When you’re renting a home in India, the tax rules can sometimes feel like navigating a maze. One of the most common questions that lands in the inbox of tax experts is this: “I pay more than ₹50,000 in monthly rent, but the property is owned by two people. Each of them receives less than ₹50,000. Do I still need to deduct TDS?”

It’s a situation many tenants find themselves in, and it’s easy to feel anxious about getting it wrong. The fear of penalties or compliance headaches often leads people to deduct tax when they don’t actually need to.

If you are currently confused about your obligations under Section 194IB of the Income Tax Act, let’s clear the air once and for all.

The ₹50,000 Threshold: Who Does It Really Apply To?

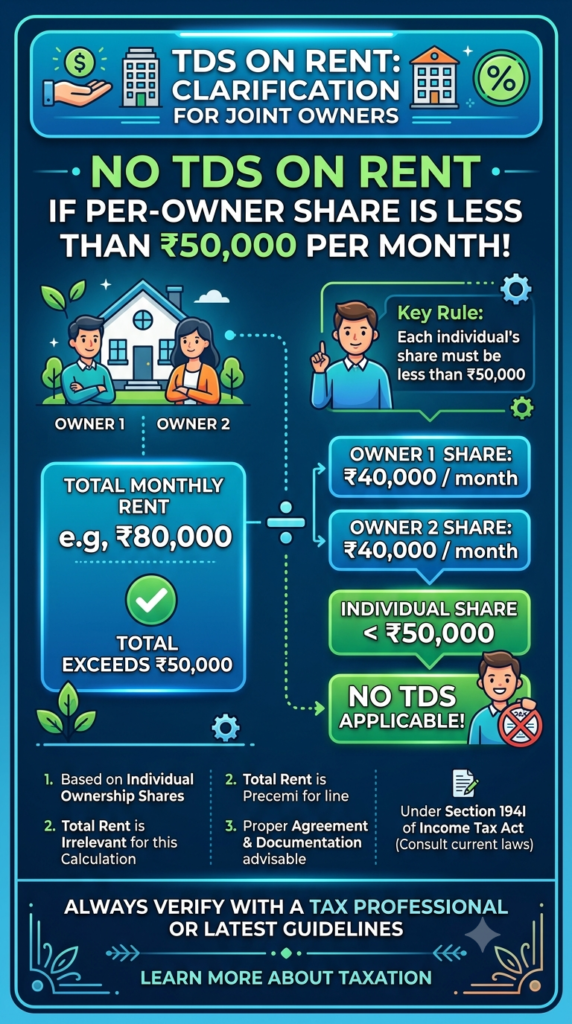

First, let’s look at the basic rule. Under Section 194IB, an individual or a Hindu Undivided Family (HUF)—who is not otherwise required to conduct a tax audit—must deduct 2% TDS from the rent they pay if the monthly rent exceeds ₹50,000.

Now, here is where the confusion usually starts: Is that ₹50,000 limit for the property or for the landlord?

The short answer: It’s for the landlord.

The law is clear that the threshold of ₹50,000 applies to each individual payee. The tax authorities look at the money received by each owner. If the property has joint owners, the total rent is split between them according to their ownership share.

The “Joint Owner” Exception: A Simple Example

Let’s imagine you are paying a total monthly rent of ₹80,000 for your apartment. If you were paying this to a single landlord, you would definitely need to deduct 2% TDS.

However, if that property is owned by two people (let’s say a husband and wife) with equal shares, each of them effectively receives ₹40,000 per month.

Since ₹40,000 is below the ₹50,000 threshold, you are not required to deduct TDS. Even though the aggregate rent for the property is well over the limit, your individual payment to each owner falls safely below it.

Why This Matters

- Reduced Paperwork: You don’t have to worry about filing Form 26QC or generating TDS certificates for landlords when you don’t meet the legal requirement.

- Peace of Mind: Understanding this rule saves you from unnecessary compliance burden.

- Clarity for Landlords: Being able to explain this rule to your landlord (who might also be confused about why they aren’t seeing TDS deductions) keeps your professional relationship transparent and smooth.

