We all love to give back to our families. Whether it’s a surprise gift for a birthday or a gesture of appreciation, the intent is usually rooted in love. But what if that gift could also be a strategic move that saves your family thousands in taxes?

When it comes to gifting shares, it turns out that “who” you gift to is far more important than “what” you gift. While gifting shares to your inner circle is legally tax-free, the aftermath—the tax on dividends and capital gains—varies wildly depending on whether you gift to your parents or your spouse.

If you’re looking to optimize your family’s tax liability, here is the breakdown of why one strategy is a masterstroke and the other might just be a tax trap.

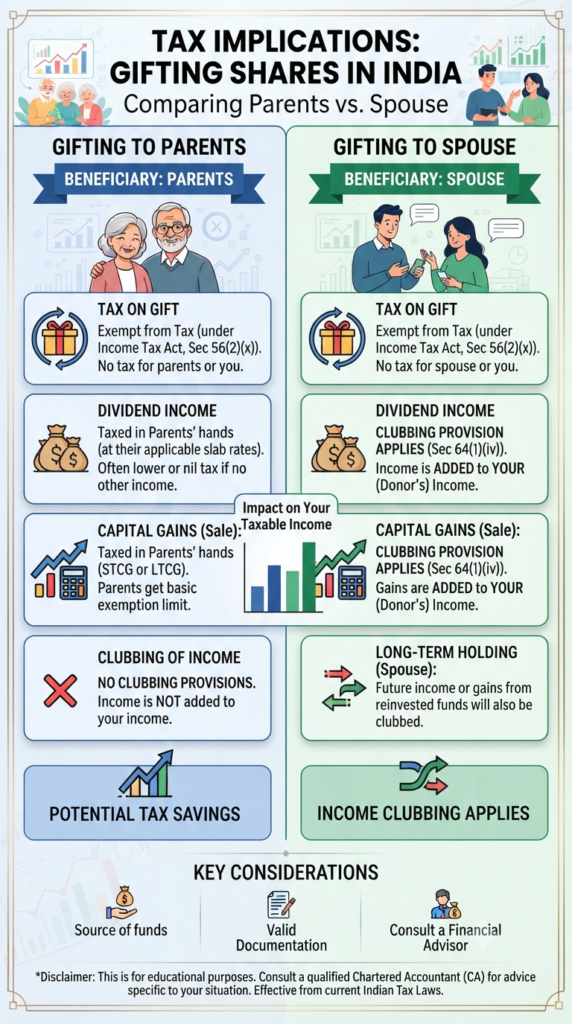

1. The Good News: The Gift Itself is Tax-Free

First, let’s clear the air. Under Section 56(2)(x) of the Income Tax Act, transferring shares to “specified relatives”—which includes your parents, spouse, children, and siblings—is completely exempt from gift tax. You don’t need to worry about a tax bill hitting your door the moment the shares move from your Demat account to theirs.

2. Gifting to Parents: The Smart Move

This is where the magic happens. Many parents, especially those who are retired, fall into a lower income tax slab than their working children.

Because parents are not covered under the “clubbing of income” rules, any income generated from those gifted shares—whether it’s dividends or capital gains when they eventually sell—is taxed according to their tax slab.

The Math Simplified:

Imagine you are in a 30% tax bracket. If you sell shares and make a profit, you pay a significant chunk in taxes. If you gift those same shares to your retired father, and he sells them, his total income may still fall below the taxable limit (or into a much lower slab). The result? You’ve effectively moved that tax liability from a high-tax environment to a zero-or-low-tax environment.

3. Gifting to a Spouse: The “Tax Trap”

It’s a common misconception that gifting shares to a spouse is a great way to split income. Unfortunately, the Income Tax Act has a specific provision—Section 64—designed to stop this.

This section enforces “clubbing of income.” If you gift assets to your spouse, the law assumes you are doing it simply to avoid taxes. Therefore, any dividend or capital gain earned on those shares is “clubbed” back into your total income and taxed at your applicable slab rate.

In short: You lose control of the assets, but you still carry the tax burden. It’s almost always a losing game from a tax-planning perspective, save for a few extremely rare exceptions that usually require a legal separation or court-approved settlements.

4. Two Golden Rules You Cannot Ignore

Regardless of who you choose to gift to, two crucial rules will always apply:

- Your Cost is Their Cost: The recipient doesn’t get a “stepped-up” cost basis. If you bought shares at ₹100 and they are now worth ₹500, the recipient’s cost of acquisition remains ₹100.

