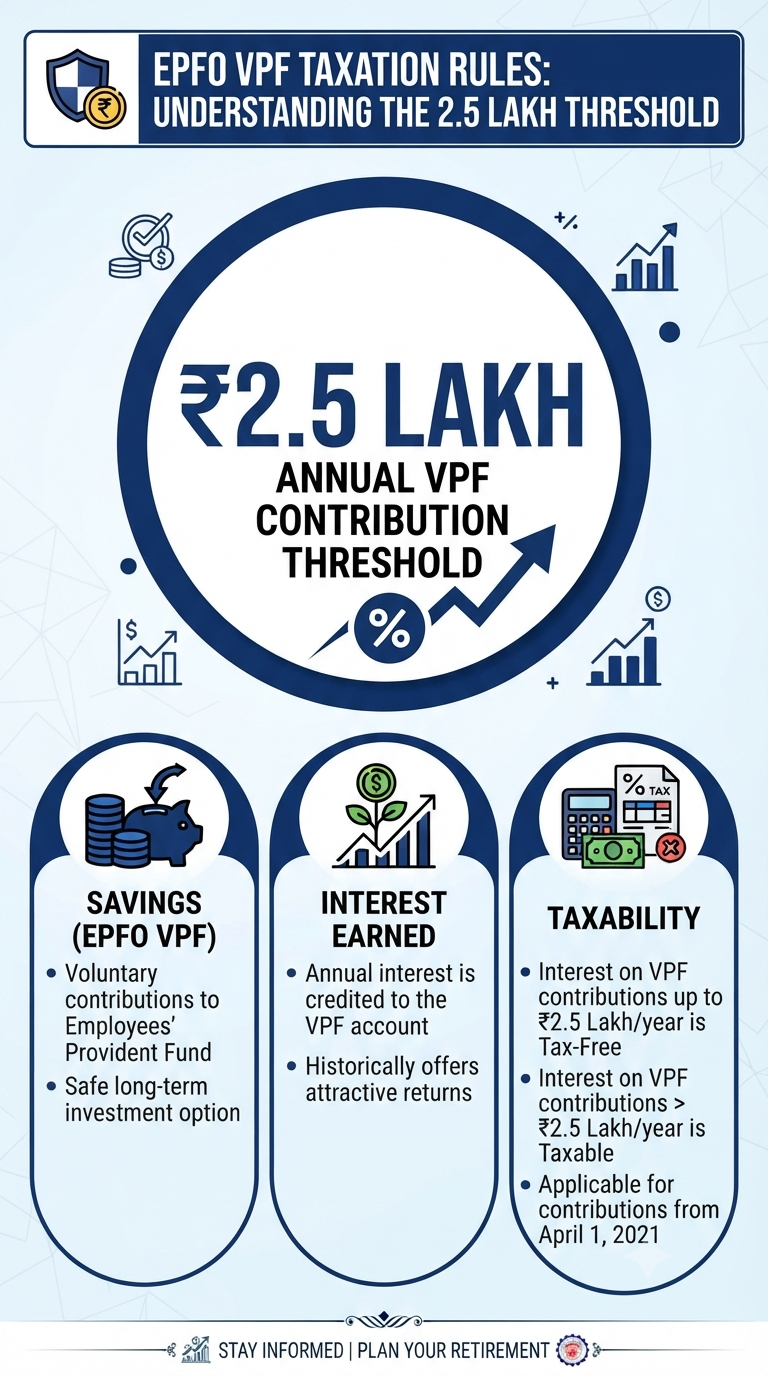

If you’ve been meticulously planning your retirement and using the Voluntary Provident Fund (VPF) as your go-to “set it and forget it” investment vehicle, you’re not alone. It’s a favorite for conservative investors who love the safety, the government backing, and those consistent returns that often outshine standard savings instruments. But, if you’ve been pumping…

Continue Reading Beyond the Threshold: Making Sense of the EPFO VPF Taxation Rule

