Planning for retirement can often feel like trying to solve a complex puzzle. With so many financial instruments available, it is easy to feel overwhelmed by the acronyms. If you are looking to secure your golden years, you have likely come across the big three: EPF, PPF, and NPS.

Each of these serves a different purpose, and understanding their nuances is the key to building a robust retirement corpus. Let’s break them down in plain English.

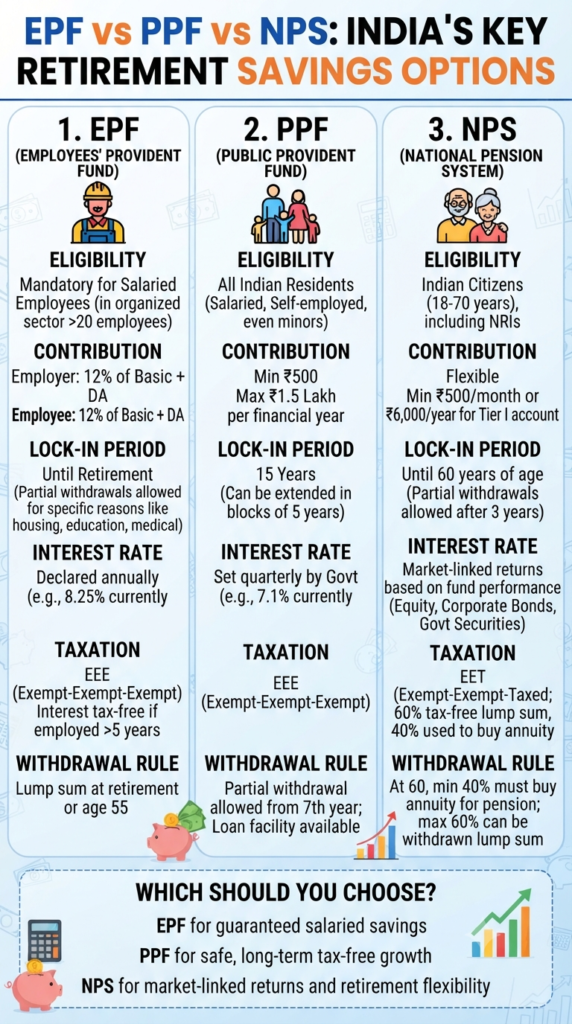

1. Employees’ Provident Fund (EPF): The Salaried Employee’s Backbone

If you work in an organized sector with more than 20 employees, EPF is likely already a part of your life. It is a mandatory savings scheme where both you and your employer contribute 12% of your basic salary and dearness allowance.

- Why it shines: It is a low-risk, guaranteed return instrument. The government declares the interest rate annually, which is typically quite attractive (currently 8.25%).

- The Taxation Perk: It follows the EEE (Exempt-Exempt-Exempt) model, meaning your contributions, the interest earned, and the final maturity amount are all tax-free, provided you have been employed for more than five years.

- Best for: Those who want a “set it and forget it” approach with guaranteed growth.

2. Public Provident Fund (PPF): The Safe Haven for Everyone

PPF is a favorite among conservative investors, and for good reason. It is open to all Indian residents, including the self-employed.

- Why it shines: It is incredibly safe as it is backed by the government. The interest rate is set quarterly (currently 7.1%).

- The Taxation Perk: Like EPF, it enjoys the EEE status, making it one of the most tax-efficient long-term investments in India.

- The Trade-off: It comes with a 15-year lock-in period, though partial withdrawals and loans are permitted after a certain period.

- Best for: Those looking for a completely safe, long-term, tax-free growth vehicle.

3. National Pension System (NPS): The Flexible Market Player

NPS is designed to provide you with a regular pension after retirement. It is a market-linked product, meaning your returns depend on how the underlying assets—equity, corporate bonds, and government securities—perform.

- Why it shines: It offers the most flexibility. You can decide how much you want to invest (as little as ₹500/month or ₹6,000/year for a Tier I account) and who manages your funds.

- The Taxation Perk: It follows the EET (Exempt-Exempt-Taxed) model. While your contributions are tax-deductible, a portion of the maturity corpus is taxed. However, you must use at least 40% of the corpus to buy an annuity for a monthly pension.