- The Clock Keeps Ticking: The holding period doesn’t reset. If you held the shares for two years and then gift them, the recipient inherits that two-year tenure. This is great for calculating Long Term Capital Gains (LTCG), as it helps the recipient meet the holding requirements faster.

The Bottom Line: Before You Click “Transfer”

Gifting shares can be a sophisticated way to manage family wealth, but it is not a DIY project to be taken lightly.

Your Checklist:

- Draft a Gift Deed: Don’t just rely on a verbal agreement. A notarized gift deed is the gold standard for documentation.

- Keep Records: Ensure you have the Demat transfer proofs and proof of relationship ready.

- Consult a Pro: Every family’s financial situation is unique. Before moving large blocks of equity, spend an hour with a Chartered Accountant (CA). They can help you navigate the edge cases and ensure your good intentions don’t lead to a surprise notice from the tax department.

Disclaimer: This article is for informational purposes only and does not constitute professional tax or financial advice. Tax laws in India are subject to change; always consult with a qualified professional before executing tax-planning strategies.

Sip Your Way to Comfort: 5 Simple After-Dinner Drinks to Ease Digestion

If you are looking for a safe, government-backed harbor for your hard-earned money, the Senior Citizens Savings Scheme (SCSS) and the Post Office Monthly Income Scheme (MIS) are likely at the top of your list. They offer peace of mind, stability, and the reliability of a sovereign guarantee. But when it comes to maximizing your…

Let’s be honest. Most of us know EPF stands for Employees’ Provident Fund, and we know a chunk of our salary goes into it every month. But how many of us actually know exactly how much is in that corpus, or—more importantly—if that promised 8.25% interest has hit our account yet? If you’ve been meaning…

Continue Reading Checkmate Your PF Status: 4 Simple Ways to View Your EPF Balance Right Now

For any salaried professional, that email from HR announcing a salary hike—or better yet, a change that boosts your monthly take-home pay—is usually a cause for celebration. We all love a little extra breathing room in our monthly budget to cover rising costs, splurge on a vacation, or simply enjoy a higher standard of living…

Continue Reading More Cash Today or Millions Tomorrow? Decoding the Proposed EPF Change

