As parents, we are constantly looking ahead. We dream of our daughter’s college graduation, her first steps into a career, and perhaps her wedding day. But dreams, while priceless, require pragmatic financial planning to become reality.

When it comes to securing a financial corpus for a girl child in India, two names inevitably pop up in every discussion: Sukanya Samriddhi Yojana (SSY) and a traditional Fixed Deposit (FD). Both offer a safe haven for your money, but they are built for very different purposes.

Is the government-backed SSY the undisputed champion, or does the flexibility of an FD make more sense for your family’s unique situation? Let’s break it down.

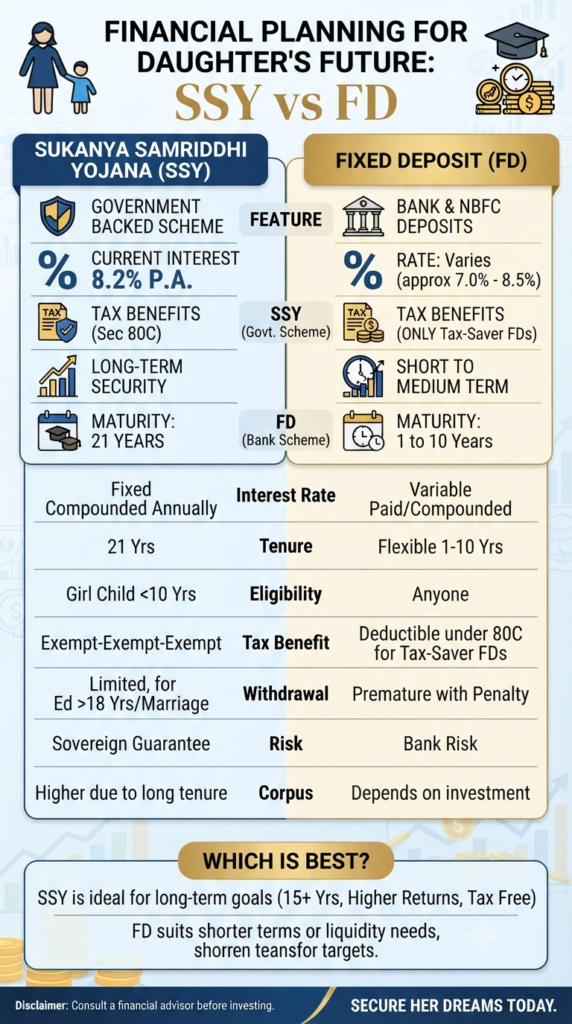

The Tale of the Tape: SSY vs. FD

Before we dive into the strategy, let’s look at the core features at a glance, comparing the blue corner (SSY) and the gold corner (FD).

- Safety First: Both are extremely safe. SSY carries a Sovereign Guarantee, meaning it is backed by the Government of India. An FD carries Bank Risk, though with deposit insurance, it is generally considered safe for typical investment amounts.

- The Power of Returns: Currently, SSY offers an attractive 8.2% P.A. interest rate, which is typically higher than most bank FDs, which range between 7.0% to 8.5%. Crucially, SSY interest is Fixed and Compounded Annually, guaranteeing that rate for the long haul.

- Tax Efficiency (The Game Changer): This is often the deciding factor. SSY falls under the coveted EEE (Exempt-Exempt-Exempt) category. Your investment qualifies for deduction under Sec 80C, the interest earned is tax-free, and the final maturity amount is 100% tax-free. Tax-saver FDs also offer Sec 80C benefits, but the interest earned is fully taxable according to your income slab.

The 5 Critical Differences That Matter to Parents

Numbers are one thing, but how these schemes work in the real world depends on your circumstances.

1. The Time Horizon

- SSY is a Marathon: This is a long-term commitment. The maturity is 21 YEARS from the date of account opening. While you only need to deposit for 15 years, the money stays locked in until that 21-year mark.

- FD is a Sprint (or a Stroll): FDs offer incredible flexibility. You can lock in your money for anywhere from 1 to 10 Years, making them perfect for short-to-medium term goals.

2. Access and Eligibility

- SSY: This is exclusively for a Girl Child, and the account must be opened before she turns 10.

- FD: Anyone can open an FD—you, your spouse, or your daughter herself, regardless of age.

3. Liquidity (The “Emergency Hatch”)

Life is unpredictable. What if you need the money before maturity?