- Best for: Individuals who are comfortable with market fluctuations and want to maximize potential returns for a flexible retirement lifestyle.

So, which one should you choose?

There isn’t a “one-size-fits-all” answer, but here is a simple guide to help you decide:

- Stick with EPF if you are a salaried professional seeking a guaranteed, employer-matched safety net.

- Opt for PPF if you want to build a secure, tax-free corpus with absolute peace of mind over a 15-year horizon.

- Choose NPS if you are willing to embrace market-linked growth to potentially build a larger corpus and prefer having more control over your pension planning.

Pro Tip: Many savvy investors do not choose just one. They use a combination of these to balance safety, liquidity, and growth, creating a diversified retirement portfolio that works as hard as they do!

Disclaimer: Financial regulations and interest rates are subject to change. Always consult with a certified financial planner before making significant investment decisions.

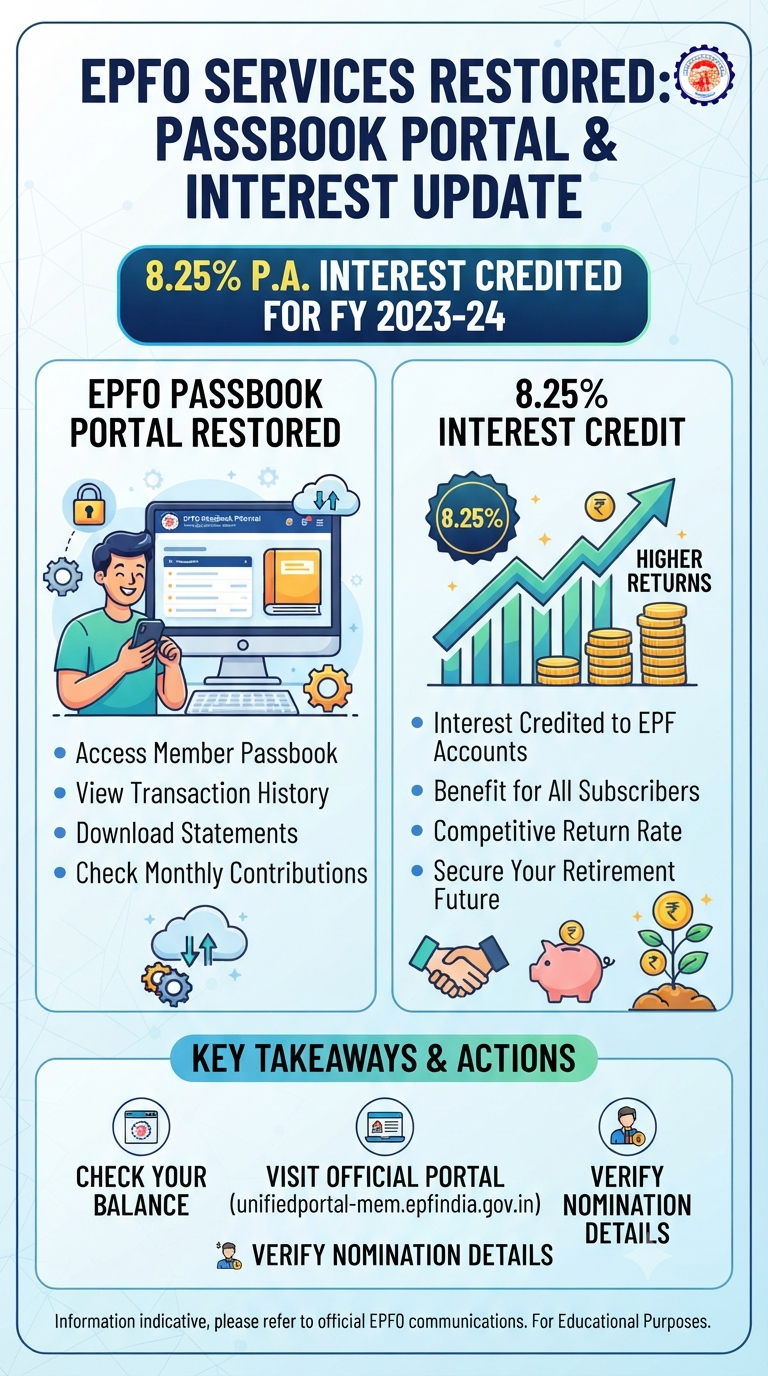

A Game-Changer for Employees: 10 Massive Upgrades to the EPFO System

For millions of employees across India, the Employees’ Provident Fund (EPF) is more than just a mandatory deduction—it’s the bedrock of a secure retirement. So, when the EPFO passbook portal goes down for maintenance, it’s understandable that anxiety levels spike. After all, your passbook is the window into your financial future. The good news? The…

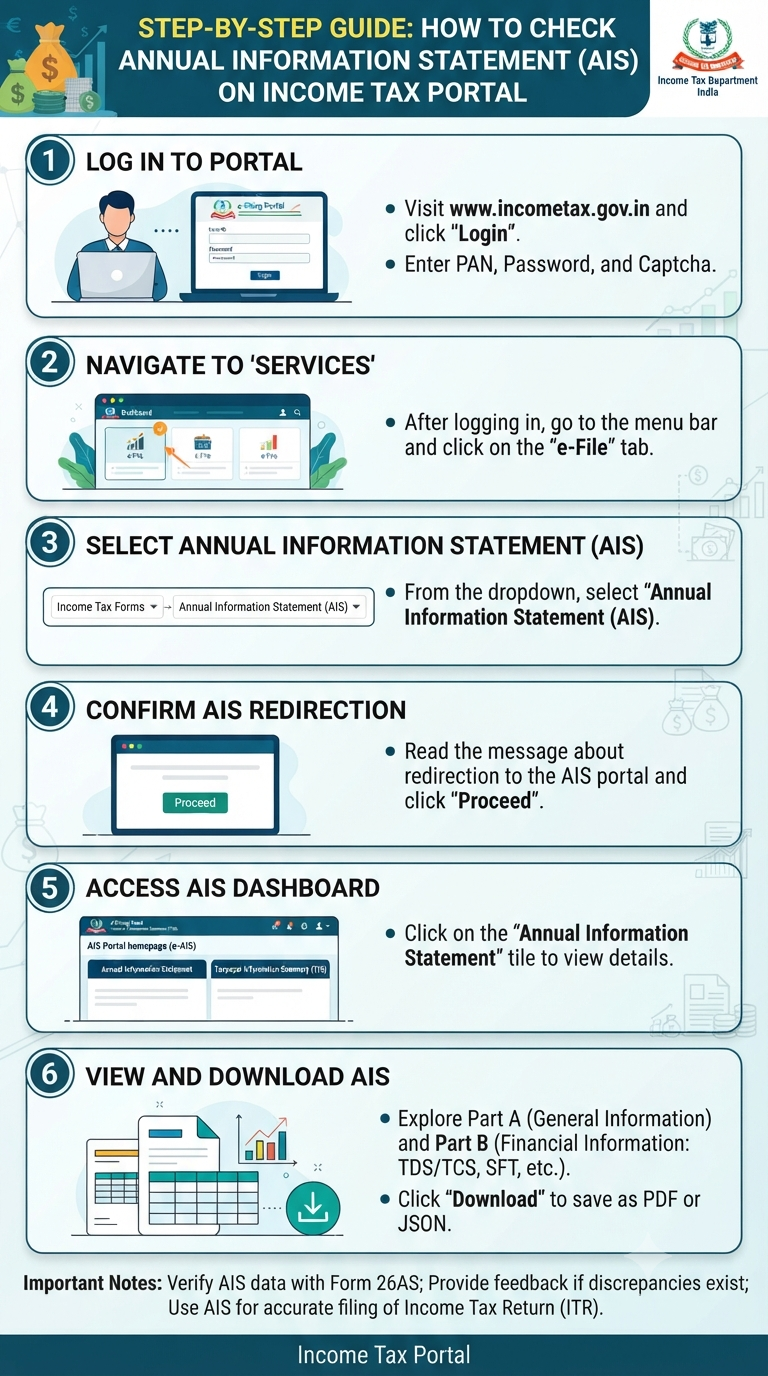

Filing your Income Tax Return (ITR) is one of those annual financial chores that often feels daunting. We scramble for Form 16s, look for investment proofs, and hope we haven’t missed anything. But what if there was a “cheat sheet” that held nearly all the information the Income Tax Department already has about your financial…

