Retirement should be a time for relaxation, hobbies, and spending time with loved ones—not worrying about market fluctuations or where the next monthly cheque is coming from. For many senior citizens in India, finding a safe, government-backed investment that offers reliable, fixed returns is the cornerstone of a peaceful retirement.

Enter the Senior Citizens’ Savings Scheme (SCSS). With interest rates remaining competitive, it continues to be a favorite among retirees looking for stability. But have you ever wondered exactly how much you need to set aside to generate a specific income?

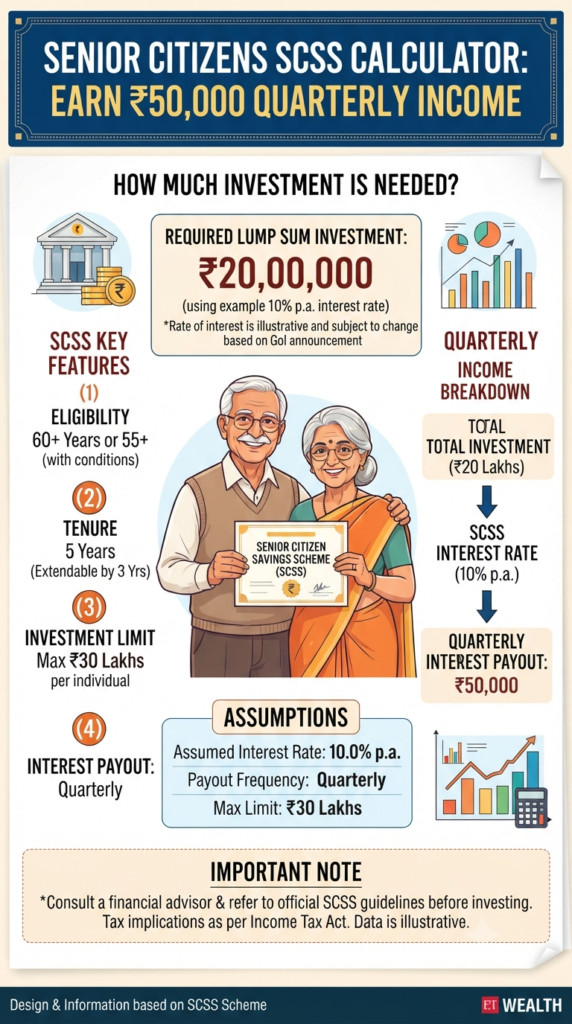

If you are aiming for a steady ₹50,000 every quarter, here is a simple breakdown of how the math works.

The Math Behind the Goal

To receive ₹50,000 every three months, you are essentially looking for an annual interest income of ₹2,00,000 (₹50,000 × 4).

Based on the current interest rate of 8.2% per annum for the July–September 2026 quarter, you would need to invest approximately ₹24.40 lakh into an SCSS account.

Note: This calculation is based on illustrative interest rates; actual earnings may vary based on government announcements and applicable tax laws.

Why SCSS Remains a Top Choice

The SCSS is more than just a savings account; it is designed specifically for those aged 60 and above (or 55+ under certain conditions). Here is why it remains a pillar of retirement portfolios:

- Government-Backed Security: It is a low-risk, government-backed small savings scheme.

- Predictable Payouts: Interest is paid out quarterly, providing a regular cash flow that helps manage day-to-day expenses.

- Attractive Rates: It currently offers one of the highest interest rates among small savings schemes.

- Flexible Limits: You can invest up to a maximum of ₹30 lakh per individual. If both spouses are eligible, you can even open separate accounts, doubling the potential investment limit.

Key Considerations Before You Invest

- Tenure: The scheme comes with a 5-year lock-in period, though it can be extended for another 3 years.

- Documentation: Ensure you have your Aadhaar card ready, as it is mandatory to open an SCSS account.

- Tax Implications: Remember that while this provides a great income stream, the interest earned is subject to tax as per the Income Tax Act.

- Financial Guidance: While tools and calculators are excellent for planning, it is always a wise move to consult with a financial advisor to ensure your investment strategy aligns perfectly with your overall retirement goals.

