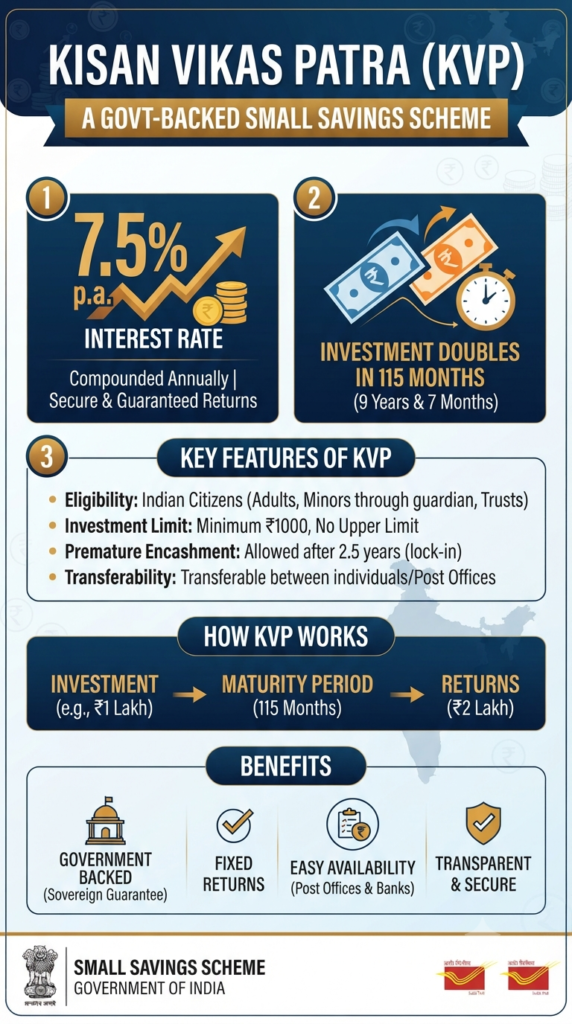

If you are a conservative investor—someone who likes to sleep soundly knowing your hard-earned money is growing in a safe, government-backed harbor—the Kisan Vikas Patra (KVP) has likely crossed your radar. For the July–September quarter, the government has reaffirmed its commitment to this classic scheme, keeping the interest rate steady at 7.5%.

But what does this actually mean for your wallet, and is it the right fit for your financial goals? Let’s break it down.

The “Magic” of 115 Months

The most popular aspect of the KVP is its straightforward promise: it doubles your money. At the current interest rate of 7.5%, your initial investment will take exactly 115 months—which translates to 9 years and 7 months—to reach double its value.

In an era where market volatility can feel like a roller coaster, there is something undeniably comforting about a predictable, guaranteed timeline for wealth accumulation.

Who is this for?

KVP isn’t designed to be a high-growth vehicle for aggressive stock market players. Instead, it is built for the risk-averse saver. Whether you are planning for a specific milestone a decade down the line or just want a secure place to park excess savings without worrying about market crashes, KVP fits the bill.

Eligibility is simple:

- Adults: You can open an account individually or jointly (up to three adults).

- Minors: A guardian can open an account on behalf of a minor, or a child over the age of 10 can open one in their own name.

The Need-to-Know Technicals

While the scheme is simple, it’s important to understand the “fine print” before you visit your local post office:

- Low Barrier to Entry: You can start with as little as ₹1,000, and there is absolutely no upper limit on how much you can invest.

- Taxation: It is essential to remember that the interest earned is fully taxable according to your specific income tax slab. Unlike some tax-saving instruments, KVP does not offer tax exemptions on the interest income.

- The “Lock-in” Factor: KVP is designed for the long haul. While the funds are locked in until maturity, the government does allow for premature closure under specific conditions, providing a small safety net if an emergency arises.

- Compliance: To keep things transparent, PAN is mandatory for investments exceeding ₹50,000, and for those investing ₹10 lakh or more, you’ll need to provide income proof, such as ITR filings or salary slips.