- SSY: It has limited liquidity. You can only make a partial withdrawal (up to 50% of the corpus) after she turns 18 for higher education.

- FD: This is highly liquid. You can break the FD prematurely, though banks will charge a penalty for premature withdrawal.

4. Building the Corpus

Because SSY leverages a longer tenure and higher interest rates (which compound), it is designed to build a significantly larger corpus for your daughter’s major milestones. An FD’s final amount depends heavily on your initial investment amount and the prevailing interest rates at the time of renewal.

5. Risk Assessment

SSY is virtually risk-free due to the government backing. FDs are also very safe, but are tied to the health of the specific financial institution holding your deposit.

The Verdict: Which One is Right for You?

There is no single “best” option; there is only what is best for your specific timeline and financial goals.

Choose Sukanya Samriddhi Yojana (SSY) if:

- Your daughter is young (under 10).

- Your goal is specifically her long-term future, such as university education or marriage, which are 15+ years away.

- You want the highest guaranteed, tax-free returns without market volatility.

- You do not need to access this capital for emergencies.

Choose a Fixed Deposit (FD) if:

- You are planning for medium-term goals (e.g., a “pre-college fund” for ages 14-18).

- You prefer flexibility in tenure and investment amounts.

- You value high liquidity and want the option to withdraw funds in case of a family emergency (even with a penalty).

- You have a lump sum to invest that you want to “park” securely.

Final Thought: For many parents, the optimal strategy isn’t SSY or FD, but SSY and FD. You can use SSY as the bedrock for long-term security, and utilize FDs to ladder smaller investments for nearer-term requirements.

No matter which path you choose, the most important step is starting today. Secure her dreams, one deposit at a time.

Disclaimer: Consult a qualified financial advisor before making any investment decisions based on this information.