Planning for your future is the best gift you can give yourself. By leveraging secure, fixed-income options like the SCSS, you can focus less on the numbers and more on enjoying your well-earned retirement.

Disclaimer: The information above is for educational purposes and is based on current interest rates. Please consult with a financial advisor and refer to official government guidelines before making any investment decisions.

Borrowers, Take Note: What HDFC Bank’s Latest Rate Update Means for You

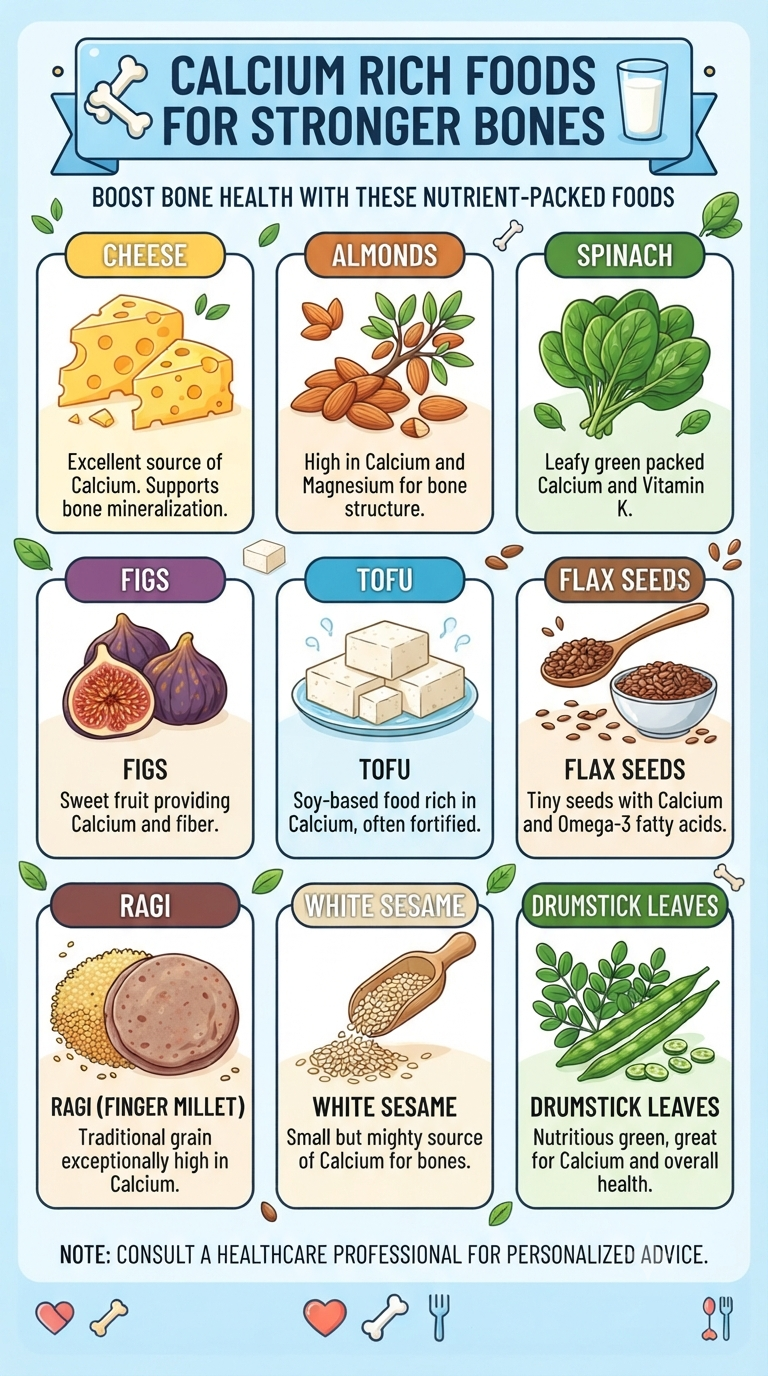

We often think of bone health as something to worry about only in our later years, but the truth is that your bones are constantly changing. Think of them like a savings account; what you “deposit” into your diet today determines how strong your skeletal structure will be tomorrow. Calcium is the cornerstone of that…

