Dreaming of trading your rent payments for a set of keys to your own front door? Buying a home is an incredible milestone, but it’s also a significant financial commitment. To ensure you’re making the best decision for your future, you need to move beyond the glossy brochures and really dig into the numbers.

That’s where understanding home loan comparison comes in. It’s not just about finding the lowest advertised interest rate; it’s about understanding the full picture of what you’ll be paying, month after month, for years to come.

We’ve compiled a detailed guide for July 2026 to help you make an informed and empowered decision. Let’s break down the key comparison factors, sample offers from real lenders, and the essential terms you need to know.

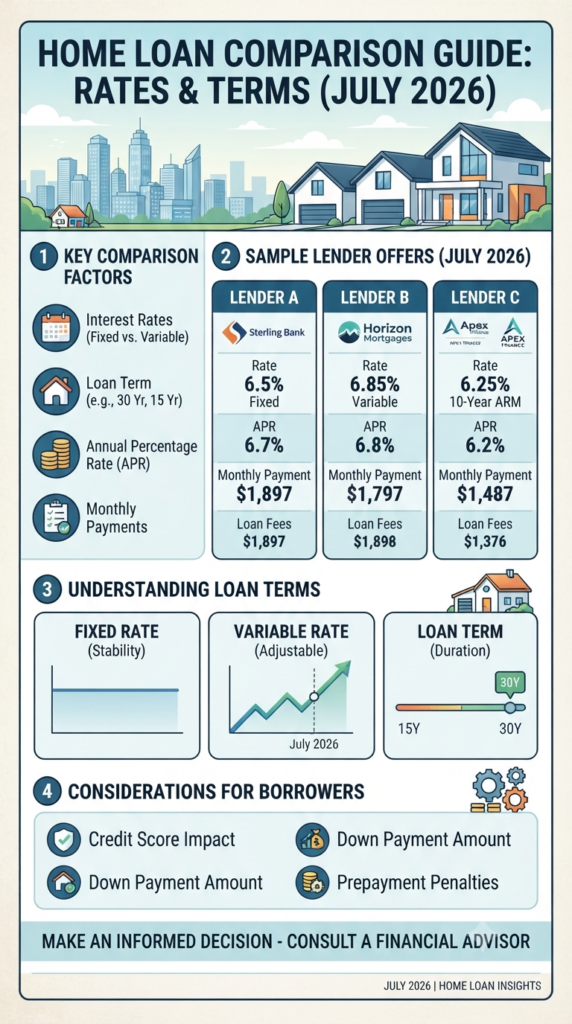

1. The Four Pillars of Comparison: What Really Matters

Before you even look at a specific lender, you need to know what to look for. Don’t get distracted by the noise; focus on these four critical pillars.

- Interest Rates (Fixed vs. Variable): This is the cost of borrowing the money. A Fixed Rate stays the same for the life of the loan, offering predictability and stability. A Variable Rate can change over time, which can be risky if market rates rise.

- Loan Term (e.g., 30-Year, 15-Year): This is the duration of your loan. A longer term (like 30 years) means smaller monthly payments but more interest paid over time. A shorter term (like 15 years) means higher monthly payments but significant savings on interest.

- Annual Percentage Rate (APR): This is the true cost of the loan. It includes the interest rate plus other costs and fees (like origination fees and points) expressed as a yearly rate. The APR is always higher than the interest rate and is the most accurate figure for comparison.

- Monthly Payments: This is the cash you need to have available every single month. While a 30-year loan has a smaller payment, you must ensure it fits comfortably within your budget.

2. Sample Lender Offers: A July 2026 Snapshot

To give you a real-world example, we’ve compared three hypothetical lenders for July 2026. As you can see, each offer presents a different strategy.

| Feature | Lender A: Sterling Bank | Lender B: Horizon Mortgages | Lender C: Apex Finance |

| Rate/Type | 6.5% Fixed | 6.85% Variable | 6.25% 10-Year ARM |

| APR | 6.7% | 6.8% | 6.2% |

| Monthly Payment | $1,897 | $1,797 | $1,487 |

| Loan Fees | $1,897 | $1,898 | $1,376 |

- Sterling Bank offers the highest rate but comes with complete payment stability. If you value predictability above all else, this is a strong contender.

- Horizon Mortgages has a slightly lower rate with the lowest upfront fees, but the variable rate means your payment could increase in the future.