How to Get Started

Opening a KVP account is a refreshingly analog, “old school” experience. You simply need to visit your nearest post office, pick up Form A, and bring along your KYC documents (Aadhaar and PAN). Once your details are verified, you’ll receive your KVP certificate—a tangible piece of paper representing your growing investment.

Final Thoughts

Is the Kisan Vikas Patra going to make you a millionaire overnight? No. But that isn’t its purpose. In a world of financial uncertainty, KVP stands as a reliable, government-guaranteed pillar for your portfolio. It’s a tool for patience, discipline, and long-term security.

If you are looking for a place where your money can sit safely, grow steadily, and be there for you when you need it most, KVP remains a timeless choice.

Disclaimer: Investment decisions should be made based on your personal financial goals and tax situation. Always consult with a financial advisor before committing to long-term savings schemes.

A Simple Guide to Paying Your LIC Premium Online

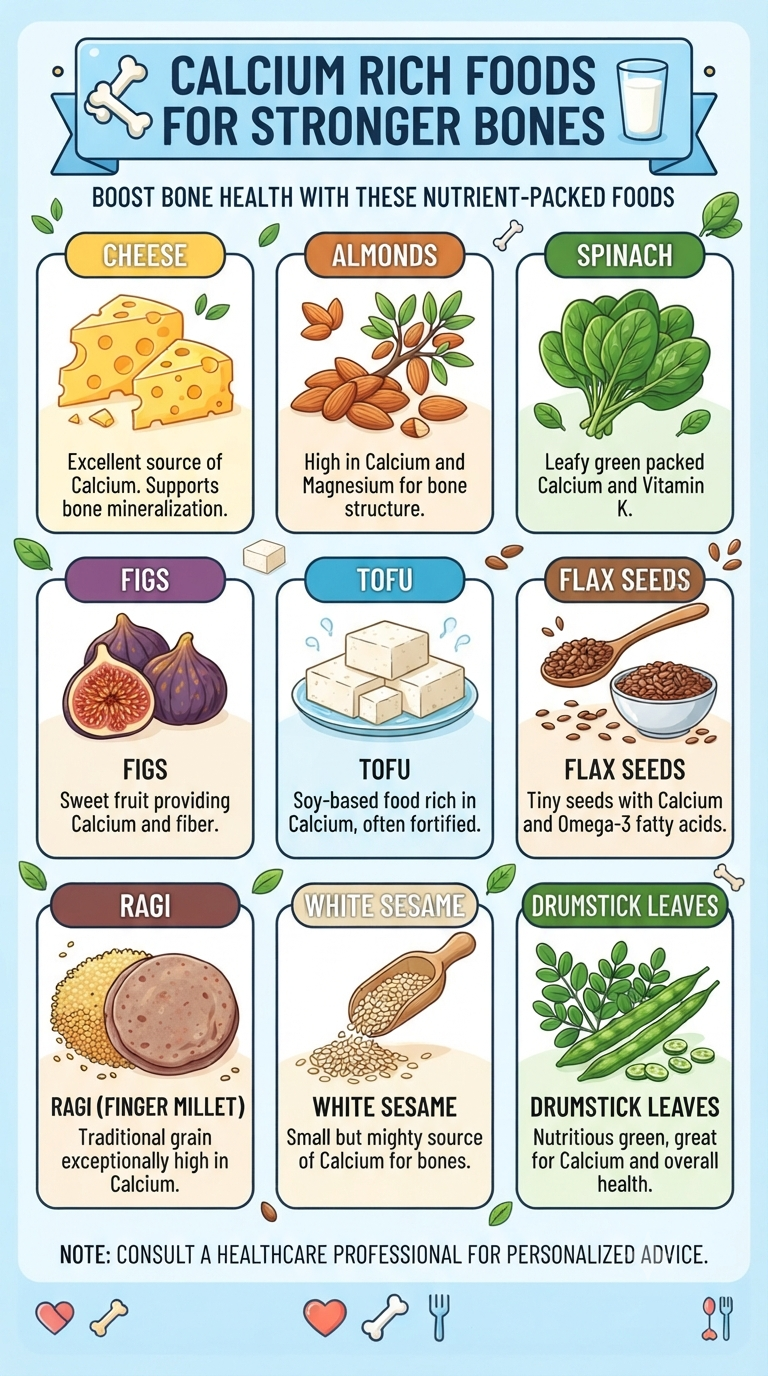

We often think of bone health as something to worry about only in our later years, but the truth is that your bones are constantly changing. Think of them like a savings account; what you “deposit” into your diet today determines how strong your skeletal structure will be tomorrow. Calcium is the cornerstone of that…