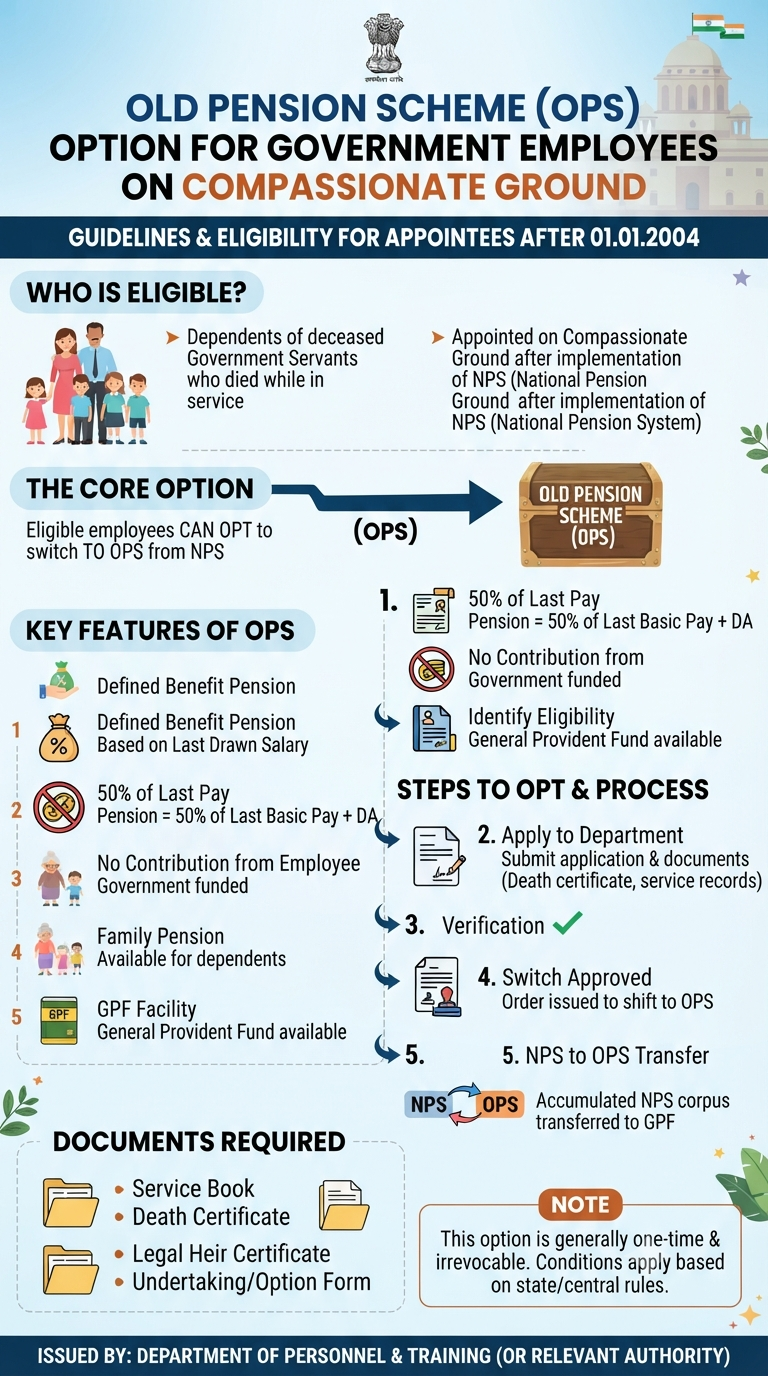

For thousands of government employees who entered service through the compassion of a family-related appointment, the transition into their careers was often marked by a bureaucratic “what-if.” Many had applied for their positions before the cutoff of December 2003, only to join service after the National Pension System (NPS) had already taken hold in January…

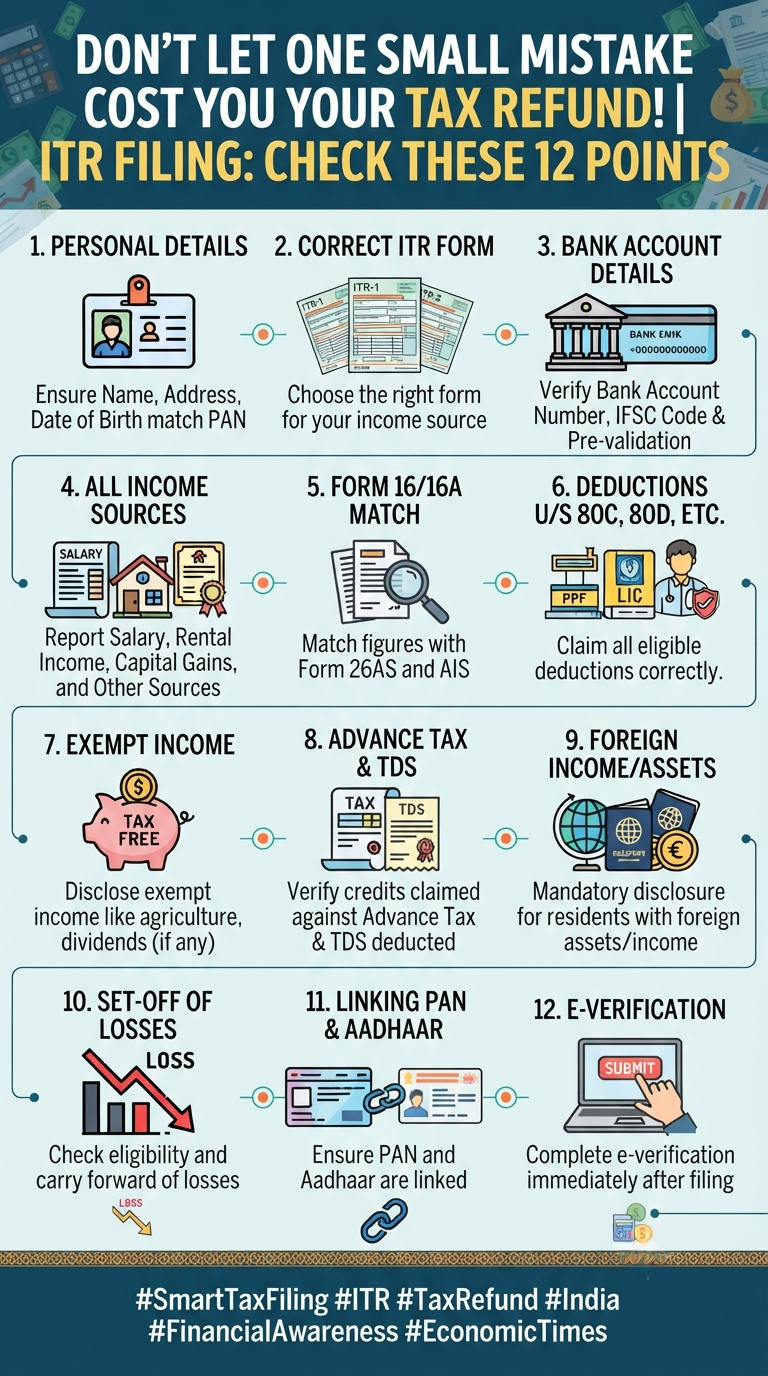

Filing your Income Tax Return (ITR) can often feel like a chore—a necessary evil that we rush through just to get it off our to-do list. But here is the reality: a single typo or a missed detail can be the difference between getting a swift tax refund and getting stuck in a bureaucratic nightmare.…