- Apex Finance has the lowest advertised rate (on a 10-year ARM) and the lowest fees, resulting in the smallest monthly payment. However, an Adjustable-Rate Mortgage (ARM) means the rate will reset after 10 years, introducing uncertainty.

Your takeaway: The best offer depends on your personal financial goals and risk tolerance. There is no single “best” lender for everyone.

3. Demystifying Loan Terms: Don’t Sign Until You Understand This

- Fixed Rate (Stability): As shown in our stability graph, your payment remains constant. This is ideal for long-term budgeting and protection against rising interest rates.

- Variable Rate (Adjustable): The graph shows a typical ARM. It starts with a low, attractive rate for a set period (like 10 years), but then the rate fluctuates with the market. Your payment could increase significantly, as indicated by the dotted line and upward arrow.

- Loan Term (Duration): This graphic illustrates the choice between a 15-year and 30-year term. A 30-year loan (labeled 30Y) has a lower payment but spans a longer period. A 15-year loan (15Y) has a higher payment but builds equity faster and saves a massive amount in interest over the life of the loan.

4. Beyond the Numbers: Crucial Considerations for Borrowers

The interest rate isn’t the only factor that influences your ability to get a great loan. Lenders also look at:

- Credit Score Impact: Every lender pulls your credit report, which can temporarily lower your score. Minimize “shopping around” by doing it all within a short, concentrated window (e.g., two weeks).

- Down Payment Amount: A larger down payment (aim for 20% to avoid Private Mortgage Insurance or PMI) reduces the lender’s risk and can often secure you a lower interest rate.

- Discount Points: These are fees you pay upfront at closing to “buy down” your interest rate. This can be a smart move if you plan to stay in the home for a long time.

- Prepayment Penalties: Some loans charge you a fee if you pay off the loan early or make extra principal payments. Avoid these loans if you plan to sell or refinance in the future.

Final Thoughts: Your Next Steps

Comparing home loans can feel overwhelming, but it’s the single most effective way to save thousands of dollars over the life of your mortgage. Don’t rush the process.

- Review your budget: Know exactly what you can afford for a monthly payment.

- Check your credit: Work on improving your score before you apply.

- Get pre-approved: This shows sellers you’re a serious buyer and gives you a firm budget.

- Compare multiple lenders: Don’t just go with your primary bank. Use the framework above to get apples-to-apples comparisons.

Most importantly: Consult a Financial Advisor. This guide is a starting point. A qualified mortgage professional or financial advisor can provide personalized advice based on your unique financial situation, helping you translate these numbers into a clear path to homeownership.

Data and figures are hypothetical for illustration purposes in July 2026. Always consult current market rates and a professional advisor before making financial decisions.