From Scarcity to Abundance: 5 Daily Rituals to Unlock True Financial Prosperity

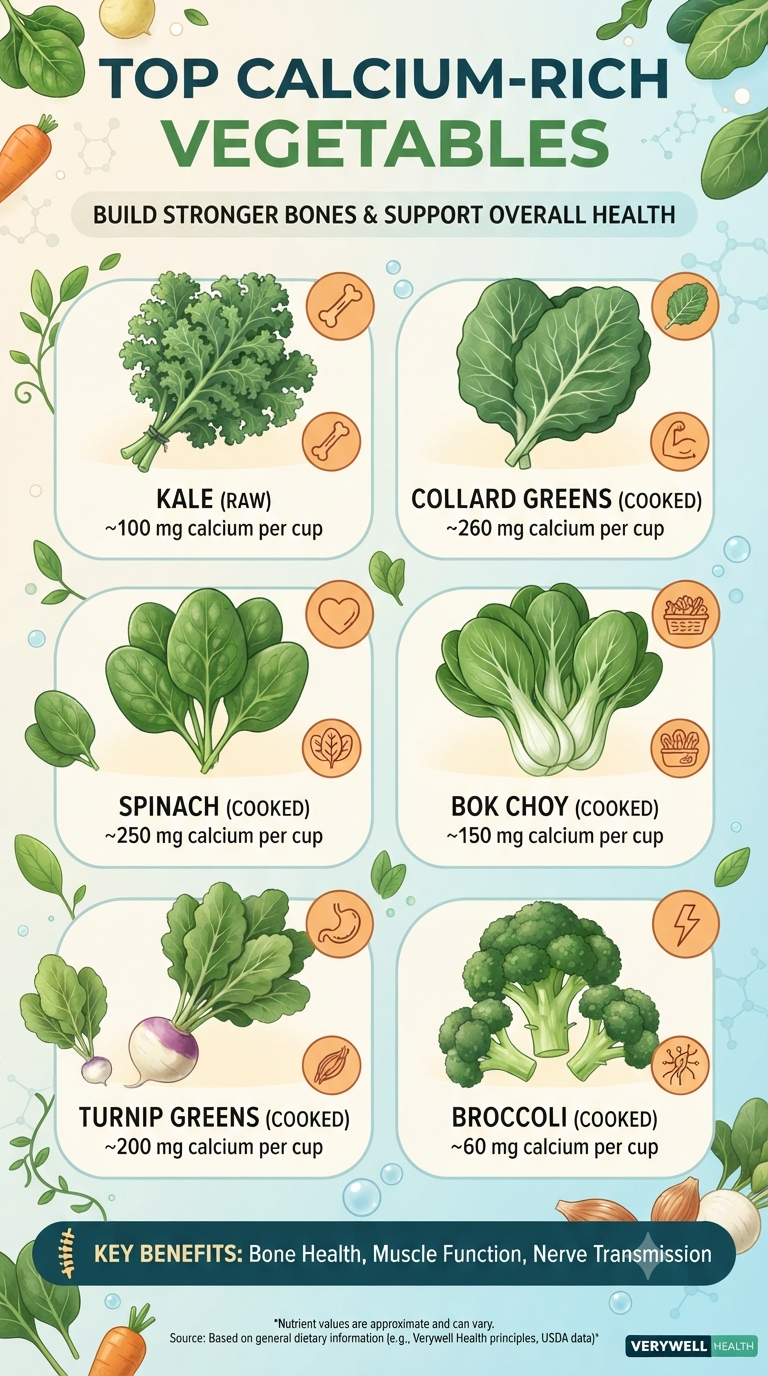

When we think of calcium, our minds often jump straight to a tall, frosty glass of milk or a wedge of cheddar. It’s the classic advice we’ve been given since childhood. But what if you aren’t a fan of dairy, or your body simply doesn’t agree with it? The good news is that you don’t…