Continue Reading Unlock Stronger Bones: The Top Calcium-Rich Foods You Should Add to Your Diet Today

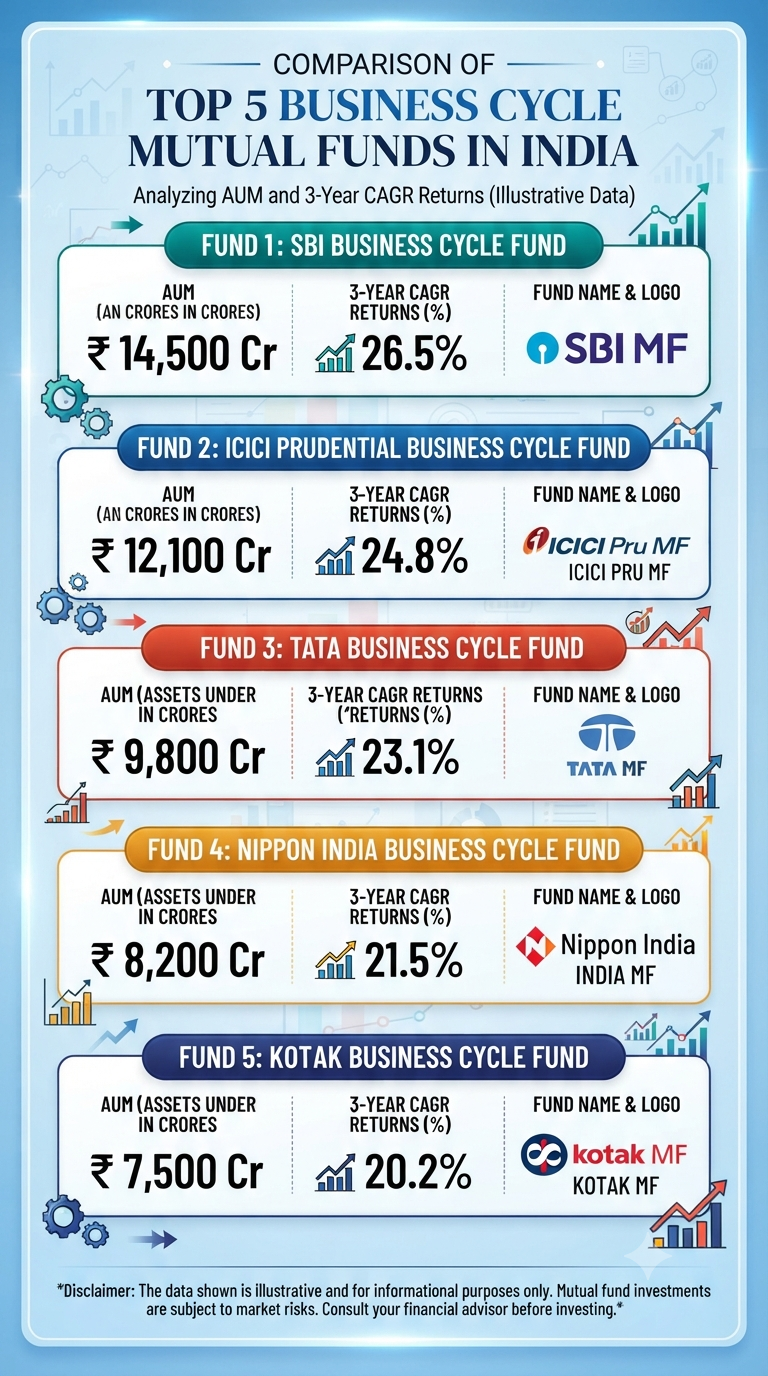

The Indian economy is a vibrant, ever-shifting landscape. Just as the seasons change, so do the fortunes of different industries. This dynamic is known as the business cycle, a natural ebb and flow of economic expansion and contraction. For investors, understanding these cycles isn’t just academic; it’s a crucial skill for identifying opportunities and managing…