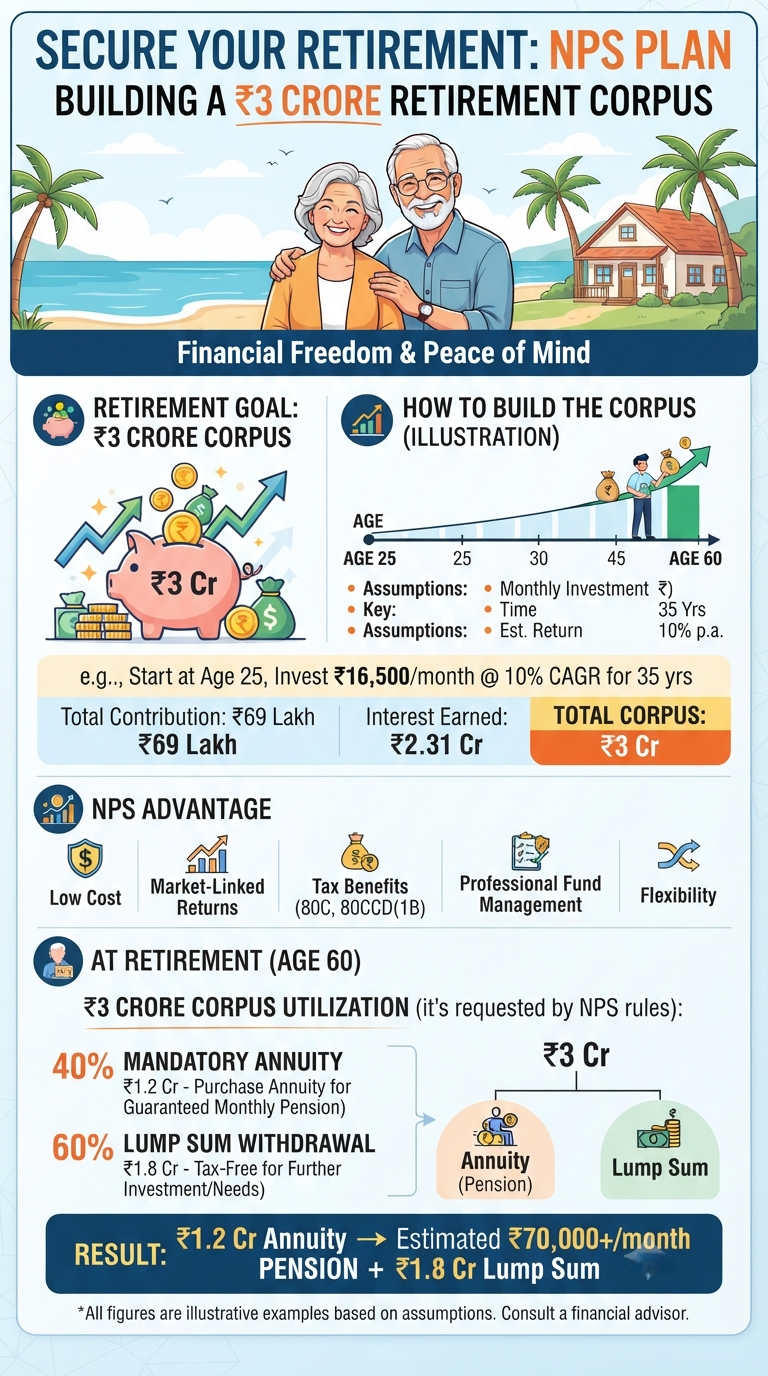

Revolutionizing Your PF Experience: A Deep Dive into EPFO 3.0

Retirement often feels like a distant milestone—something to worry about “later.” But what if you could visualize that “later” right now? Imagine hitting age 60 with a solid ₹3 crore corpus. It’s not just a number on a screen; it’s the key to your financial independence, the bridge to your passions, and the ultimate safety…

Continue Reading Retire Rich: How a ₹3 Crore Corpus Can Power Your Dream Life

You’ve done your homework. You’ve read the financial news, listened to the podcasts, and decided it’s time to secure your financial future. To build a robust, resilient portfolio, you adopt a “more is merrier” strategy, buying into several different mutual funds to ensure you are diversified. But here is a hard truth that many investors…

Continue Reading The Illusion of Choice: Are You Trapped in the Mutual Fund Overlap Web?