Continue Reading Beyond Dairy: The Green Way to Stronger Bones

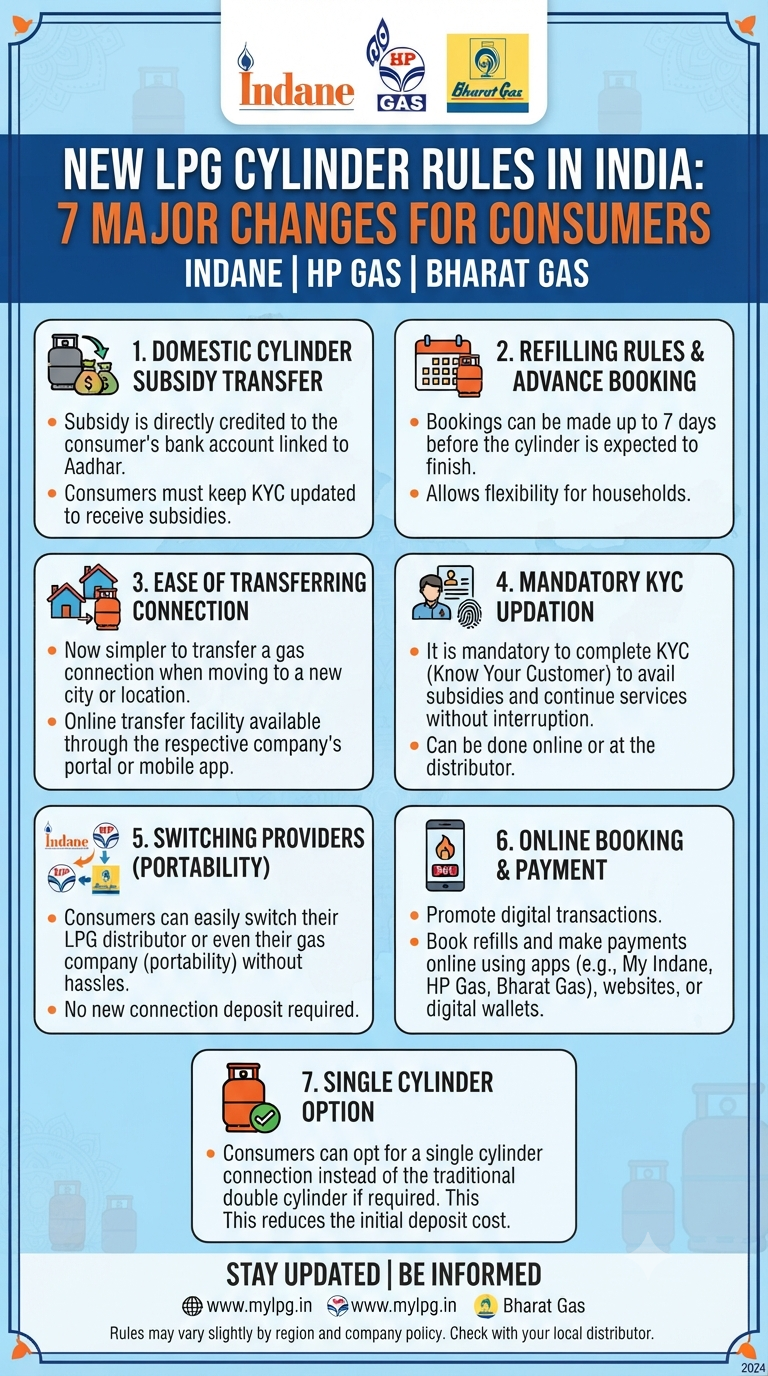

If you are a household consumer in India using Indane, HP Gas, or Bharat Gas, keeping up with changing policies can sometimes feel like a chore. However, staying informed is the best way to ensure you never face a disruption in your cooking gas supply or miss out on your hard-earned subsidies. Recent updates to…

Continue Reading New LPG Rules Simplified: 7 Major Changes You Need to Know

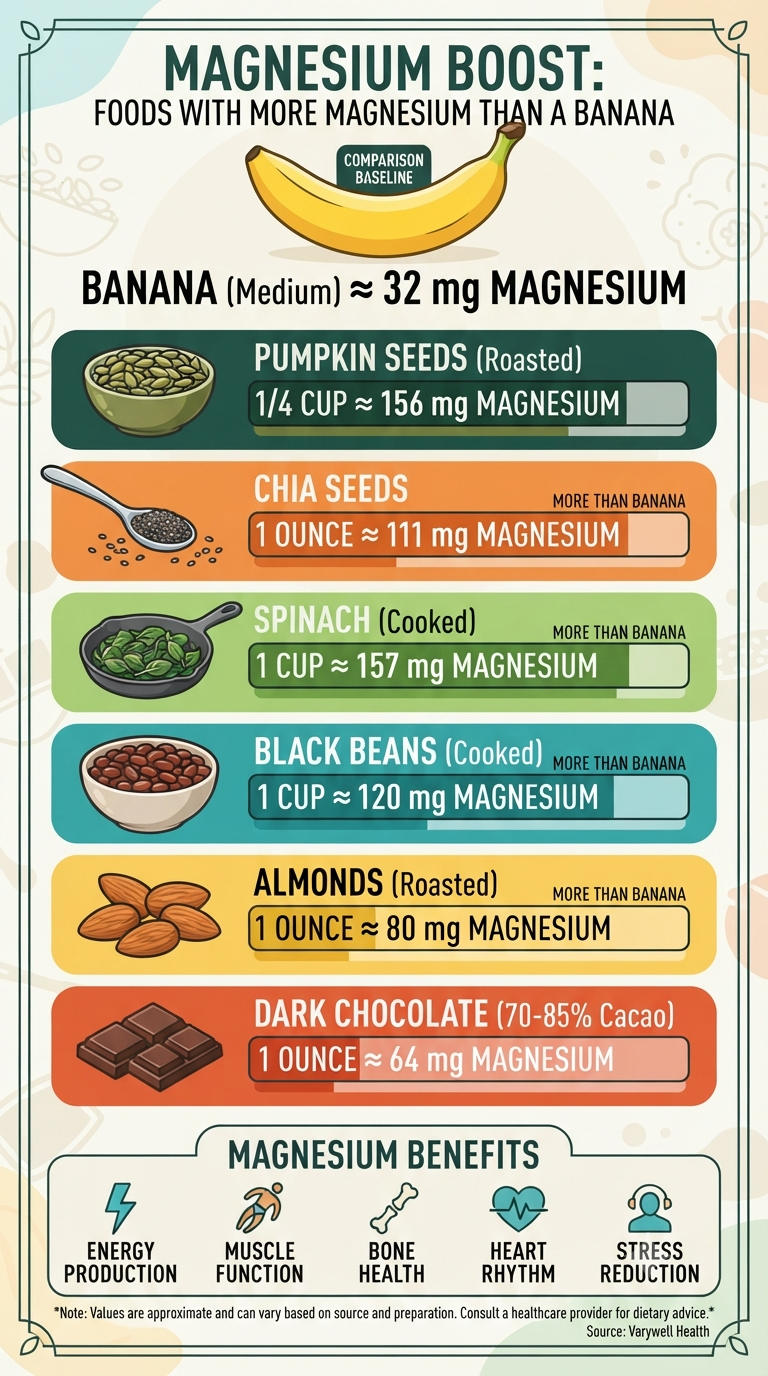

When we think of magnesium-rich foods, the humble banana often takes center stage. It’s convenient, affordable, and—let’s be honest—it’s been marketed as the go-to fruit for potassium and magnesium for decades. But did you know that your banana might actually be underperforming when it comes to your daily magnesium needs? Magnesium is an unsung hero…