The Bottom Line

Before you start the process of deducting tax, always look at how much money is actually reaching the individual bank account of the landlord. If the amount is ₹50,000 or less, you can skip the TDS deduction process for that specific payment.

A Quick Tip: Always keep your rental agreement handy. It clearly states the ownership structure and the rent-sharing arrangement. This documentation is your best friend if you ever need to explain your tax position to the authorities.

Disclaimer: Tax laws are subject to change, and individual circumstances can vary. While this information is based on current Income Tax provisions, it is always a smart idea to consult with a qualified tax professional regarding your specific rental agreement and tax obligations.

Did you find this guide helpful? Keep this summary handy for your next rent payment cycle!

Unlock Any-Branch Banking: How to Upgrade Your Post Office CIF to e-KYC

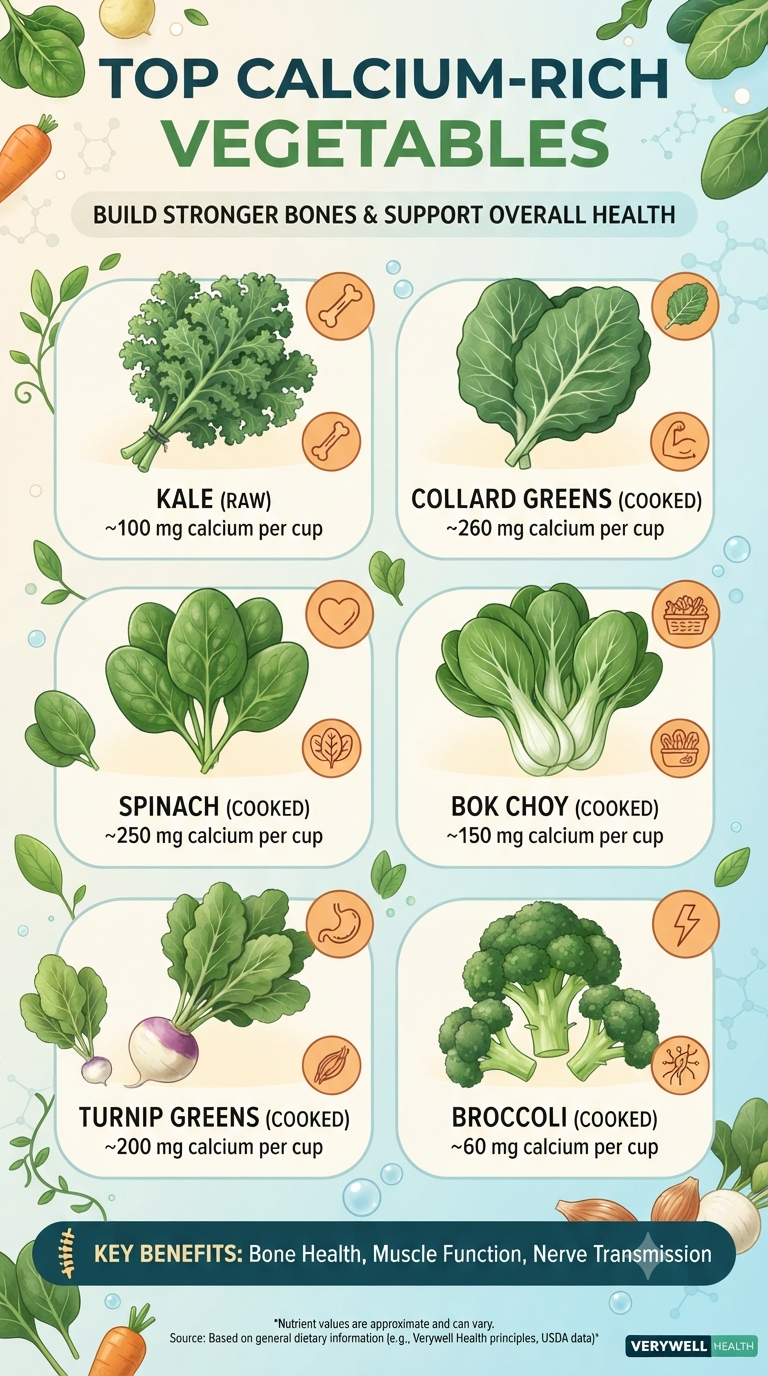

When we think of calcium, our minds often jump straight to a tall, frosty glass of milk or a wedge of cheddar. It’s the classic advice we’ve been given since childhood. But what if you aren’t a fan of dairy, or your body simply doesn’t agree with it? The good news is that you don’t…