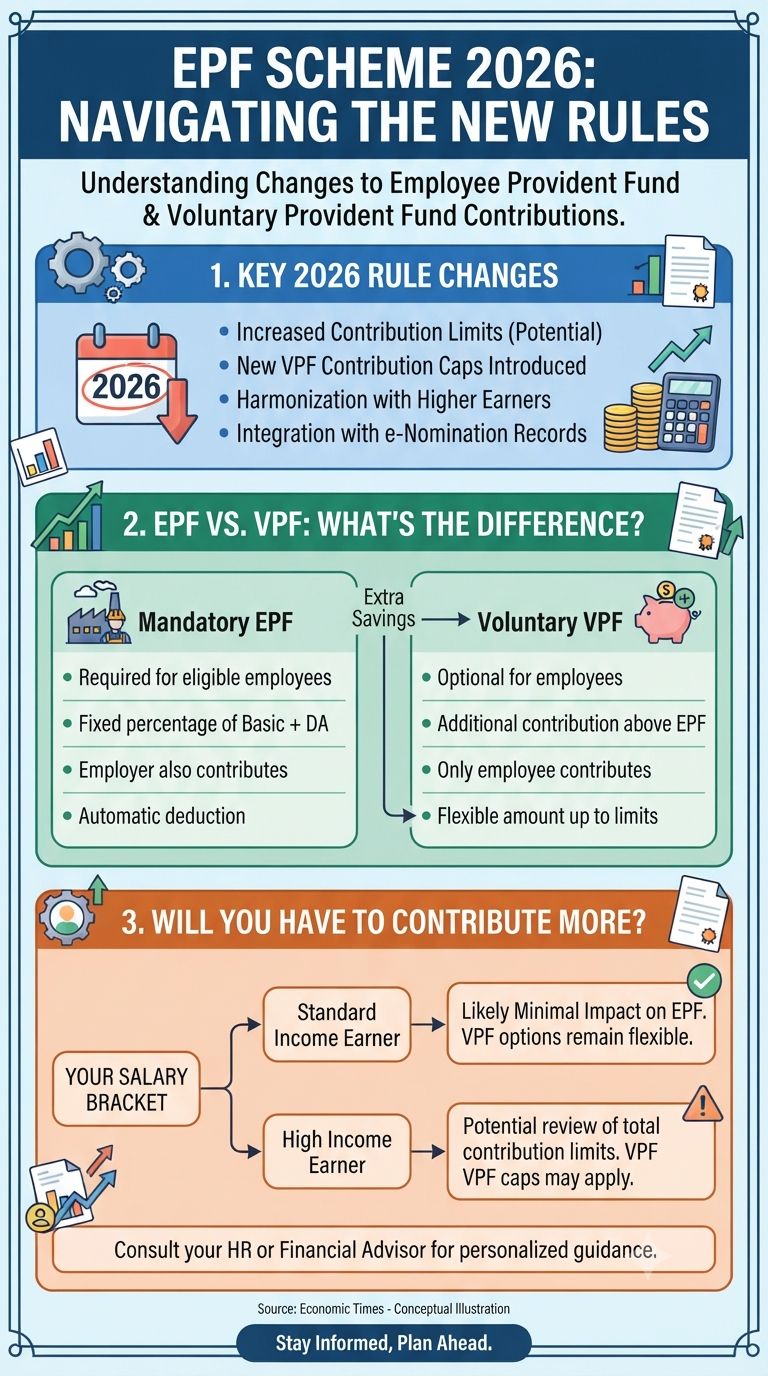

If you’ve been scrolling through financial news lately, you’ve probably noticed the buzz around the “EPF Scheme 2026” updates. It’s the kind of topic that sounds dry until you realize it directly affects how much of your hard-earned money stays in your pocket today versus how much gets tucked away for your future. With the…

Continue Reading EPF Scheme 2026: What the New Rules Actually Mean for Your Paycheck

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.