Continue Reading Move Over, Banana: The Surprising Foods That Pack More Magnesium

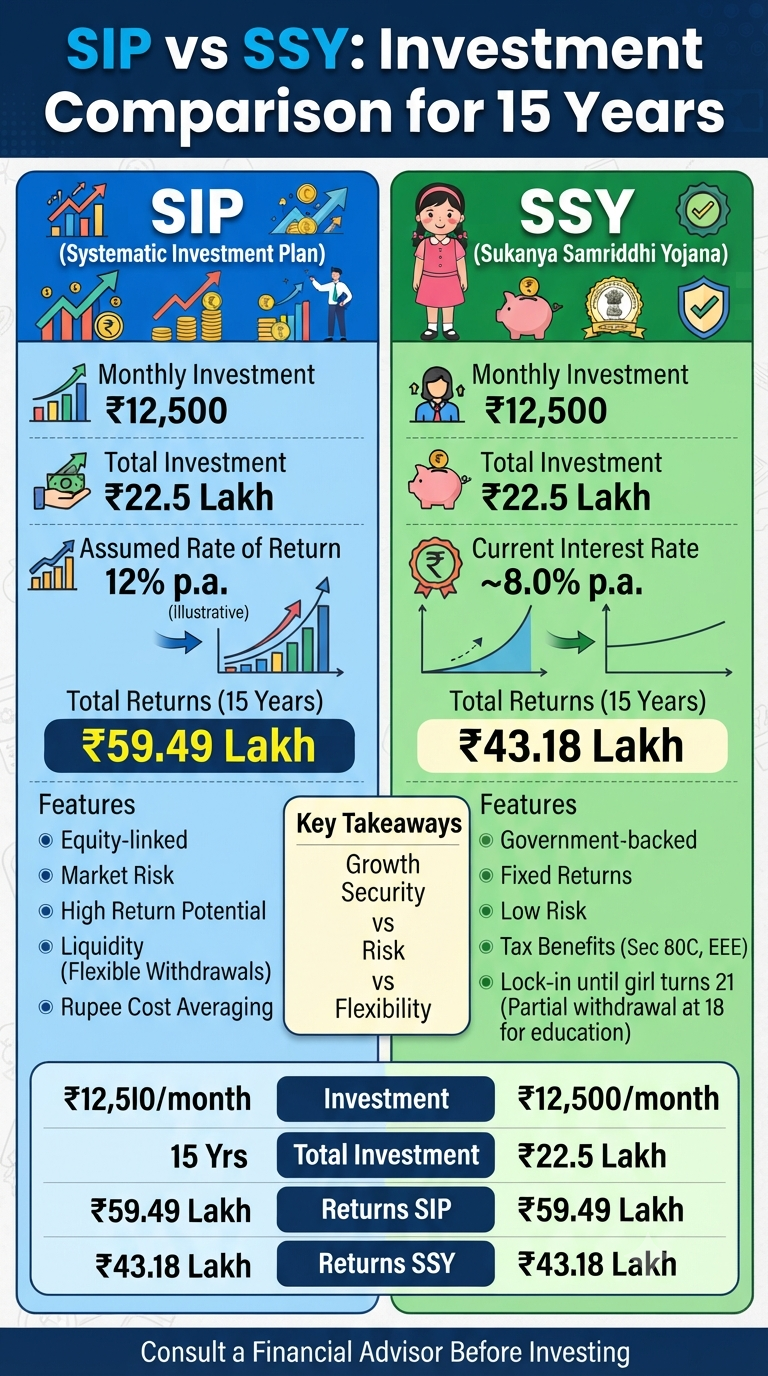

Investing for the future is crucial, and choosing the right investment avenue can make a significant difference in achieving your financial goals. Two popular options in India are the Systematic Investment Plan (SIP) and the Sukanya Samriddhi Yojana (SSY). Let’s delve into a detailed comparison to help you make an informed decision. SIP: Equity-linked and…