Continue Reading Beyond Dairy: The Green Way to Stronger Bones

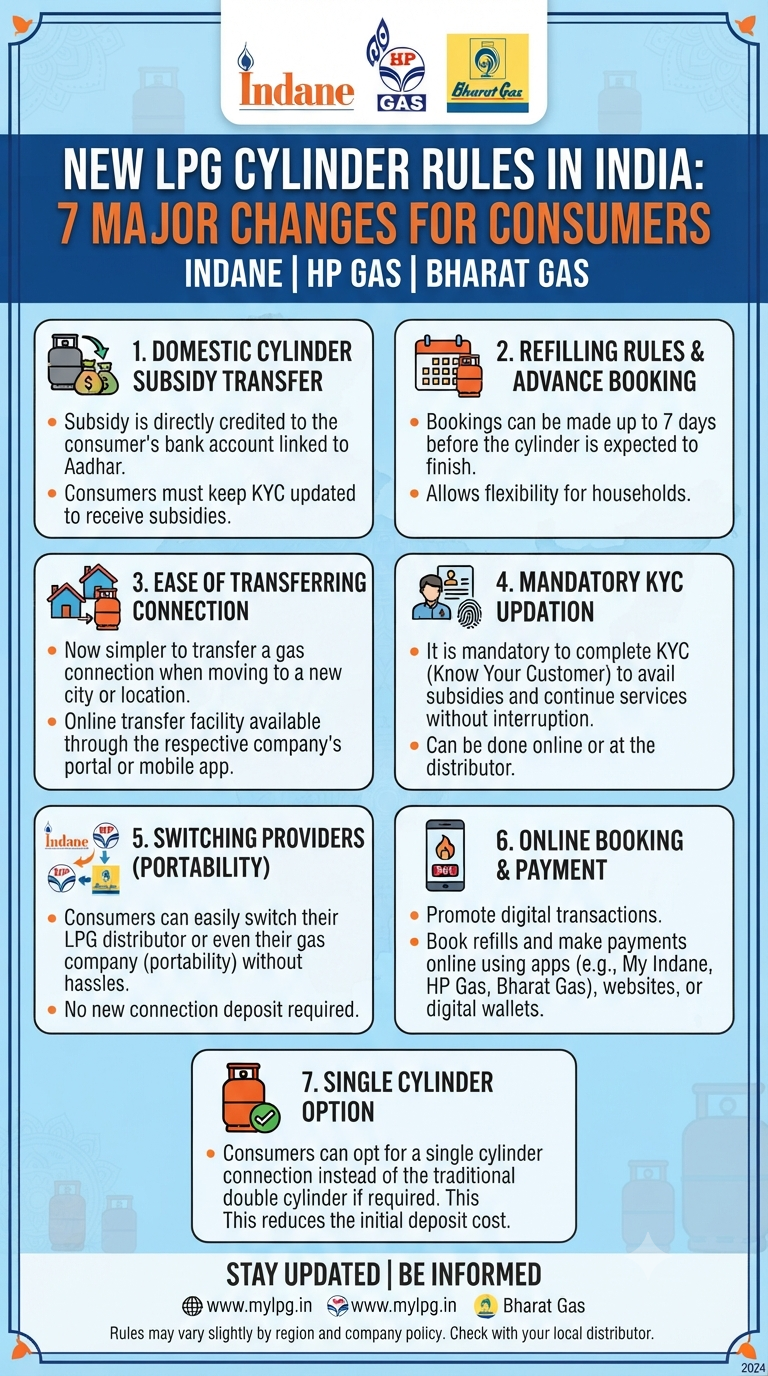

If you are a household consumer in India using Indane, HP Gas, or Bharat Gas, keeping up with changing policies can sometimes feel like a chore. However, staying informed is the best way to ensure you never face a disruption in your cooking gas supply or miss out on your hard-earned subsidies. Recent updates to…