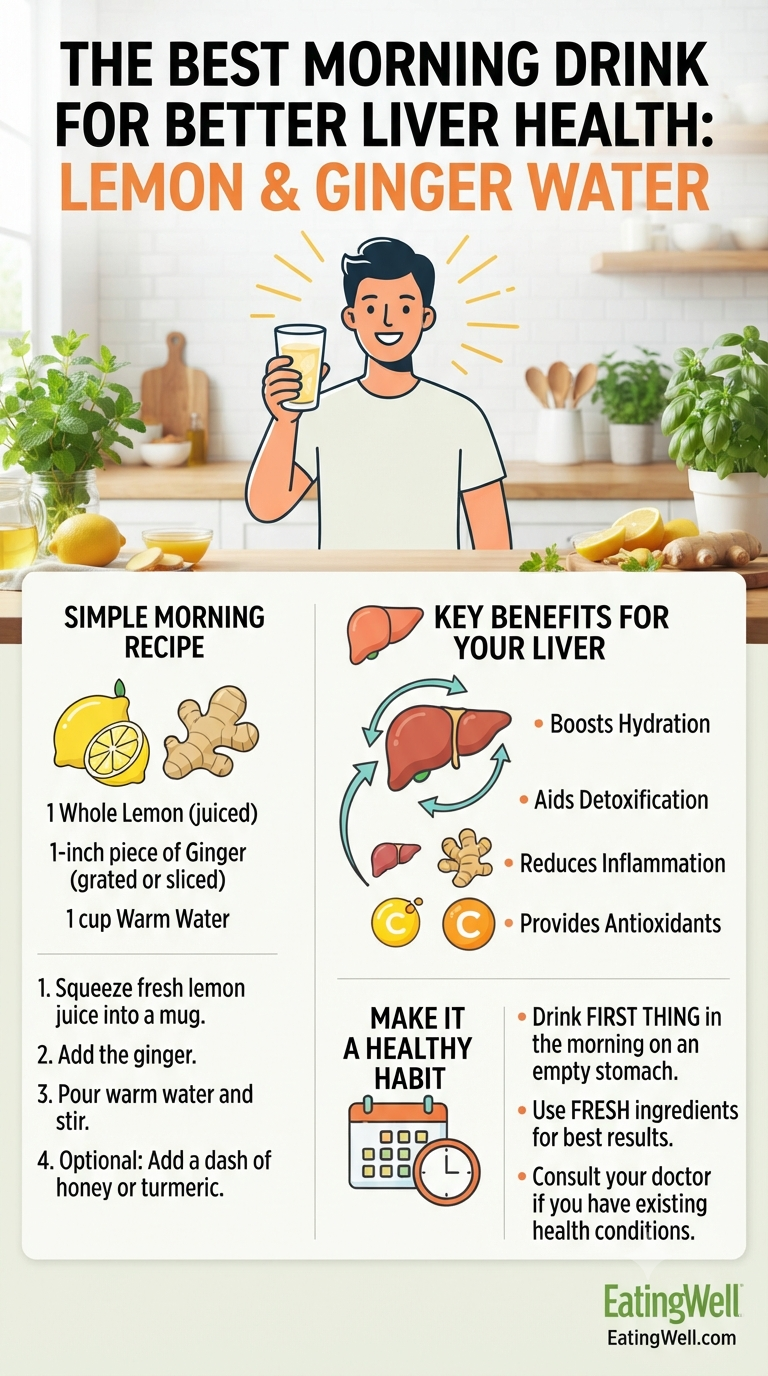

We often talk about kickstarting our metabolism or waking up our brains, but how often do you think about your liver first thing in the morning? Your liver is the ultimate multitasker, working tirelessly to filter your blood, process nutrients, and detoxify your body. Given how hard it works, it deserves a little extra love.…