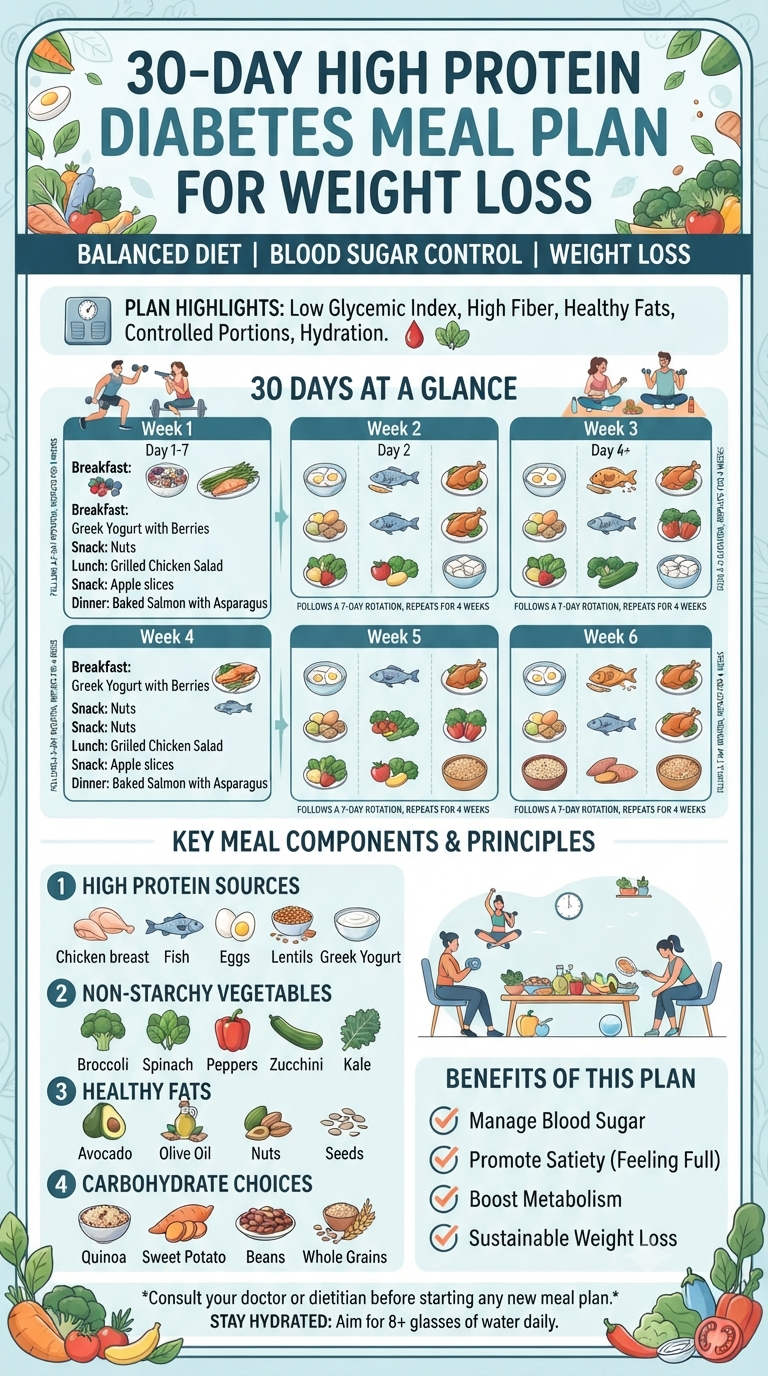

When it comes to health, we’re often bombarded with quick fixes and extreme restrictions. But what if the secret to managing blood sugar and achieving weight loss wasn’t about deprivation, but about intentional, high-protein nourishment? If you’ve been looking for a way to reset your habits without feeling constantly hungry, a high-protein, diabetes-friendly approach might…