Continue Reading New LPG Rules Simplified: 7 Major Changes You Need to Know

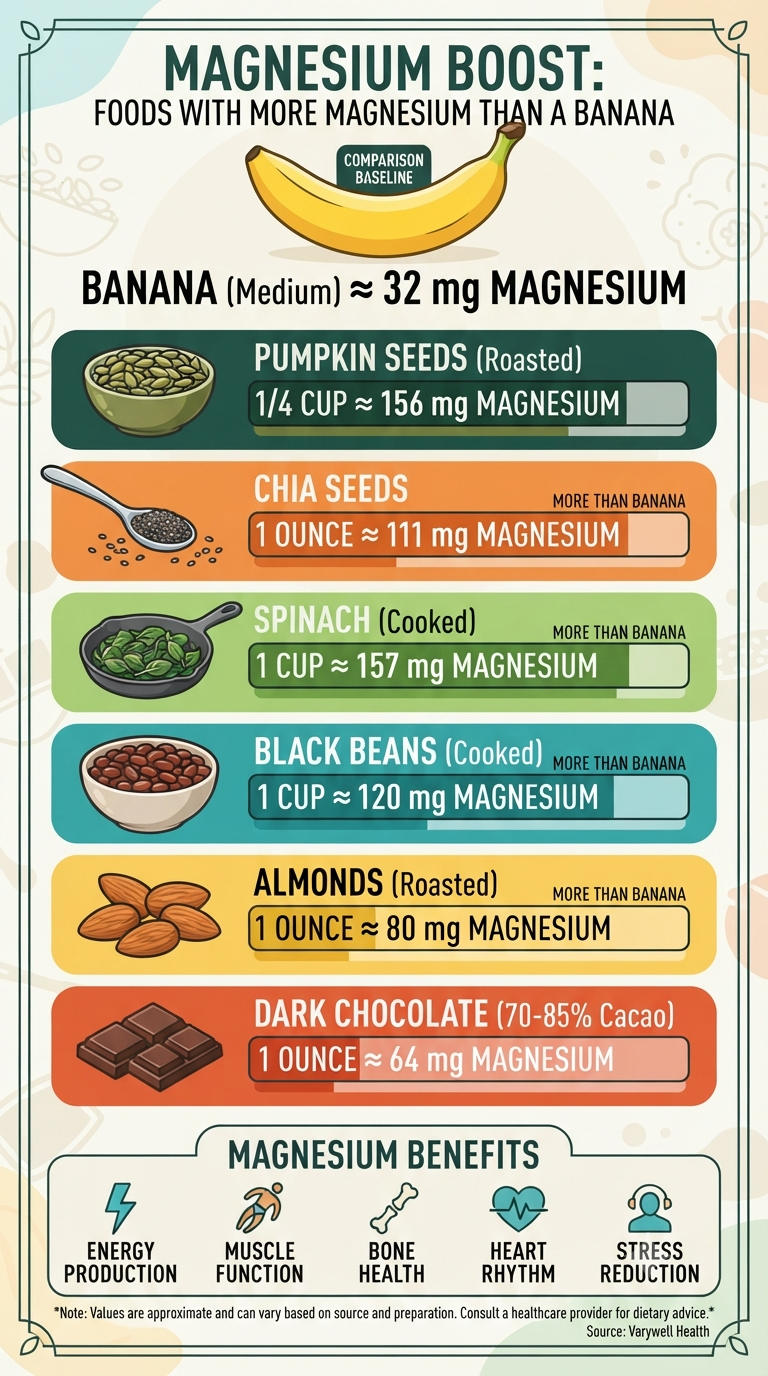

When we think of magnesium-rich foods, the humble banana often takes center stage. It’s convenient, affordable, and—let’s be honest—it’s been marketed as the go-to fruit for potassium and magnesium for decades. But did you know that your banana might actually be underperforming when it comes to your daily magnesium needs? Magnesium is an unsung hero…

Continue Reading Move Over, Banana: The Surprising Foods That Pack More Magnesium