Continue Reading Wake Up Your Liver: Why Lemon & Ginger Water Is Your Morning Must-Have

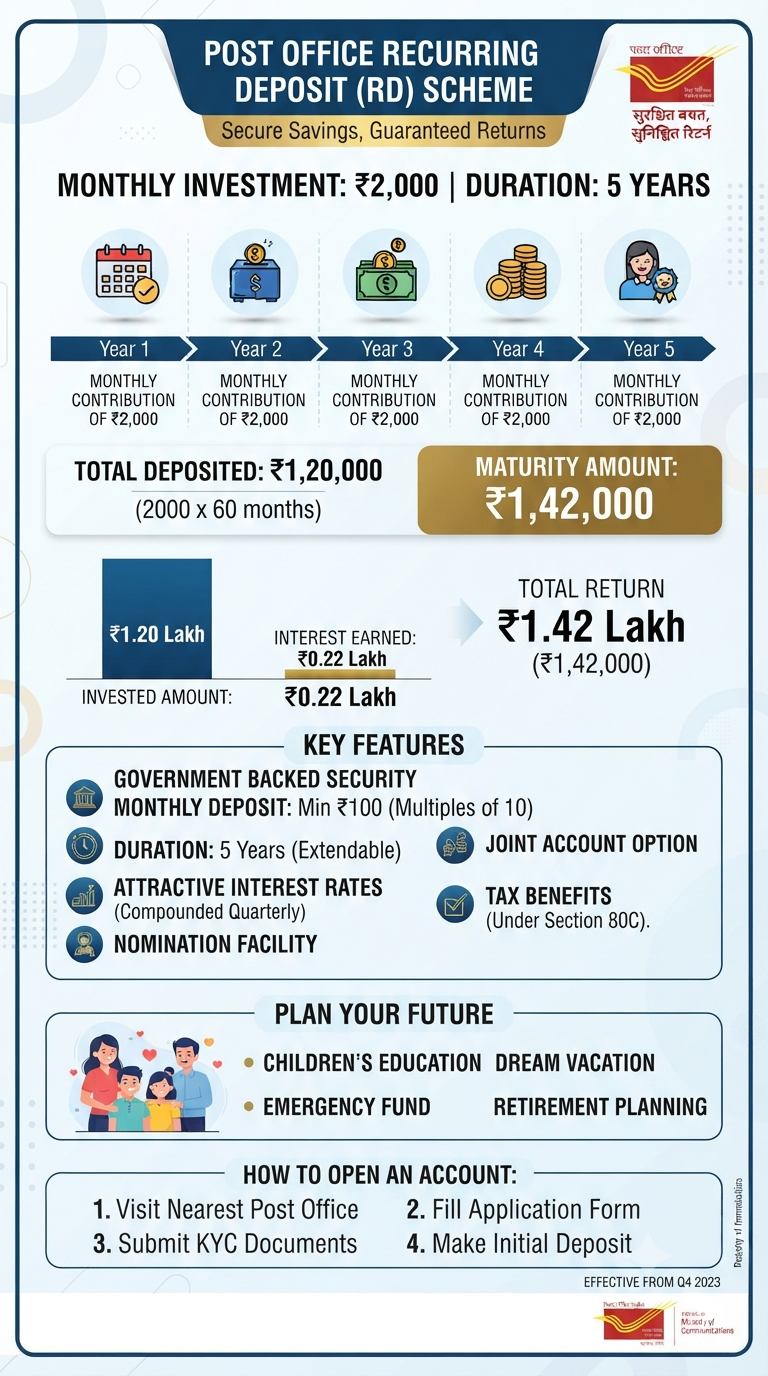

In today’s volatile financial landscape, where market fluctuations can turn a sound investment strategy upside down overnight, finding a safe haven for your hard-earned money is more important than ever. If you are looking for a risk-free way to grow your wealth, you don’t always need a high-risk portfolio. Sometimes, the most powerful tool is…