Continue Reading Unlock Stronger Bones: The Top Calcium-Rich Foods You Should Add to Your Diet Today

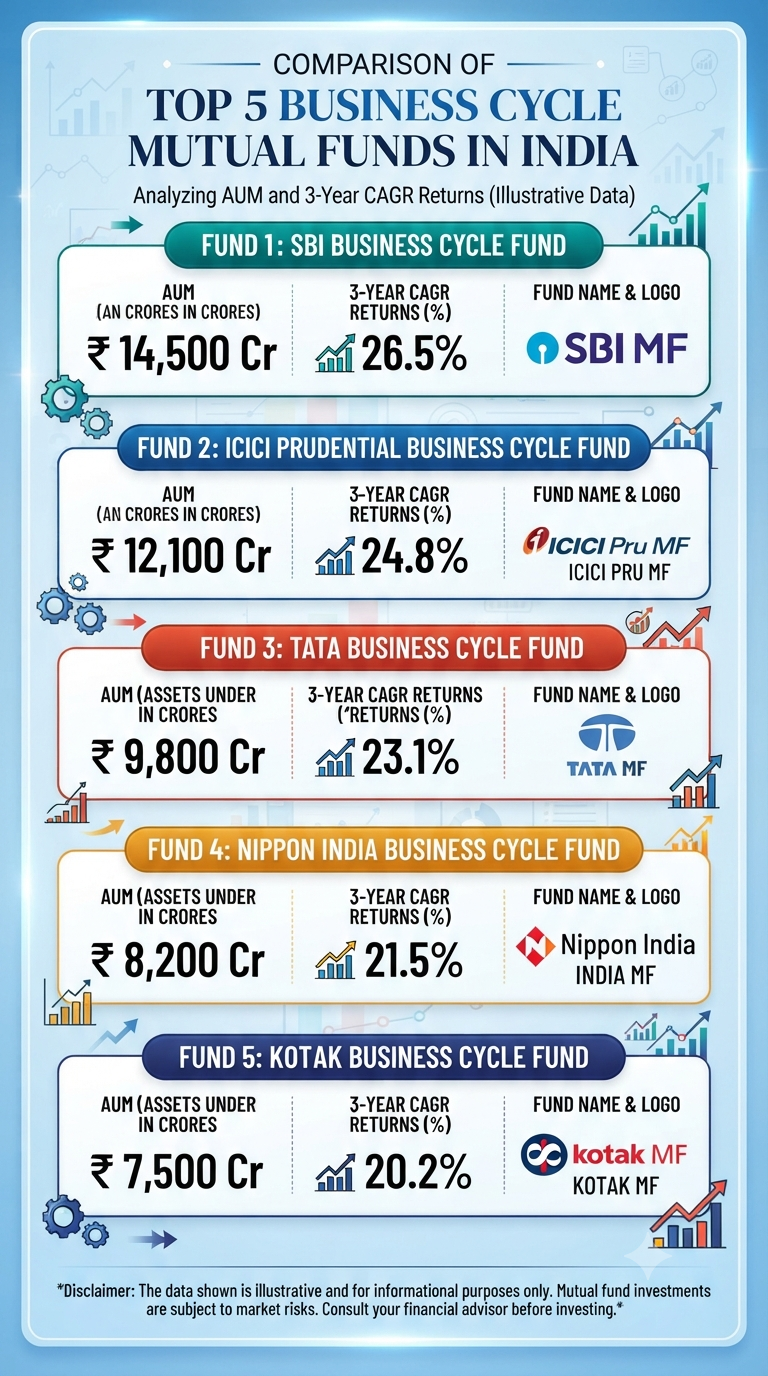

The Indian economy is a vibrant, ever-shifting landscape. Just as the seasons change, so do the fortunes of different industries. This dynamic is known as the business cycle, a natural ebb and flow of economic expansion and contraction. For investors, understanding these cycles isn’t just academic; it’s a crucial skill for identifying opportunities and managing…