Continue Reading Why Your Annual Information Statement (AIS) is Your Best Friend Before Filing ITR

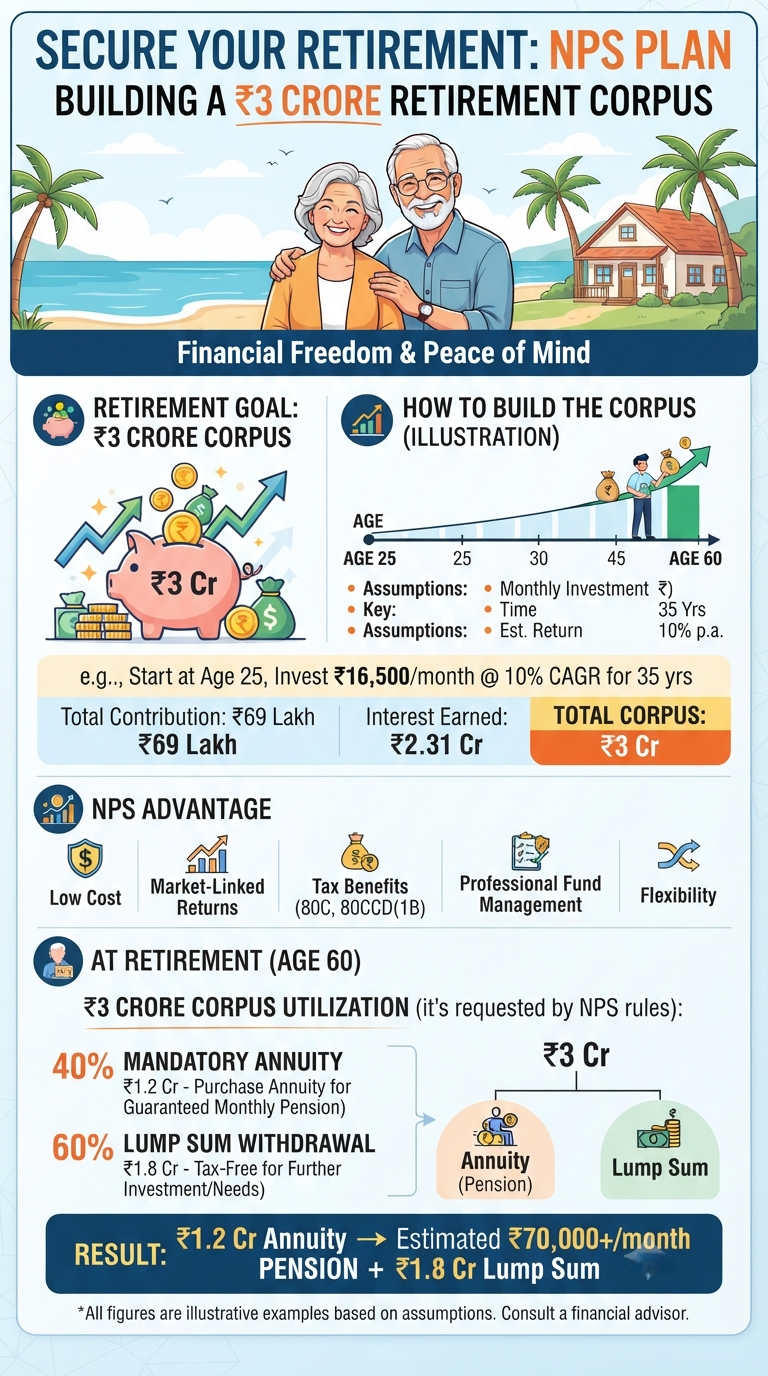

Retirement often feels like a distant milestone—something to worry about “later.” But what if you could visualize that “later” right now? Imagine hitting age 60 with a solid ₹3 crore corpus. It’s not just a number on a screen; it’s the key to your financial independence, the bridge to your passions, and the ultimate safety…

Continue Reading Retire Rich: How a ₹3 Crore Corpus Can Power Your Dream Life

You’ve done your homework. You’ve read the financial news, listened to the podcasts, and decided it’s time to secure your financial future. To build a robust, resilient portfolio, you adopt a “more is merrier” strategy, buying into several different mutual funds to ensure you are diversified. But here is a hard truth that many investors…

Continue Reading The Illusion of Choice: Are You Trapped in the Mutual Fund Overlap Web?