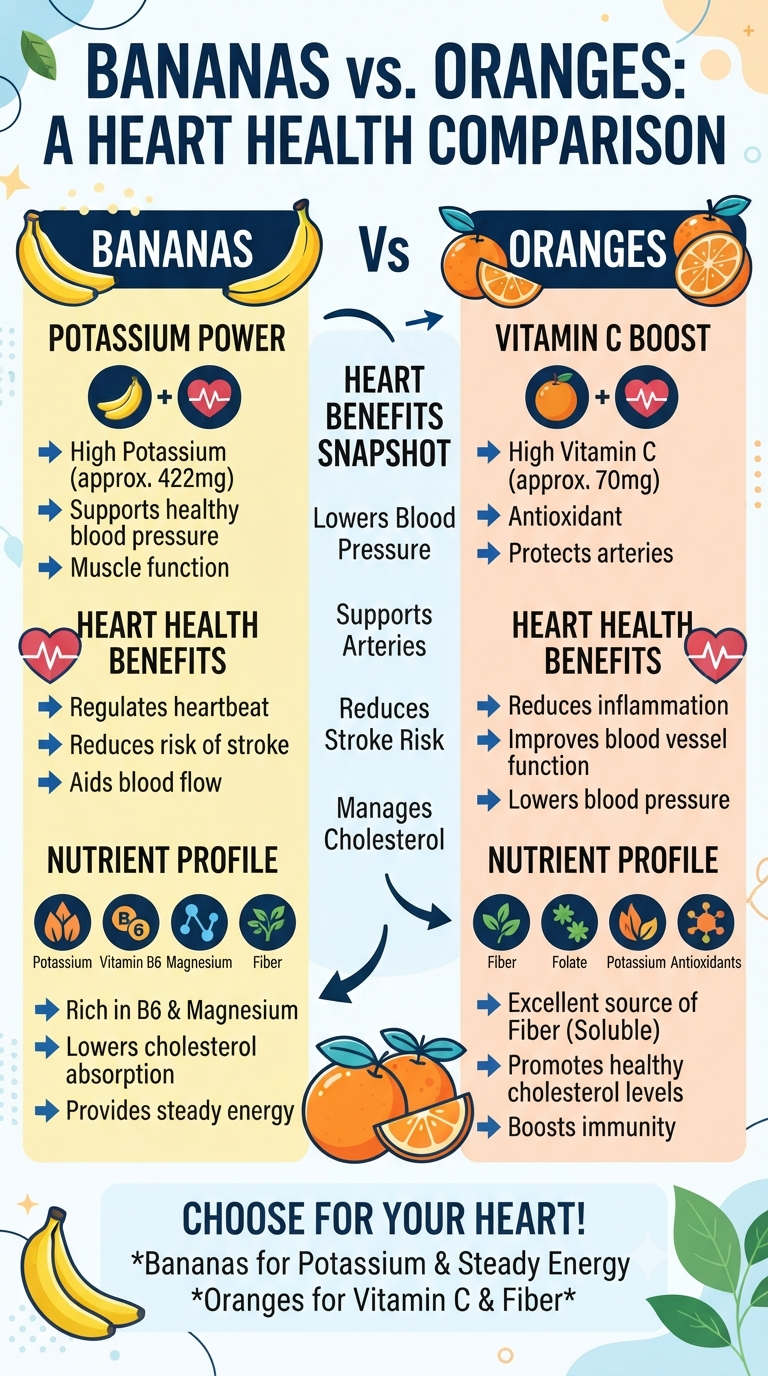

When you’re staring at the fruit bowl wondering which snack will do your heart the most good, it’s easy to feel torn. Do you reach for the convenient banana or the zesty, refreshing orange? Both are nutritional powerhouses, but they bring different strengths to your cardiovascular game. Let’s break down how these two favorites measure…

Continue Reading Heart-Healthy Snacking: The Battle of the Fruits

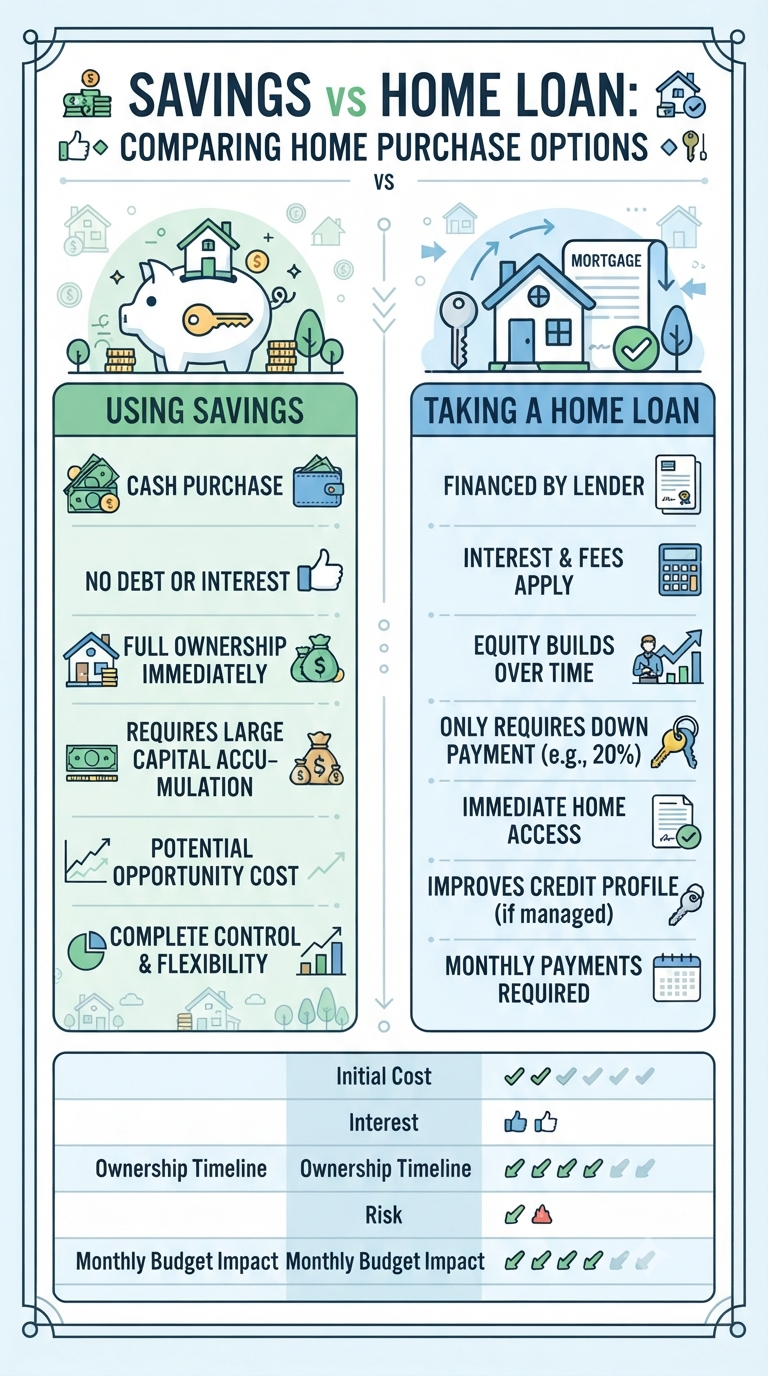

Buying a home is one of life’s biggest milestones. For most people, it’s not just a house—it’s a long-term investment in their future and a place to build a life. But with such a massive price tag, a fundamental question arises: Should I save up and pay cash, or should I take out a home…

Continue Reading The Ultimate Showdown: Is it Better to Buy Your Dream Home with Cash or a Mortgage?