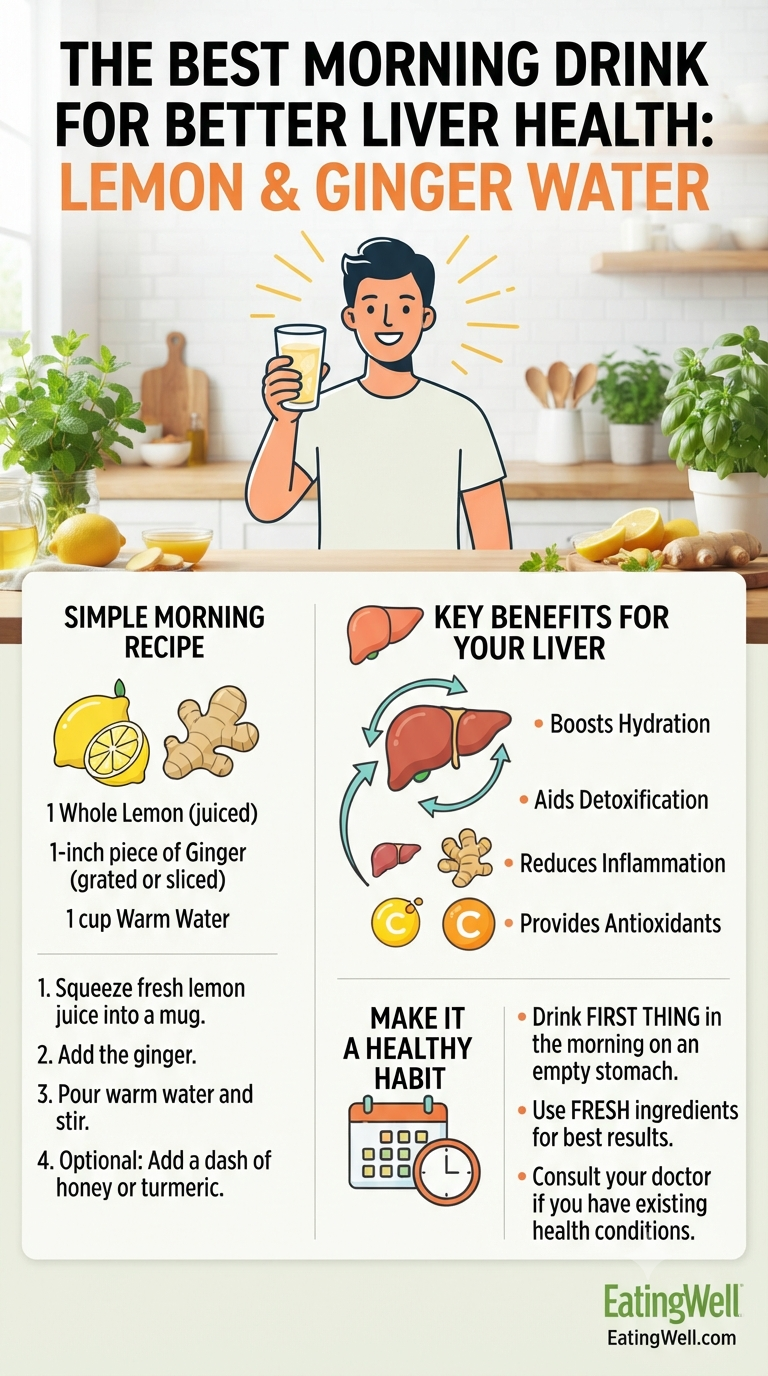

We often talk about kickstarting our metabolism or waking up our brains, but how often do you think about your liver first thing in the morning? Your liver is the ultimate multitasker, working tirelessly to filter your blood, process nutrients, and detoxify your body. Given how hard it works, it deserves a little extra love.…

Continue Reading Wake Up Your Liver: Why Lemon & Ginger Water Is Your Morning Must-Have

In today’s volatile financial landscape, where market fluctuations can turn a sound investment strategy upside down overnight, finding a safe haven for your hard-earned money is more important than ever. If you are looking for a risk-free way to grow your wealth, you don’t always need a high-risk portfolio. Sometimes, the most powerful tool is…