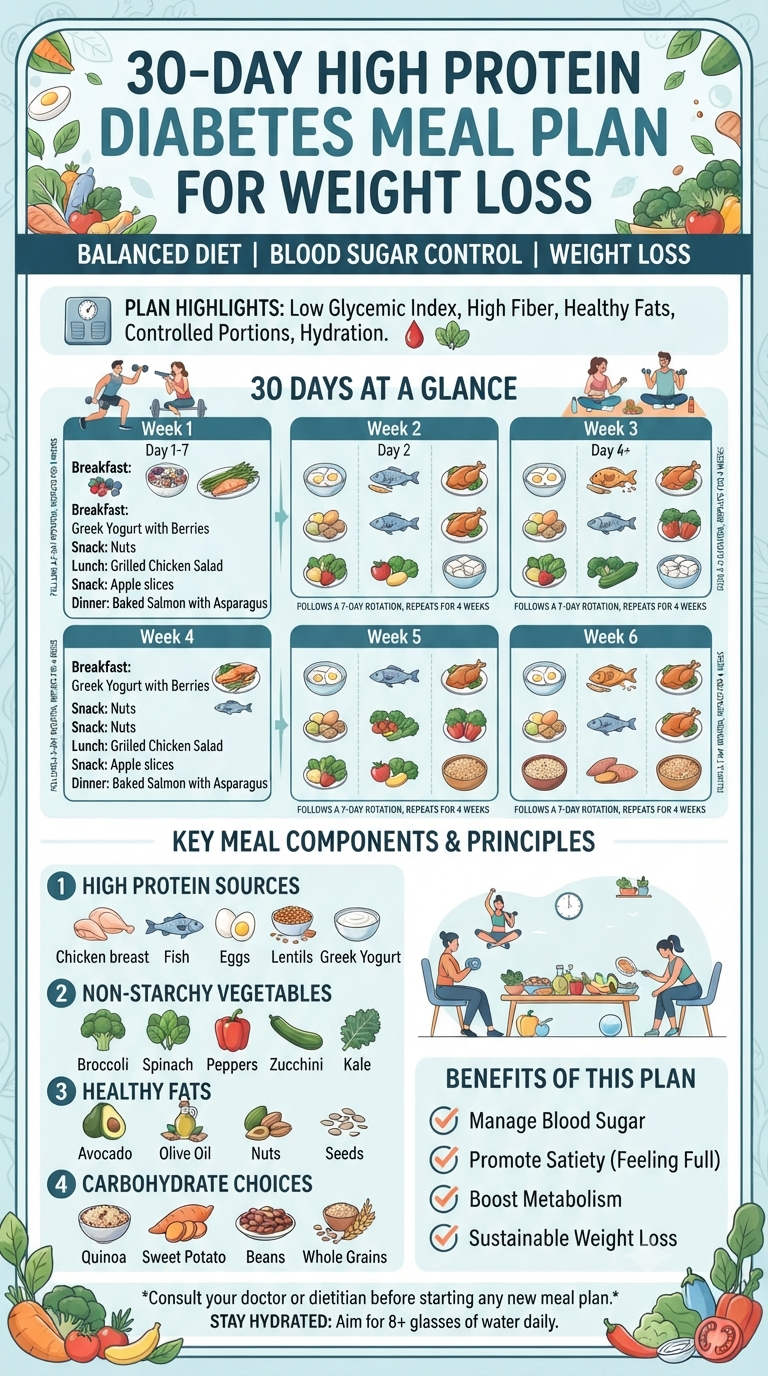

When it comes to health, we’re often bombarded with quick fixes and extreme restrictions. But what if the secret to managing blood sugar and achieving weight loss wasn’t about deprivation, but about intentional, high-protein nourishment? If you’ve been looking for a way to reset your habits without feeling constantly hungry, a high-protein, diabetes-friendly approach might…