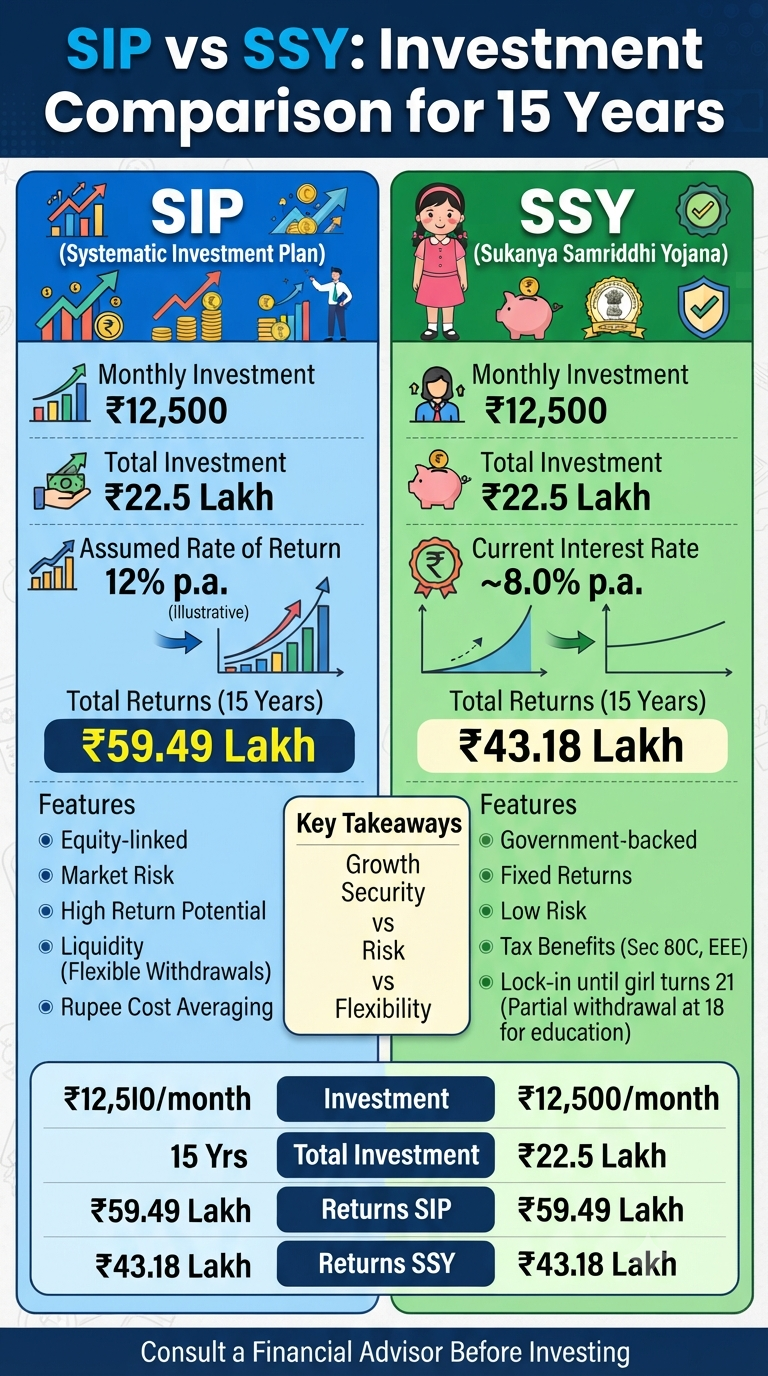

Investing for the future is crucial, and choosing the right investment avenue can make a significant difference in achieving your financial goals. Two popular options in India are the Systematic Investment Plan (SIP) and the Sukanya Samriddhi Yojana (SSY). Let’s delve into a detailed comparison to help you make an informed decision. SIP: Equity-linked and…

Continue Reading SIP vs. SSY: A Detailed Comparison for a Secure Financial Future