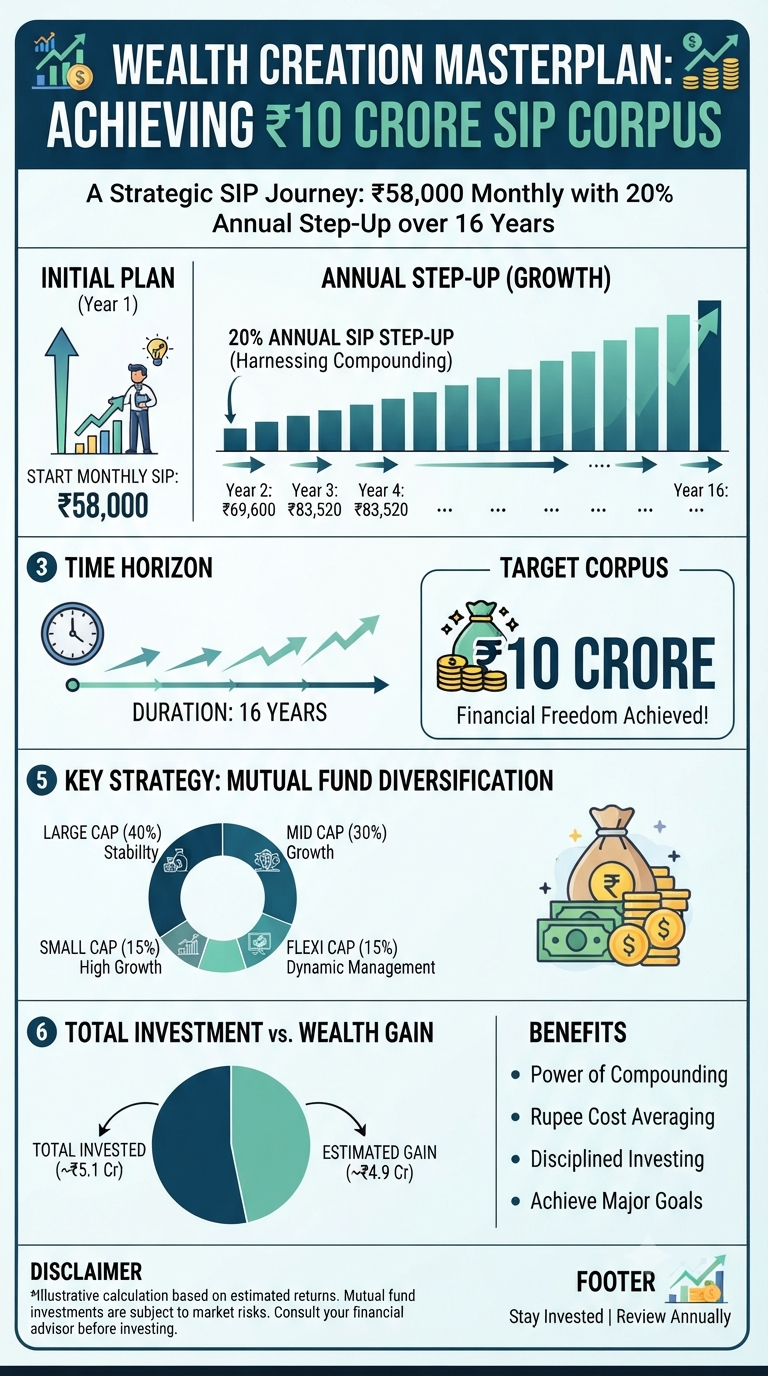

We all dream of financial freedom—that golden ticket where our money works harder for us than we ever did for it. But for most of us, that dream feels like exactly that: a dream. Something reserved for lottery winners or tech entrepreneurs. But what if I told you that you could build a ₹10 Crore…

Continue Reading The ₹10 Crore Dream: Is a Strategic SIP the Ultimate Wealth Creation Masterplan?