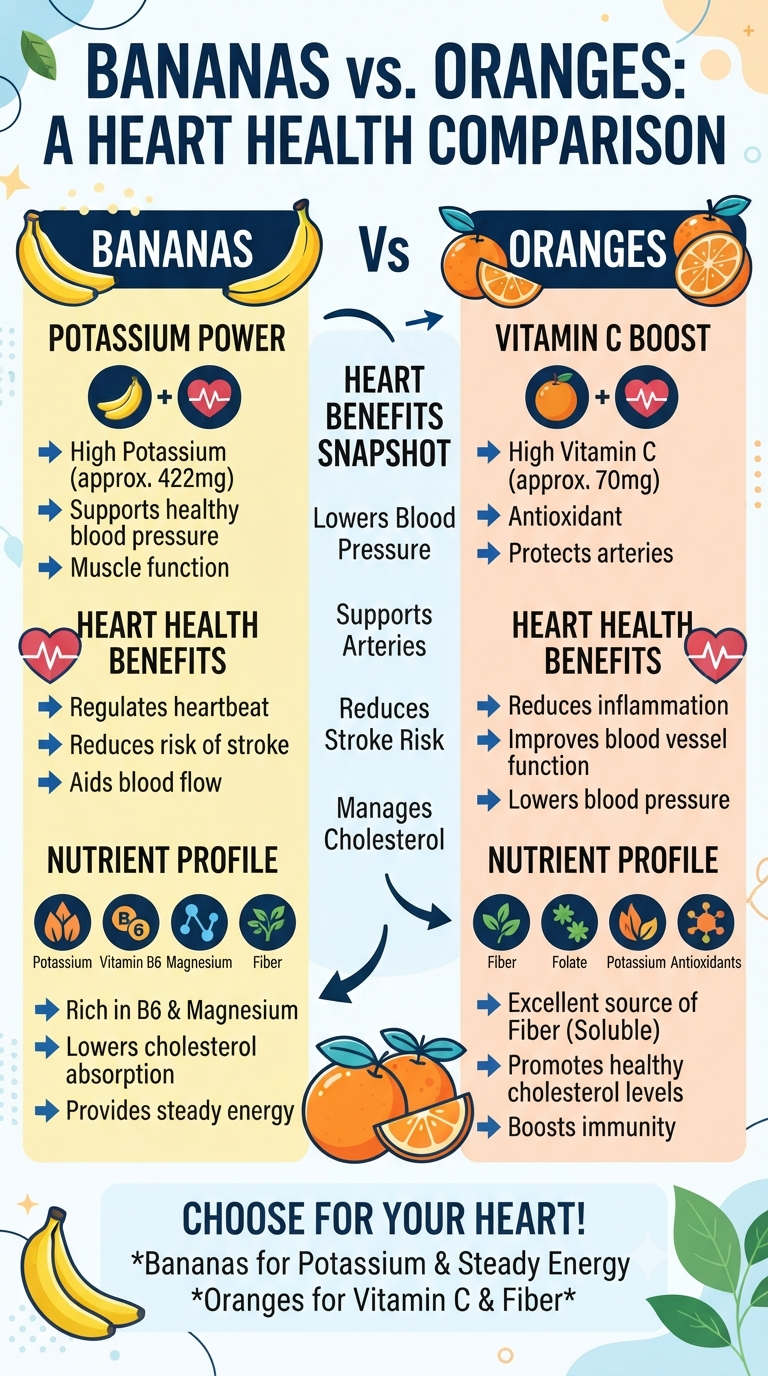

When you’re staring at the fruit bowl wondering which snack will do your heart the most good, it’s easy to feel torn. Do you reach for the convenient banana or the zesty, refreshing orange? Both are nutritional powerhouses, but they bring different strengths to your cardiovascular game. Let’s break down how these two favorites measure…

Continue Reading Heart-Healthy Snacking: The Battle of the Fruits

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.