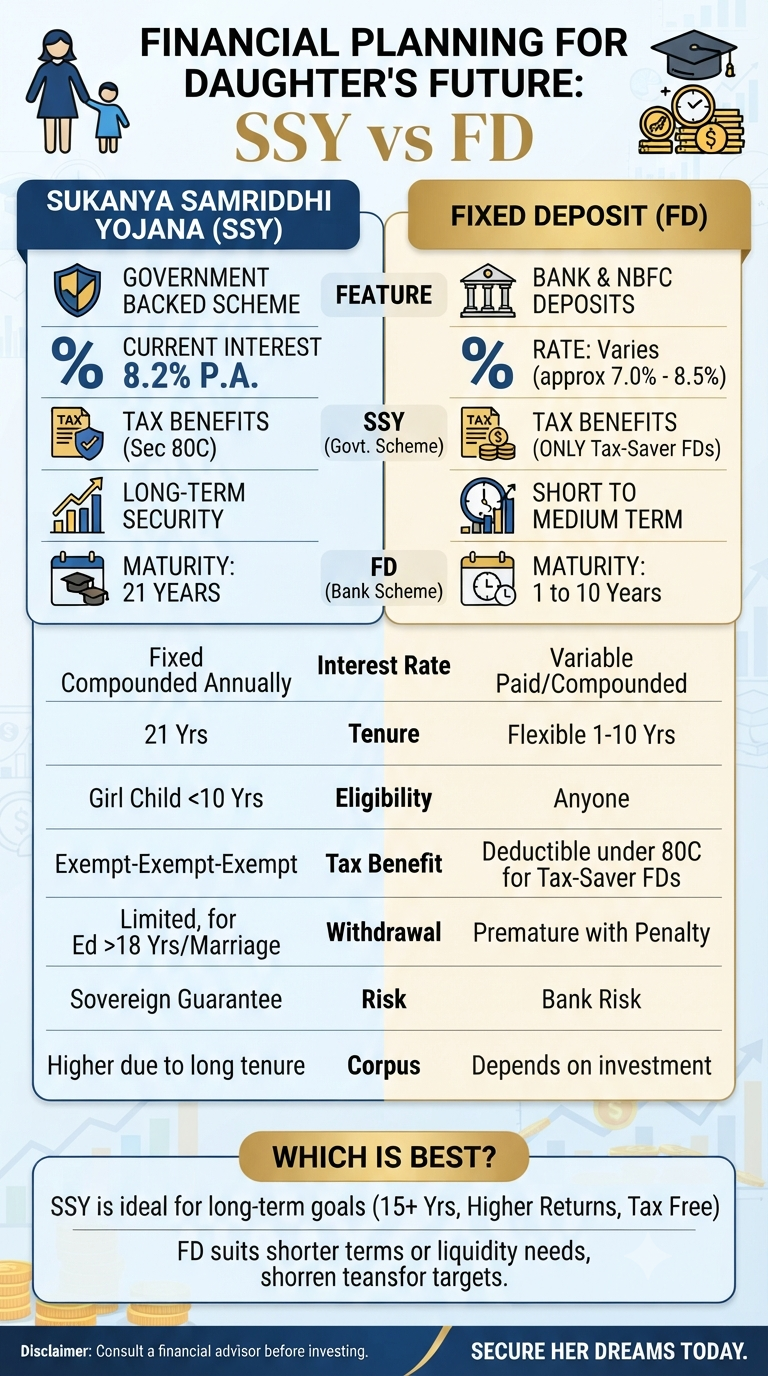

As parents, we are constantly looking ahead. We dream of our daughter’s college graduation, her first steps into a career, and perhaps her wedding day. But dreams, while priceless, require pragmatic financial planning to become reality. When it comes to securing a financial corpus for a girl child in India, two names inevitably pop up…

Continue Reading Secure Her Dreams: Decystifying the SSY vs. FD Battle for Your Daughter’s Future

We’ve all been there—staring at the bank balance, feeling the familiar squeeze of anxiety, and wondering when things will finally get easier. Often, we treat money problems purely as a logistical issue: we need more income, less debt, or a better budget. But what if the key to financial freedom isn’t just found in a…

Continue Reading From Scarcity to Abundance: 5 Daily Rituals to Unlock True Financial Prosperity

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.