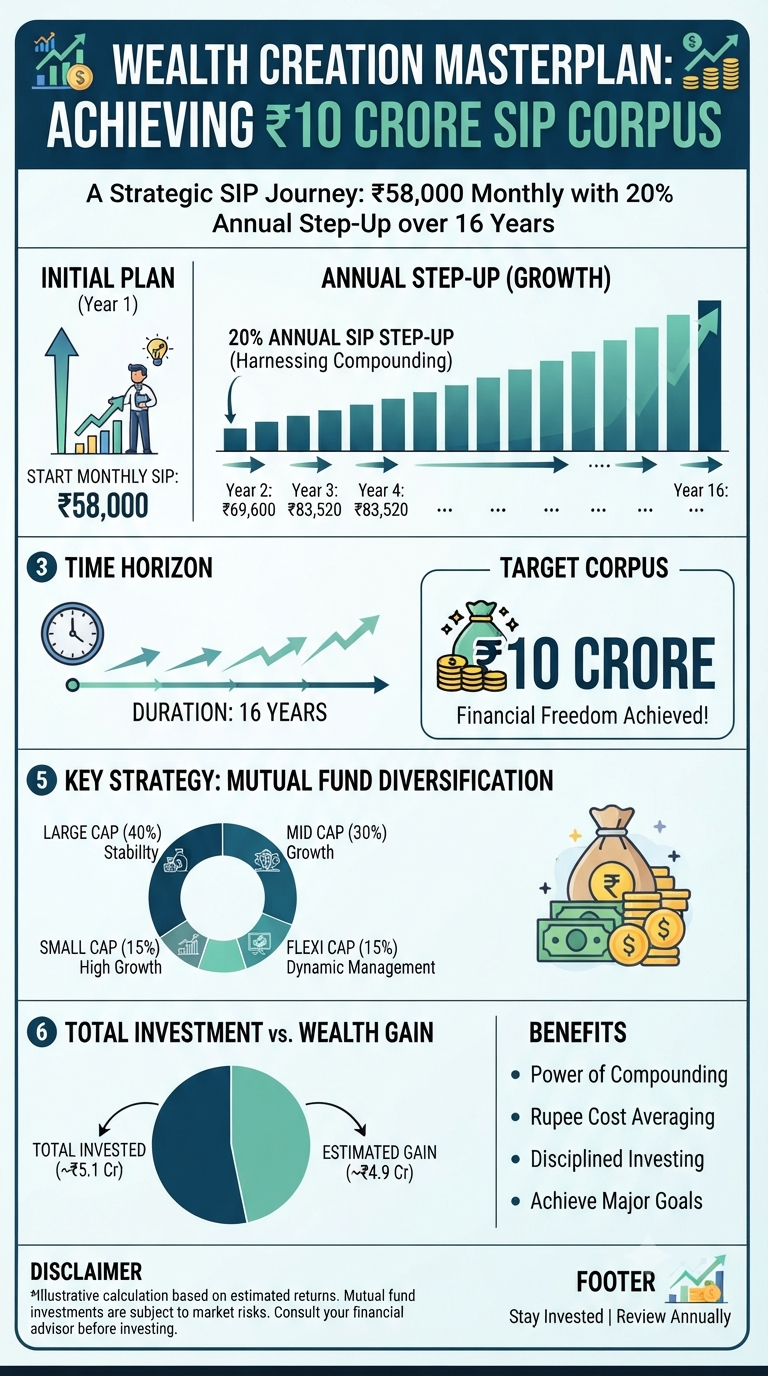

We all dream of financial freedom—that golden ticket where our money works harder for us than we ever did for it. But for most of us, that dream feels like exactly that: a dream. Something reserved for lottery winners or tech entrepreneurs. But what if I told you that you could build a ₹10 Crore…

Continue Reading The ₹10 Crore Dream: Is a Strategic SIP the Ultimate Wealth Creation Masterplan?