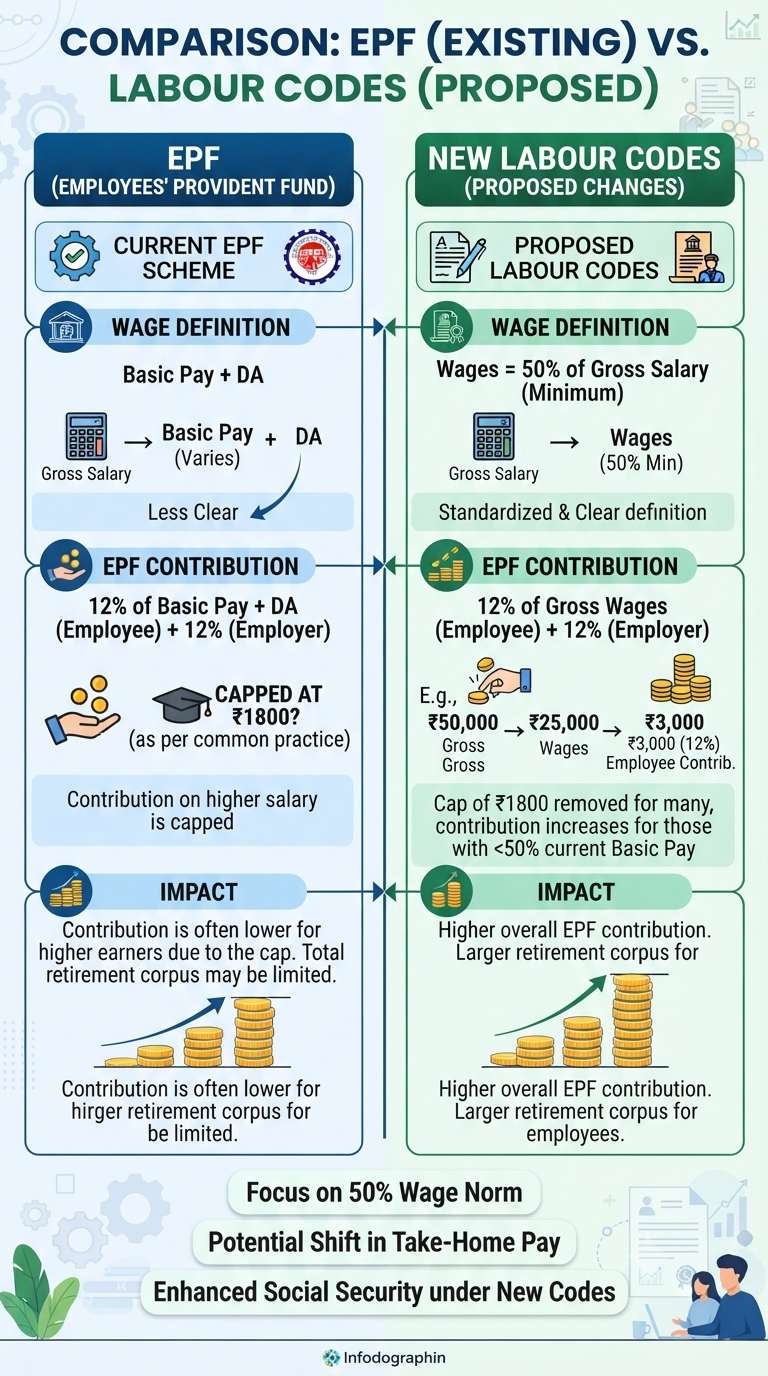

If you’ve recently opened your payslip with a sense of bewilderment, you aren’t alone. Between the buzz surrounding India’s new Labour Codes and the persistent questions about that mysterious ₹1,800 Provident Fund (PF) cap, the world of personal finance can feel like a labyrinth. But what exactly is changing, and more importantly, what does it…

Continue Reading The Great Salary Shift: Decoding the Labour Codes and the EPF Cap Myth

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.