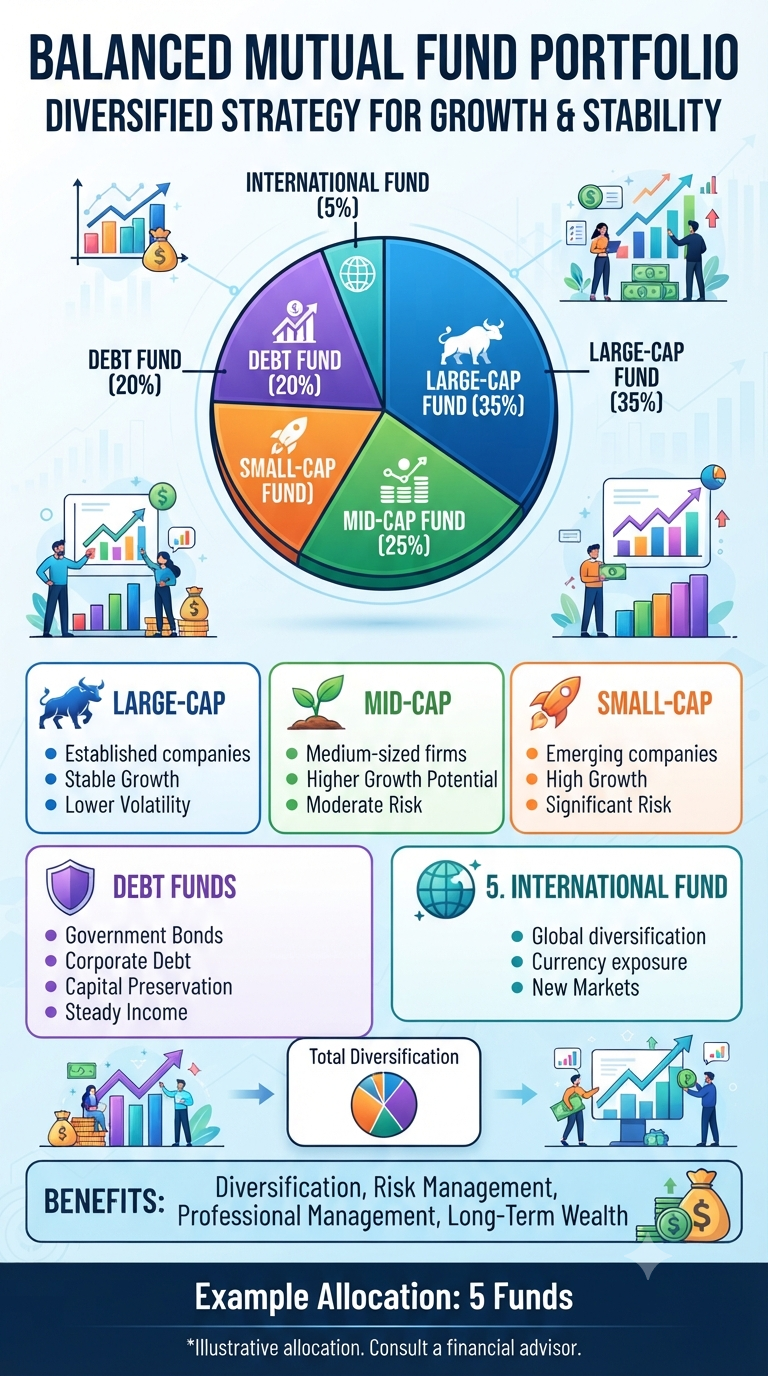

We’ve all been there—scrolling through an investment app, seeing a shiny new mutual fund, and thinking, “Why not? Adding another one can’t hurt, right?” It’s easy to fall into the trap of “fund collecting.” You assume that by holding ten, fifteen, or twenty different schemes, you’re becoming the ultimate master of diversification. But according to…

Continue Reading Less is More: Why Your Portfolio Doesn’t Need a Dozen Mutual Funds

Shreejith is the founder of InfographicStory.com, a hub for visual learning and data storytelling. Dedicated to simplifying complex ideas, he creates infographics that turn facts into insights. Have questions or collaboration ideas? Reach out to him at storyinfographic@gmail.com.