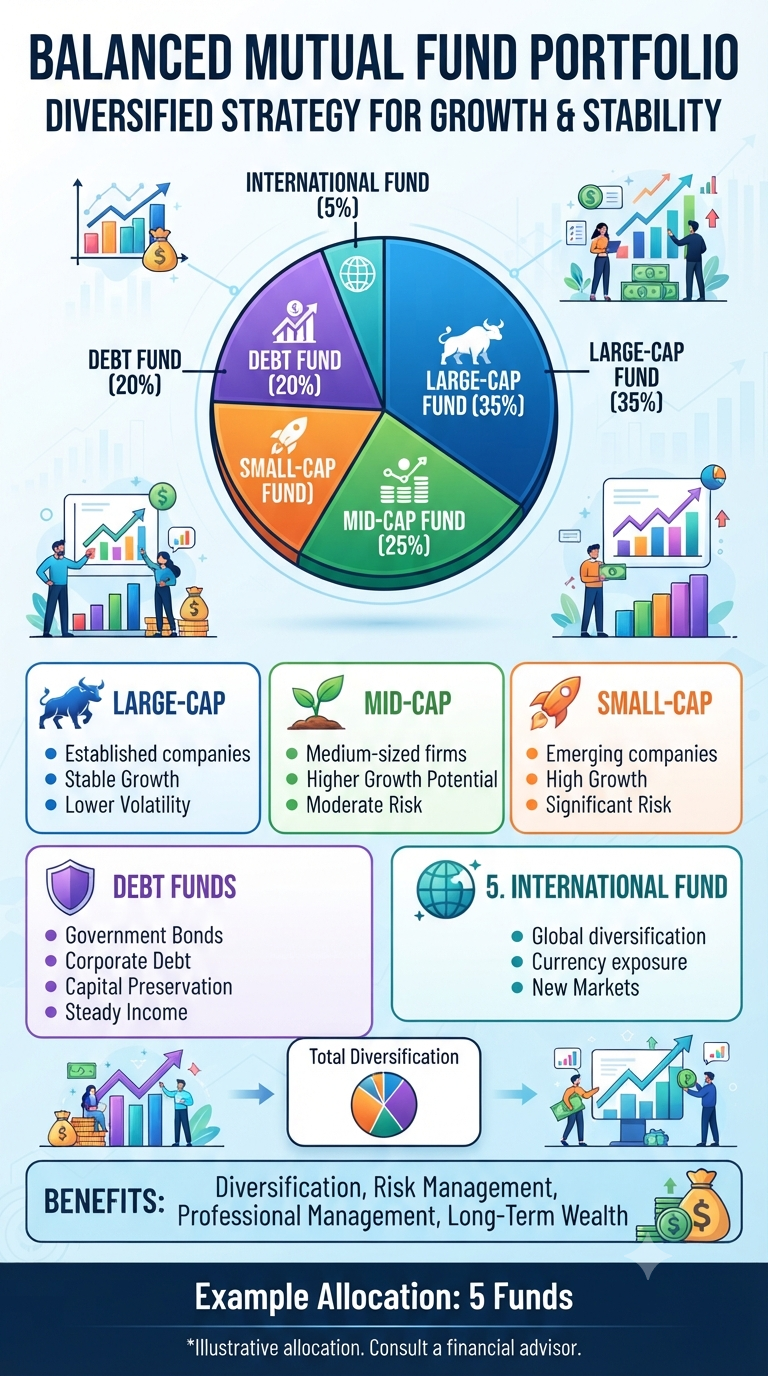

We’ve all been there—scrolling through an investment app, seeing a shiny new mutual fund, and thinking, “Why not? Adding another one can’t hurt, right?” It’s easy to fall into the trap of “fund collecting.” You assume that by holding ten, fifteen, or twenty different schemes, you’re becoming the ultimate master of diversification. But according to…

Continue Reading Less is More: Why Your Portfolio Doesn’t Need a Dozen Mutual Funds

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.