Continue Reading SIP vs. SSY: A Detailed Comparison for a Secure Financial Future

We’ve all been there—staring at the bank balance, feeling the familiar squeeze of anxiety, and wondering when things will finally get easier. Often, we treat money problems purely as a logistical issue: we need more income, less debt, or a better budget. But what if the key to financial freedom isn’t just found in a…

Continue Reading From Scarcity to Abundance: 5 Daily Rituals to Unlock True Financial Prosperity

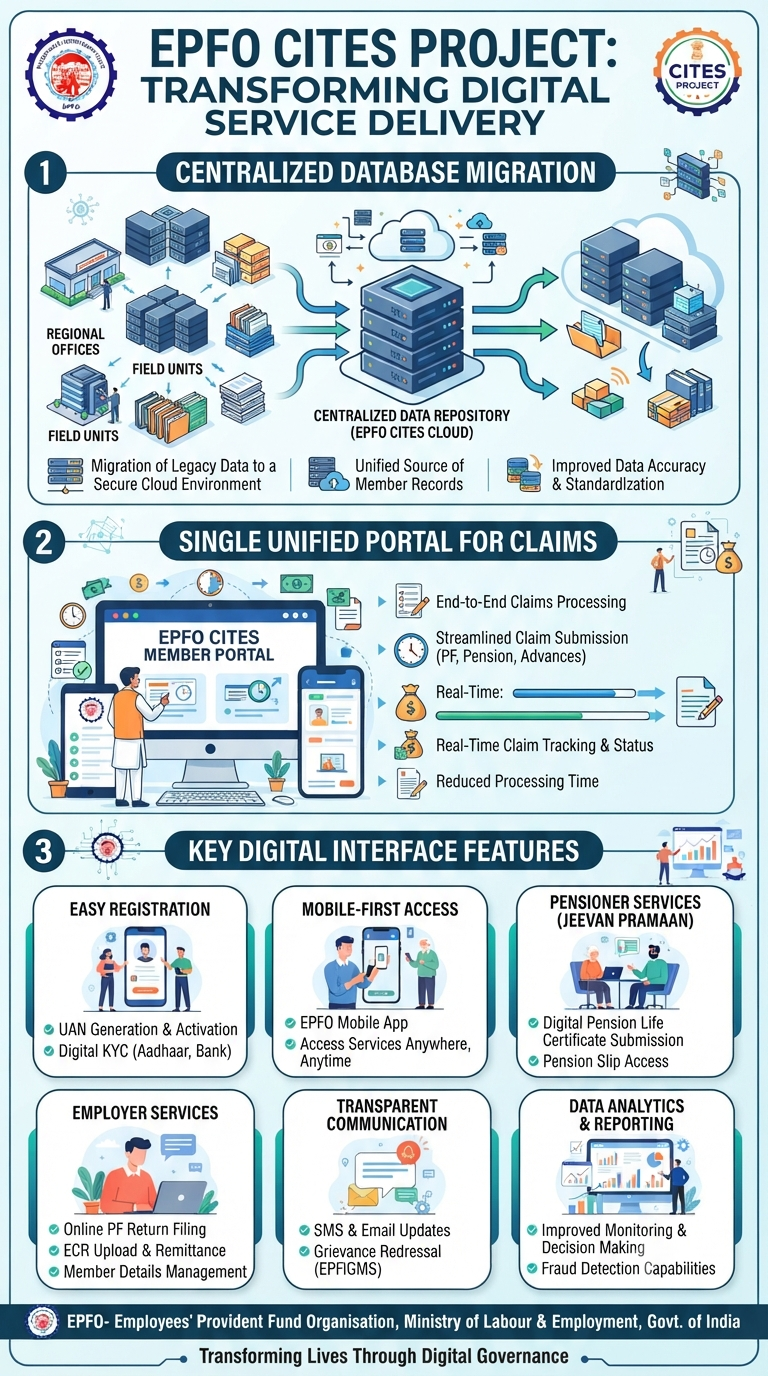

For decades, interacting with the Employees’ Provident Fund Organisation (EPFO) often felt like stepping back in time. Between the mountain of physical paperwork, the anxiety of waiting for transfer approvals, and the occasional need to visit regional offices just to check a status update, the system was ripe for a modern evolution. Well, that evolution…

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.