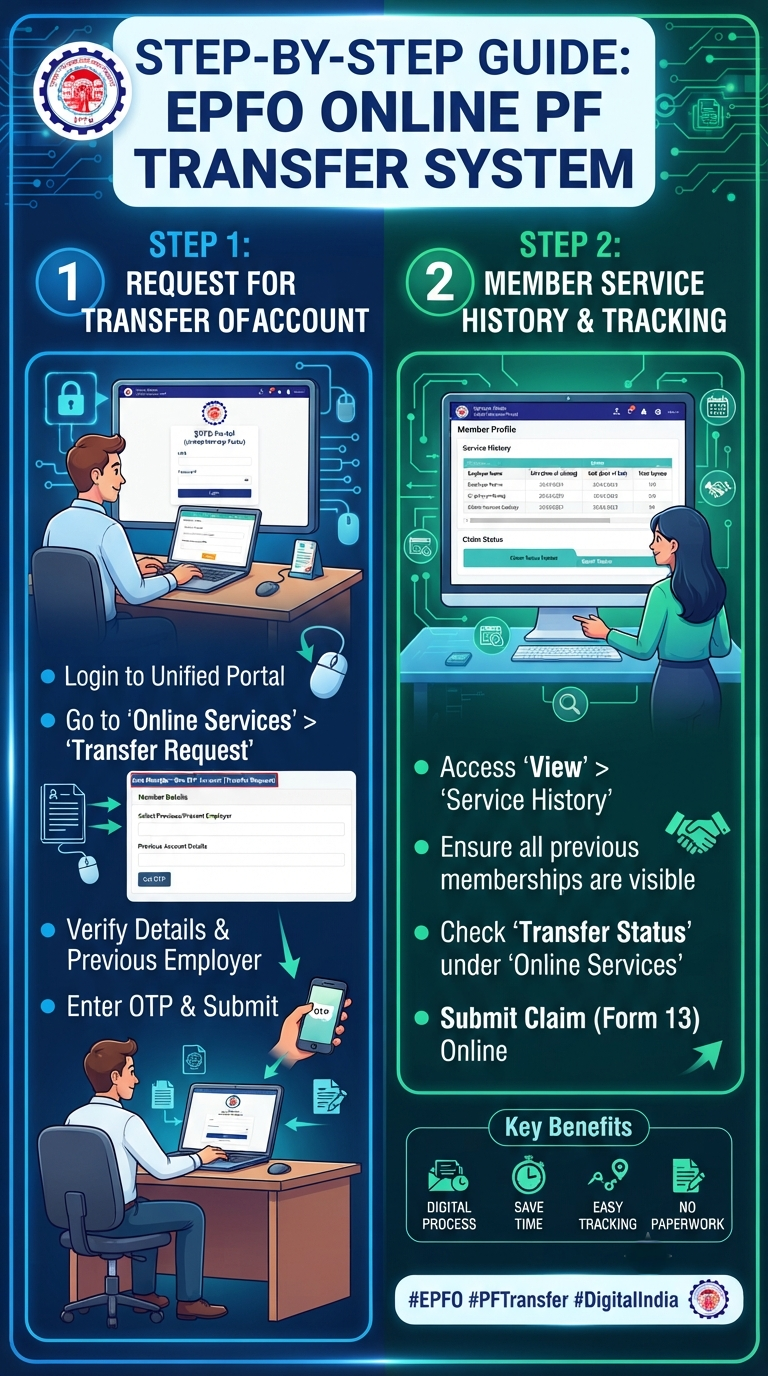

Let’s be honest: tracking down old Provident Fund (PF) accounts from past jobs feels like a chore no one wants to tackle. Between the mountain of forms, the fear of losing service history, and the sheer time it takes, many of us just leave our old accounts sitting idle. But what if you could clean…

Continue Reading Say Goodbye to Paperwork: How to Consolidate Your EPF Accounts Online

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.